American Airlines 1999 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 1999 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

|

|

AMR CORPORATION

49

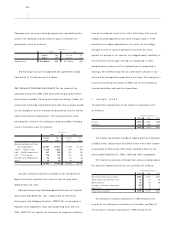

At December 31, 1999, the weighted-average remaining

life of the interest rate swap agreements in effect was 5.1 years.

The weighted-average floating rates and fixed rates on the

contracts outstanding were:

December 31,

1999 1998

Average floating rate 5.855% 5.599%

Average fixed rate 6.593% 6.277%

Floating rates are based primarily on LIBOR and may change

significantly, affecting future cash flows.

Fuel Price Risk Management American enters into fuel swap

and option contracts to protect against increases in jet fuel prices.

Under the fuel swap agreements, American receives or makes

payments based on the difference between a fixed price and a

variable price for certain fuel commodities. Under the fuel option

agreements, American pays a premium to cap prices at a fixed

level. The changes in market value of such agreements have a

high correlation to the price changes of the fuel being hedged.

Gains or losses on fuel hedging agreements are recognized as a

component of fuel expense when the underlying fuel being

hedged is used. Any premiums paid to enter into option contracts

are recorded as a prepaid expense and amortized to fuel expense

over the respective contract periods. Gains and losses on fuel

hedging agreements would be recognized immediately should

the changes in the market value of the agreements cease to have

a high correlation to the price changes of the fuel being hedged.

At December 31, 1999, American had fuel hedging agreements

with broker-dealers on approximately two billion gallons of fuel

products, which represents approximately 48 percent of its

expected 2000 fuel needs and approximately 10 percent of its

expected 2001 fuel needs. The fair value of the Company’s fuel

hedging agreements at December 31, 1999, representing the

amount the Company would receive to terminate the agree-

ments, totaled $232 million. At December 31, 1998, American

had fuel hedging agreements with broker-dealers on approxi-

mately two billion gallons of fuel products, which represented

approximately 48 percent of its expected 1999 fuel needs

and approximately 19 percent of its expected 2000 fuel needs.

The fair value of the Company’s fuel hedging agreements

at December 31, 1998, representing the amount the Company

would pay to terminate the agreements, totaled $108 million.

Foreign Exchange Risk Management To hedge against the risk

of future exchange rate fluctuations on a portion of American’s

foreign cash flows, the Company enters into various currency put

option agreements on a number of foreign currencies. The option

contracts are denominated in the same foreign currency in which

the projected foreign cash flows are expected to occur. These

contracts are designated and effective as hedges of probable

quarterly foreign cash flows for various periods through Decem-

ber 31, 2000, which otherwise would expose the Company to

foreign currency risk. Realized gains on the currency put option

agreements are recognized as a component of passenger

revenues. At December 31, 1999 and 1998, the notional amount

related to these options totaled approximately $445 million and

$597 million, respectively, and the fair value, representing the

amount AMR would receive to terminate the agreements,

totaled approximately $14 million and $10 million, respectively.

The Company has entered into Japanese yen currency

exchange agreements to effectively convert certain yen-based

lease obligations into dollar-based obligations. Changes in the

value of the agreements due to exchange rate fluctuations are

offset by changes in the value of the yen-denominated lease

obligations translated at the current exchange rate. Discounts or

premiums are accreted or amortized as an adjustment to interest

expense over the lives of the underlying lease obligations. The

related amounts due to or from counterparties are included in

other liabilities or other assets. The net fair values of the