Walmart 2004 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2004 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

40

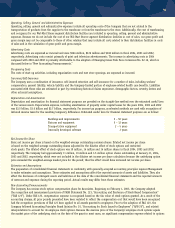

was recognized under APB 25. The adoption of the fair value method in 2003 resulted in a reduction of retained earnings of

$348 million, an increase in paid-in capital of $472 million and an increase in deferred tax assets of $124 million. Following the

provisions of FAS 123, fiscal 2004, 2003 and 2002 include a reduction of net income of $102 million, $84 million and $79 million,

respectively, or $0.02 in each fiscal year.

The fair value of stock options was estimated at the date of grant using the Black-Scholes option valuation model which was developed

for use in estimating the fair value of traded options, which have no vesting restrictions and are fully transferable. Option valuation

methods require the input of highly subjective assumptions, including the expected stock price volatility. The fair value of these options

was estimated at the date of the grant based on the following assumptions:

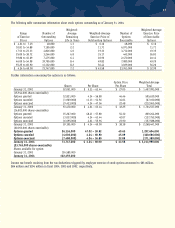

2004 2003 2002

Dividend yield 1.0% 0.7% 0.7%

Volatility 32.3% 32.1% 36.5%

Risk-free interest rate 2.8% 3.2% 4.6%

Expected life in years 4.5 4.6 5.2

Weighted average fair value

of options at grant date $ 15.83 $ 15.67 $ 20.27

On February 1, 2003, the Company adopted the standards of FASB Statement No. 143, “Asset Retirement Obligations” (“FAS 143”).

FAS 143 requires the Company to recognize the fair value of a liability associated with the cost the Company would be obligated to

incur in order to retire an asset at some point in the future. The adoption of this standard did not have a material impact on the

Company’s results of operations.

In July 2002, the FASB issued FAS No. 146, “Accounting for Costs Associated with Exit or Disposal Activities” (“FAS 146”). FAS 146

addresses financial accounting and reporting for costs associated with exit or disposal activities and replaces the FASB’s Emerging Issues

Task Force (“EITF”) 94-3, “Liability Recognition for Certain Employee Termination Benefits and Other Costs to Exit an Activity (including

Certain Costs Incurred in a Restructuring).” FAS 146 requires that a liability for a cost associated with an exit or disposal activity be

recognized when the liability is incurred. FAS 146 also establishes that fair value is the objective for initial measurement of the liability.

The statement is effective for exit or disposal activities initiated after December 31, 2002. The adoption of FAS 146 in fiscal 2004 did

not have a material impact on the Company’s financial statements.

In April 2003, the FASB issued FAS No. 149, “Amendment of Statement 133 on Derivative Instruments and Hedging Activities”

(“FAS 149”). This statement amends and clarifies accounting for derivative instruments and is effective for contracts entered into or

modified after June 30, 2003. The adoption of FAS 149 did not have a material impact on our financial statements.

In May 2003, the FASB issued FAS No. 150, “Accounting for Certain Financial Instruments with Characteristics of both Liabilities and

Equity” (“FAS 150”). FAS 150 clarifies the classification and measurement of certain financial instruments with characteristics of both

liabilities and equity, and is effective for financial instruments entered into or modified after May 31, 2003, or otherwise for the first

interim period beginning after June 15, 2003. The adoption of FAS 150 did not have a material impact on our financial statements.

In November 2002, the EITF reached a consensus on EITF 02-16, “Accounting by a Reseller for Cash Consideration Received from a

Vendor” (“EITF 02-16”), which addresses the accounting for “Cash Consideration” (which includes slotting fees, cooperative advertising

payments, etc.) and “Rebates or Refunds” from a vendor that are payable only if the merchant completes a specified cumulative level

of purchases or remains a customer of the vendor for a specified period of time. EITF 02-16 established an overall presumption that

all consideration from vendors should be accounted for as a reduction of item cost and be recognized at the time the related inventory

is sold. EITF 02-16 provides that the overall presumption can be overcome in two ways. First, consideration representing a payment

for assets or services delivered to a vendor should be classified as revenue or other income. Second, consideration representing a

reimbursement of a specific, incremental, identifiable cost incurred in selling the vendor’s product should be recorded as a reduction

of that expense. Wal-Mart had historically recorded certain consideration from vendors primarily as a reduction of advertising expense.

We adopted EITF 02-16 on February 1, 2003, and now account for this consideration as a reduction of purchases. The adoption of

EITF 02-16 resulted in an after-tax impact of approximately $140 million, or $0.03 per share.

In November 2003, the FASB ratified the EITF’s consensus on Issue 03-10, “Application of Issue 02-16 by Resellers to Sales Incentives

Offered to Consumers by Manufacturers” (“EITF 03-10”), which amends EITF 02-16. This consensus requires that if certain criteria are met,

consideration received by a reseller in the form of reimbursement from a vendor for honoring the vendor’s sales incentives offered directly

to consumers (i.e., manufacturer’s coupons) should not be recorded as a reduction of the cost of the reseller’s purchases from the vendor.

The adoption of EITF 03-10, which is required for us on February 1, 2004, did not have a material impact on our financial statements.