American Airlines 1999 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 1999 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

|

|

48

6. FINANCIAL INSTRUMENTS AND RISK

MANAGEMENT

As part of the Company’s risk management program, AM R uses

a variety of financial instruments, including interest rate swaps,

fuel swap and option contracts and currency exchange agreements.

The Company does not hold or issue derivative financial instru-

ments for trading purposes.

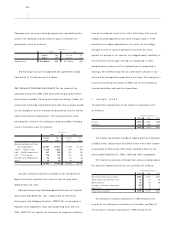

Notional Amounts and Credit Exposures of Derivatives The

notional amounts of derivative financial instruments summarized

in the tables which follow do not represent amounts exchanged

between the parties and, therefore, are not a measure of the

Company’s exposure resulting from its use of derivatives. The

amounts exchanged are calculated based on the notional amounts

and other terms of the instruments, which relate to interest rates,

exchange rates or other indices.

The Company is exposed to credit losses in the event of non-

performance by counterparties to these financial instruments, but

it does not expect any of the counterparties to fail to meet its

obligations. The credit exposure related to these financial instru-

ments is represented by the fair value of contracts with a positive

fair value at the reporting date, reduced by the effects of master

netting agreements. To manage credit risks, the Company selects

counterparties based on credit ratings, limits its exposure to a

single counterparty under defined guidelines, and monitors the

market position of the program and its relative market position

with each counterparty. The Company also maintains industry-

standard security agreements with the majority of its counter-

parties which may require the Company or the counterparty

to post collateral if the value of these instruments falls below

certain mark-to-market thresholds. As of December 31, 1999,

no collateral was required under these agreements, and the

Company does not expect to post collateral in the near future.

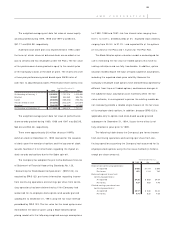

Interest Rate Risk Management American enters into interest

rate swap contracts to effectively convert a portion of its fixed-

rate obligations to floating-rate obligations. These agreements

involve the exchange of amounts based on a floating interest rate

for amounts based on fixed interest rates over the life of the

agreement without an exchange of the notional amount upon

which the payments are based. The differential to be paid or

received as interest rates change is accrued and recognized as an

adjustment of interest expense related to the obligation. The

related amount payable to or receivable from counterparties is

included in current liabilities or assets. The fair values of the swap

agreements are not recognized in the financial statements. Gains

and losses on terminations of interest rate swap agreements are

deferred as an adjustment to the carrying amount of the out-

standing obligation and amortized as an adjustment to interest

expense related to the obligation over the remaining term of the

original contract life of the terminated swap agreement. In the

event of the early extinguishment of a designated obligation, any

realized or unrealized gain or loss from the swap would be

recognized in income coincident with the extinguishment.

The following table indicates the notional amounts and fair

values of the Company’s interest rate swap agreements (in

millions):

December 31,

1999 1998

Notional Fair Notional Fair

Amount Value Amount Value

Interest rate swap agreements $696 $(9) $1,054 $38

The fair values represent the amount the Company would pay

or receive if the agreements were terminated at December 31,

1999 and 1998, respectively.