APC 2004 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2004 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

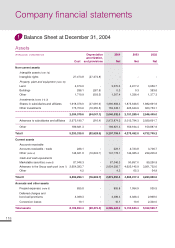

114

Plan assets have been reclassified as a deduction of

corresponding plan liabilities (315 million at January

1, 2004 and 262 million at December 31, 2004).

Net effect on pension and other post employment

benefit liabilities is 420 million at January 1, 2004

and 365 million at December 31, 2004.

The absence of amortization of actuarial gains and

losses recognized in the balance sheet has an effect

of 38 million on the 2004 IFRS income statement.

of which 20 million is reported in administrative

costs and 18 million in cost of sales.

Going forward, the Group has decided to recognize all

actuarial gains and losses in shareholders' equity, on

the line "Statement Of Recognized Income and

Expenses ("SORIES")", as allowed in the amended

version of IAS 19 (not yet endorsed by European

Union). The amount for 2004 is 22 million, net of tax.

2.3.6 - Revenue recognition

The revenue recognition policies applied in the

French GAAP accounts are not materially different

from the requirements of IAS 18 -

Revenue

and IAS

11 -

Long-Term Contracts:

Sales of goods are recognized when the significant

risks and rewards of ownership are transferred to the

buyer.

Long-term contract revenue is recognized by the

percentage-of-completion method and a provision is

booked for expected contract losses as soon as they

are considered probable.

Volume rebates granted to distributors are recog-

nized as an expense from initial sales made by

Schneider Electric to these distributors.The change in

generating event has been recognized under French

and IFRS financial statements as of January 1, 2004

and represents 32 million.

Certain cash discounts (8.4 million in 2004)

included in interest expense and certain sales incen-

tives (7.6 million in 2004) reported under selling

expenses have been reclassified as a reduction of

sales in the IFRS accounts.

2.3.7 - IFRS 2- Share-Based Payments

I

FRS 2 applies to stock options granted after

November 7, 2002 that do not vest prior to January 1,

2005.

The plans concerned are plan 21 dated February 5,

2003 (2,000,000 options exercisable as from

February 5, 2007) and plan 24 dated May 6, 2004

(2,060,700 options exercisable as from May 6, 2008).

The Group has chosen to value options using the Cox

Ross Rubinstein binomial option pricing model.

Based on market data at the grant dates, the total

stock option expense for 2004 is 8.9 million, report-

ed under administrative expenses.

2.4 - Standards with little

or no impact on the Group accounts

2.4.1 - Consolidation scope and methods

Application of the control criteria set out in IAS 27 -

Consolidated Financial Statements And Accounting

For Investments In Subsidiaries

has not led to any

change in the companies fully consolidated in the

Group accounts.

The principles and methods described in Note 1.3 to

the 2004 French GAAP consolidated financial state-

ments are compliant with IFRS.

2.4.2 - Foreign currency translation

The cumulative translation adjustment has been reset

to zero in the opening IFRS balance sheet at January

1, 2004, as allowed under IFRS 1. The impact of

reclassification within shareholder's equity at January

1, 2004 is 211 million.

Adoption of IAS 21 and IAS 29 has no impact on the

Group accounts because the foreign currency con-

version and translation principles applied in the

French GAAP accounts (note 1.4 and 1.5 to the 2004

French GAAP Consolidated Financial Statements)

comply fully with the methods prescribed under IFRS.

2.4.3 - Property, plant and equipment and leases

Adoption of IAS 16 -

Property, Plant And Equipment

and IAS 40 -

Investment Property

has no impact on

the Group accounts.

Property, plant and equipment consist mainly of man-

ufacturing equipment dedicated to specific product

lines and material parts of individual items of equip-

ment are already depreciated separately in the

French GAAP accounts.

Consequently, there is no need to change the assets'

carrying value or depreciation schedules to comply

with IAS 16. In addition, the Group does not own any

investment property.

The Group has chosen to apply the benchmark treat-

ment set out in IAS 16, which consists of measuring

property, plant and equipment in the opening IFRS

balance sheet at historical cost.

Adoption of IAS 17 - Leases has led to the restate-

ment of certain non material leases. The impact is

5.5 million on assets and 5 million on financial

debt as of January 1, 2004.

In accordance with IFRS 5 -

Non-Current Assets Held

For Sale And Discontinued Operations

, assets held

for sale at the year-end (consisting mainly of real

estate) are reported separately for 15 million at

January 1, 2004 and 8 million at December 31,

2004.

In the French GAAP accounts, borrowing costs for the

acquisition of property, plant and equipment are rec-

ognized as an expense and no such costs are capi-

talized. This method corresponds to the benchmark

treatment set out in IAS 23 -

Borrowing Costs.