Windstream 2007 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2007 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Background and Basis for Presentation:

Formation of Windstream – On July 17, 2006, Alltel Corporation (“Alltel”) completed the spin off of its wireline

telecommunications division, Alltel Holding Corp., to its shareholders. Immediately after the consummation of

the spin off, Alltel Holding Corp. merged with and into Valor Communications Group Inc. (“Valor”), with Valor

continuing as the surviving corporation. The resulting company was renamed Windstream Corporation. The

merger was accounted for using the purchase method of accounting for business combinations in accordance with

Statement of Financial Accounting Standards (“SFAS”) No. 141 “Business Combinations”, with Alltel Holding

Corp. serving as the accounting acquirer. The accompanying consolidated financial statements reflect the

combined operations of Alltel Holding Corp. and Valor following the spin off and merger transactions on July 17,

2006. Results of operations prior to the merger and for all historical periods presented are for Alltel Holding Corp.

Description of Business – In this report, Windstream Corporation, a Delaware corporation, and its wholly owned

subsidiaries are referred to as “Windstream”, “we”, or “the Company”. For all periods prior to the merger with

Valor described herein, references to the Company include Alltel Holding Corp. or the wireline

telecommunications division and related businesses of Alltel. Windstream is one of the largest providers of

telecommunications services in rural communities in the United States, and based on the number of telephone

lines in service, is the fifth largest local telephone company in the country. Windstream has focused its

communications business strategy on enhancing the value of its customer relationships by offering additional

products and services and providing superior customer service. The Company’s subsidiaries provide local

telephone, high-speed Internet, long distance, network access and video services in sixteen states.

Telecommunications products are also warehoused and sold by the Company’s product distribution subsidiary.

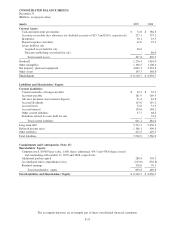

Basis of Presentation – The preparation of financial statements, in accordance with accounting principles

generally accepted in the United States, requires management to make estimates and assumptions that affect the

reported amounts of assets, liabilities, revenues and expenses and disclosure of contingent assets and liabilities.

The estimates and assumptions used in the accompanying consolidated financial statements are based upon

management’s evaluation of the relevant facts and circumstances as of the date of the consolidated financial

statements. Actual results may differ from the estimates and assumptions used in preparing the accompanying

consolidated financial statements, and such differences could be material. Certain prior year amounts have been

reclassified to conform to the 2007 financial statement presentation. All significant affiliated transactions, except

those with certain affiliates described below in Note 2, have been eliminated.

2. Summary of Significant Accounting Policies and Changes:

Significant Accounting Policies

Cash and Short-term Investments – Cash and short-term investments consist of highly liquid investments with

original maturities of three months or less.

Accounts Receivable – Accounts receivable consist principally of trade receivables from customers and are

generally unsecured and due within 30 days. Expected credit losses related to trade accounts receivable are

recorded as an allowance for doubtful accounts in the consolidated balance sheets. In establishing the allowance

for doubtful accounts, the Company considers a number of factors, including historical collection experience,

aging of the accounts receivable balances, current economic conditions, and a specific customer’s ability to meet

its financial obligations to the Company. When internal collection efforts on accounts have been exhausted, the

accounts are written off by reducing the allowance for doubtful accounts. Concentration of credit risk with respect

to accounts receivable is limited because a large number of geographically diverse customers make up the

Company’s customer base, thus spreading the credit risk. Due to varying customer billing cycle cut-off times, the

Company must estimate service revenues earned but not yet billed at the end of each reporting period. Included in

accounts receivable are unbilled receivables related to communications revenues of $21.0 million and

$33.5 million at December 31, 2007 and 2006, respectively.

Inventories – Inventories are stated at the lower of cost or market value. Cost is determined using either an

average original cost or specific identification method of valuation.

Assets Held For Sale – In accordance with SFAS No. 142, certain assets acquired from CT Communications, Inc.

(“CTC”) are classified as held for sale and are included in acquired assets held for sale in the accompanying

F-38