Windstream 2007 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2007 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

(c) capital expenditures must not exceed a specified amount in any fiscal year (for 2008 this amount is

$534.3 million, which includes $84.3 million of unused capacity from 2007).

In addition, certain of the Company’s debt agreements contain various covenants and restrictions specific to the

subsidiary that is the legal counterparty to the agreement. Under the Company’s long-term debt agreements,

acceleration of principal payments would occur upon payment default, violation of debt covenants not cured within 30

days, or breach of certain other conditions set forth in the borrowing agreements. At December 31, 2007, the Company

was in compliance with all such covenants and restrictions.

Windstream’s senior secured and senior unsecured credit ratings with Moody’s Investors Service (“Moody’s”),

Standard & Poor’s Corporation (“S&P”) and Fitch Ratings (“Fitch”) were as follows at December 31, 2007:

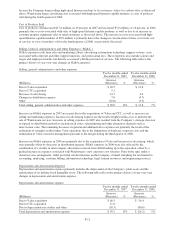

Description Moody’s S&P Fitch

Senior secured credit rating Baa3 BBB BBB-

Senior unsecured credit rating Ba3 BB- BB+

Outlook Stable Negative Stable

Factors that could affect Windstream’s short and long-term credit ratings would include, but are not limited to, a

material decline in the Company’s operating results, increased debt levels relative to operating cash flows resulting

from future acquisitions, increased capital expenditure requirements, or changes to our dividend policy. If

Windstream’s credit ratings were to be downgraded from current levels, the Company would incur higher interest costs

on its borrowings, and the Company’s access to the public capital markets could be adversely affected. A downgrade in

Windstream’s current short or long-term credit ratings would not accelerate scheduled principal payments of

Windstream’s existing long-term debt.

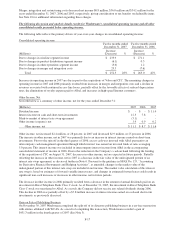

Historical Cash Flows

(Millions) 2007 2006 2005

Cash flows from (used in):

Operating activities $1,033.7 $ 1,145.7 $ 986.4

Investing activities (867.1) (299.0) (353.6)

Financing activities (481.4) (471.8) (634.2)

Change in cash and short-term investments $ (314.8) $ 374.9 $ (1.4)

Cash Flows – Operating Activities

Cash flows from operating activities decreased by $112.0 million in 2007 as compared to 2006. This decrease was

primarily due to increases of $140.1 million in interest payments as the Company did not make its first interest

payments on the debt issued and assumed pursuant to the spin off and merger transactions until the fourth quarter of

2006. These decreases in cash flows were partially offset by new cash flows generated in 2007 from the acquired Valor

and CTC operations. During 2007, the Company generated sufficient cash flows from operations to fund its capital

expenditure requirements, dividend payments and scheduled principle payments on its long-term debt. The increase in

cash provided from operations in 2006 as compared to 2005 was driven primarily by increased cash flows due to the

acquisition of Valor. Additionally, cash flows from operations in all years reflect changes in working capital

requirements, including timing differences in the billing and collection of accounts receivable, purchases of inventory,

and the payment of trade payables and taxes.

Cash Flows – Investing Activities

During 2007, cash used in investing activities included $546.8 million in net cash used to acquire CTC. This cash

outlay was funded primarily with cash on hand at the time of the acquisition, with the remainder funded through

borrowings from the Company’s revolving line of credit. It was partially offset by $40.0 million in proceeds received

on the sale of the publishing business. During 2006, cash flows from investing activities included $69.0 million of net

cash assumed in the acquisition of Valor.

Capital expenditures are the Company’s primary use of capital resources. Capital expenditures were $365.7 million in

2007, $373.8 million in 2006 and $356.9 million in 2005. Capital expenditures in each of the past three years were

incurred to construct additional network facilities and to upgrade our telecommunications network in order to expand

our offering of other communications services, including high-speed Internet communications services. During each of

the past three years, the Company funded its capital expenditures through internally generated funds.

F-20