Walmart 2004 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2004 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

combination of commercial paper and long-term debt. We plan to refinance existing long-term debt as it matures and may desire to

obtain additional long-term financing for other corporate purposes. We anticipate no difficulty in obtaining long-term financing in view

of our credit rating and favorable experiences in the debt market in the recent past. At January 31, 2004, Standard & Poors (“S&P”),

Moody’s Investors Services, Inc. and Fitch Ratings rated our commercial paper A-1+, P-1 and F1+ and our long-term debt AA, Aa2 and

AA, respectively. As of January 31, 2004, we had $6 billion of debt securities remaining under a shelf registration statement previously

filed with the United States Securities and Exchange Commission (“SEC”) which are eligible for issuance, subject to market conditions in

the public markets. Subsequent to fiscal 2004 year-end, in February and March 2004, we sold notes totaling $1.25 billion and $750

million, respectively, under that shelf registration statement. These notes bear interest of 4.125% and mature in February 2011. The

proceeds from the sale of these notes were used for general corporate purposes. After consideration of this debt issuance, we are

permitted to sell up to $4 billion of public debt under our shelf registration statement.

At January 31, 2004, the ratio of our debt to our total capitalization was 38%. Historically, our objective has been to maintain a debt to

total capitalization ratio of approximately 40%.

Future Expansion

In the United States, we plan to open approximately 40 to 45 new Discount Stores and approximately 230 to 240 new Supercenters in

fiscal 2005. Conversions and/or relocations of existing Discount Stores will account for approximately 150 of the new Supercenters, with

the balance being new locations. We also plan to further expand our Neighborhood Market concept by adding approximately 20 to 25

new units during fiscal 2005. The SAM’S CLUB segment plans to open 30 to 35 Clubs during fiscal 2005, of which approximately 20 will

be relocations or expansions of existing SAM’S CLUBs. In order to serve these and future developments, the Company plans to construct

five new distribution centers in the next fiscal year. Internationally, the Company plans to open 130 to 140 new units, of which

approximately 30 will be conversions and/or relocations. Projects scheduled to open within the International segment include new

stores and Clubs as well as relocations of a few existing units. The units also include restaurants, specialty apparel retail stores and

supermarkets. The planned square footage growth for fiscal 2005 represents approximately 50 million square feet of new retail space,

which is more than an 8% increase over current square footage. We estimate that our capital expenditures in fiscal 2005 relating to

these new units and distribution centers will be approximately $12 billion in the aggregate. We plan to finance expansion primarily out

of cash flows from operations and with a combination of commercial paper and the issuance of long-term debt.

Subsequent to fiscal year-end 2004, in February 2004, the Company completed its purchase of Bompreco S.A. Supermercados do

Nordeste (“Bompreco”), a supermarket chain in northern Brazil with 118 hypermarkets, supermarkets and mini-markets. The purchase

price was approximately $300 million. The results of operations for Bompreco will be consolidated beginning in fiscal 2005.

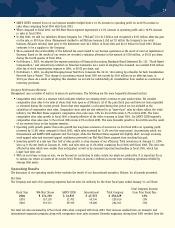

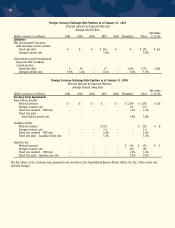

Market Risk

Market risks relating to our operations include changes in interest rates and changes in foreign exchange rates. We enter into interest

rate swaps to minimize the risks and costs associated with financing activities, as well as to maintain an appropriate mix of fixed- and

floating-rate debt. Our preference is to maintain approximately 50% of our debt portfolio, including interest rate swaps in floating-rate

debt. The swap agreements are contracts to exchange fixed- or variable-rates for variable- or fixed-interest rate payments periodically

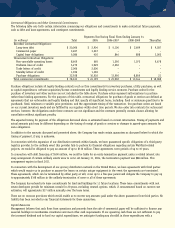

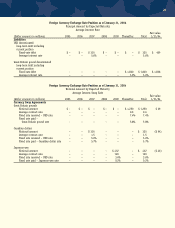

over the life of the instruments. The following tables provide information about our derivative financial instruments and other financial

instruments that are sensitive to changes in interest rates. For debt obligations, the table presents principal cash flows and related

weighted-average interest rates by expected maturity dates. For interest rate swaps, the table presents notional amounts and interest

rates by contractual maturity dates. The applicable floating-rate index is included for variable-rate instruments. The fair values of all

instruments presented are based on expected interest rate curves. Current fair values may not be indicative of future performance due

to changes in market conditions.

26