Walmart 2002 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2002 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

22

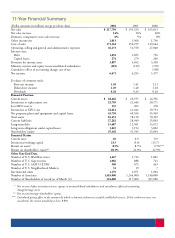

The Company holds currency swaps to hedge its net investment in the United Kingdom. The following tables provide information about our cross-

currency interest rate swap agreements by functional currency, and presents the information in United States dollar equivalents. For these instruments

the tables present notional amounts, exchange rates and interest rates by contractual maturity date.

Foreign Currency Exchange Rate Sensitivity as of January 31, 2002

Principal (Notional) Amount by Expected Maturity

Fair value

(Amounts in millions) 2003 2004 2005 2006 2007 Thereafter Total 1/31/2002

Currency Swap Agreements

Payment of Great Britain pounds

Notional amount – – – – – $ 1,250 $ 1,250 $ 192

Average contract rate – – – – – 0.6 0.6

Fixed rate received – USD rate – – – – – 7.4% 7.4%

Fixed rate paid – Great Britain pound rate – – – – – 5.8% 5.8%

Payment of Canadian dollars

Notional amount – – – – – 325 325 8

Average contract rate – – – – – 1.5 1.5

Fixed rate received – USD rate – – – – – 5.6% 5.6%

Fixed rate paid – Canadian dollar rate – – – – – 5.7% 5.7%

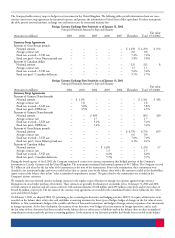

Foreign Currency Exchange Rate Sensitivity as of January 31, 2001

Principal (Notional) Amount by Expected Maturity

Fair value

(Amounts in millions) 2002 2003 2004 2005 2006 Thereafter Total 1/31/2001

Currency Swap Agreements

Payment of German Deutschemarks

Notional amount – $ 1,101 – – – – $ 1,101 $ 186

Average contract rate – 1.8 – – – – 1.8

Fixed rate received – USD rate – 5.8% – – – – 5.8%

Fixed rate paid – DEM rate – 4.5% – – – – 4.5%

Payment of German Deutschemarks

Notional amount – – $ 809 – – – 809 180

Average contract rate – – 1.7 – – – 1.7

Fixed rate received – USD rate – – 5.2% – – – 5.2%

Fixed rate paid – DEM rate – – 3.4% – – – 3.4%

Payment of Great Britain pounds

Notional amount – – – – – $ 4,750 4,750 659

Average contract rate – – – – – 0.6 0.6

Fixed rate received – USD rate – – – – – 7.0% 7.0%

Fixed rate paid – Great Britain pound rate – – – – – 6.1% 6.1%

Payment of Canadian dollars

Notional amount – – – $ 1,250 – – 1,250 57

Average contract rate – – – 1.5 – – 1.5

Fixed rate received – USD rate – – – 6.6% – – 6.6%

Fixed rate paid – Canadian dollar rate – – – 5.7% – – 5.7%

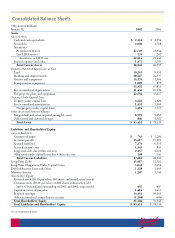

During the fourth quarter of fiscal 2002, the Company terminated certain cross currency instruments that hedged portions of the Company’s

investments in Canada, Germany and the United Kingdom. The instruments terminated had notional amounts of $6.7 billion. The Company received

$1.1 billion in cash related to the fair value of the instruments at the time of the terminations. Prior to the terminations, these instruments were

classified as net investment hedges and were recorded at fair value as current assets on the balance sheet with a like amount recorded in the shareholders’

equity section of the balance sheet in line “other accumulated comprehensive income.” No gain related to the terminations was recorded in the

Company’s income statement.

We routinely enter into forward currency exchange contracts in the regular course of business to manage our exposure against foreign currency

fluctuations on cross-border purchases of inventory. These contracts are generally for durations of six months or less. At January 31, 2002 and 2001,

we held contracts to purchase and sell various currencies with notional amounts of $118 million and $292 million, respectively, and net fair values of

$0 and $6 million, respectively. The fair values of the currency swap agreements are recorded in the consolidated balance sheets within the line “other

assets and deferred charges.”

On February 1, 2001, we adopted SFAS 133 pertaining to the accounting for derivatives and hedging activities. SFAS 133 requires all derivatives to be

recorded on the balance sheet at fair value and establishes accounting treatment for three types of hedges: hedges of changes in the fair value of assets,

liabilities, or firm commitments; hedges of the variable cash flows of forecasted transactions; and hedges of foreign currency exposures of net investments

in foreign operations. At the date of adoption, the majority of our derivatives were hedges of net investments in foreign operations, and as such,

the fair value of these derivatives had been recorded on the balance sheet as either assets or liabilities and on the balance sheet in other accumulated

comprehensive income under the previous accounting guidance. As the majority of our derivative portfolio had already been recorded on the balance