Windstream 2007 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2007 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

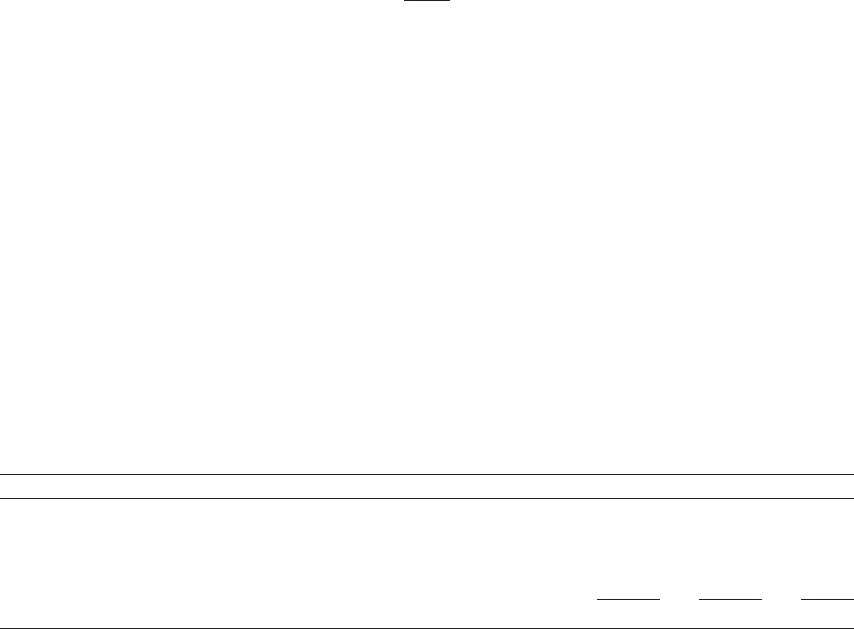

5. Debt, Continued:

borrowing under the revolving credit agreement. Accordingly, the total amount outstanding under the letters of

credit and the indebtedness incurred under the revolving credit agreement may not exceed $500.0 million. At

December 31, 2007, the amount available for borrowing under the revolving credit agreement was $394.1 million.

The terms of the credit facility and indentures include customary covenants that, among other things, require

Windstream to maintain certain financial ratios and restrict its ability to incur additional indebtedness. These

financial ratios include a maximum leverage ratio of 4.5 to 1.0 and a minimum interest coverage ratio of 2.75 to

1.0. In addition, the covenants include restrictions on capital expenditures, which must not exceed a specified

amount for any fiscal year (for 2007 this amount was $530.0 million, which included $80.0 million of unused

capacity from 2006). The Company was in compliance with all covenants as of December 31, 2007.

Maturities and sinking fund requirements for the five years after 2007 for long-term debt outstanding as of

December 31, 2007, were $24.3 million for 2008 and 2009, $24.0 million for 2010, $403.8 million for 2011, and

$27.5 million for 2012.

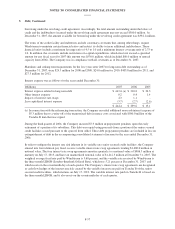

Interest expense was as follows for the years ended December 31:

(Millions) 2007 2006 2005

Interest expense related to long-term debt $ 443.6 (a) $ 210.8 $ 20.3

Other interest expense 0.2 0.4 1.4

Impacts of interest rate swaps 4.3 1.1 -

Less capitalized interest expense (3.7) (2.7) (2.6)

$ 444.4 $ 209.6 $ 19.1

(a) In connection with the refinancing transaction, the Company recorded additional non-cash interest expense of

$5.3 million due to a write-off of the unamortized debt issuance costs associated with $500.0 million of the

Tranche B loan that was repaid.

During the third quarter of 2006, the Company incurred $7.9 million in prepayment penalties upon the early

retirement of a portion of its subsidiary. This debt was repaid using proceeds from a portion of the senior secured

credit facilities issued pursuant to the spin off from Alltel. These debt prepayment penalties are included in loss on

extinguishment of debt in the accompanying consolidated statement of income for the year ended December 31,

2006.

In order to mitigate the interest rate risk inherent in its variable rate senior secured credit facilities, the Company

entered into four identical pay fixed, receive variable interest rate swap agreements totaling $1,600.0 million in

notional value. The four interest rate swap agreements amortize quarterly to a notional value of $906.3 million at

maturity on July 17, 2013, and have an unamortized notional value of $1,412.5 million at December 31, 2007. The

weighted average fixed rate paid by Windstream is 5.60 percent, and the variable rate received by Windstream is

the three-month LIBOR (London-Interbank Offered Rate), which was 5.21 percent at December 31, 2007, and

which resets on the seventeenth day of each quarter. The Company’s interest rate swap agreements are designated

as cash flow hedges of the interest rate risk created by the variable interest rate paid on Tranche B of the senior

secured credit facilities, which matures on July 17, 2013. The variable interest rate paid on Tranche B is based on

the three-month LIBOR, and it also resets on the seventeenth day of each quarter.

F-57