3M 2013 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2013 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

32

Legal Proceedings:

The categories of claims for which the Company has a probable and estimable liability, the amount of its liability accruals,

and the estimates of its related insurance receivables are critical accounting estimates related to legal proceedings.

Please refer to the section entitled “Process for Disclosure and Recording of Liabilities and Insurance Receivables

Related to Legal Proceedings” (contained in “Legal Proceedings” in Note 13) for additional information about such

estimates.

Pension and Postretirement Obligations:

3M has various company-sponsored retirement plans covering substantially all U.S. employees and many employees

outside the United States. The primary U.S. defined-benefit pension plan was closed to new participants effective January

1, 2009. The Company accounts for its defined benefit pension and postretirement health care and life insurance benefit

plans in accordance with Accounting Standard Codification (ASC) 715, Compensation — Retirement Benefits, in

measuring plan assets and benefit obligations and in determining the amount of net periodic benefit cost. ASC 715

requires employers to recognize the underfunded or overfunded status of a defined benefit pension or postretirement plan

as an asset or liability in its statement of financial position and recognize changes in the funded status in the year in which

the changes occur through accumulated other comprehensive income, which is a component of stockholders’ equity.

While the company believes the valuation methods used to determine the fair value of plan assets are appropriate and

consistent with other market participants, the use of different methodologies or assumptions to determine the fair value of

certain financial instruments could result in a different estimate of fair value at the reporting date.

Pension benefits associated with these plans are generally based primarily on each participant’s years of service,

compensation, and age at retirement or termination. Two critical assumptions, the discount rate and the expected return

on plan assets, are important elements of expense and liability measurement. See Note 10 for additional discussion of

actuarial assumptions used in determining pension and postretirement health care liabilities and expenses.

The Company determines the discount rate used to measure plan liabilities as of the December 31 measurement date for

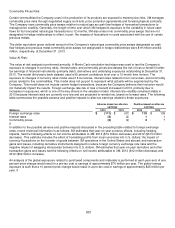

its pension and postretirement benefit plans. The discount rate reflects the current rate at which the associated liabilities

could be effectively settled at the end of the year. The Company sets its rate to reflect the yield of a portfolio of high

quality, fixed-income debt instruments that would produce cash flows sufficient in timing and amount to settle projected

future benefits. Using this methodology, the Company determined a discount rate of 4.98% for the primary U.S. qualified

pension plan and 4.83% for U.S. postretirement plans to be appropriate as of December 31, 2013, which represents an

increase from the 4.14% and 4.00% rates, respectively, used as of December 31, 2012. The weighted average discount

rate for international pension plans as of December 31, 2013 was 4.02%, an increase from the 3.78% rate used as of

December 31, 2012.

A significant element in determining the Company’s pension expense in accordance with ASC 715 is the expected return

on plan assets, which is based on historical results for similar allocations among asset classes. For the primary U.S.

qualified pension plan, the expected long-term rate of return on an annualized basis for 2014 is 7.75%, a 0.25% decrease

from 2013. Refer to Note 10 for information on how the 2014 rate was determined. Return on assets assumptions for

international pension and other post-retirement benefit plans are calculated on a plan-by-plan basis using plan asset

allocations and expected long-term rate of return assumptions. The weighted average expected return for the international

pension plan is 5.83% for 2014, compared to 5.87% for 2013.

For the year ended December 31, 2013, the Company recognized total consolidated defined benefit pre-tax pension and

postretirement expense (after settlements, curtailments and special termination benefits) of $553 million, down from

$650 million in 2012. Defined benefit pension and postretirement expense (before settlements, curtailments and special

termination benefits) is anticipated to decrease to $393 million in 2014, a decrease of $160 million compared to 2013. For

the pension plans, holding all other factors constant, a 0.25 percentage point increase/decrease in the expected long-term

rate of return on plan assets would decrease/increase 2014 pension expense by approximately $34 million for U.S.

pension plans and approximately $14 million for international pension plans. Also, holding all other factors constant, a

0.25 percentage point increase in the discount rate used to measure plan liabilities would decrease 2014 pension

expense by approximately $41 million for U.S. pension plans and approximately $21 million for international pension

plans. In addition, a 0.25 percentage point decrease in the discount rate used to measure plan liabilities would increase

2014 pension expense by approximately $42 million for U.S. pension plans and approximately $24 million for international

pension plans.