American Airlines 1999 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 1999 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

|

|

50

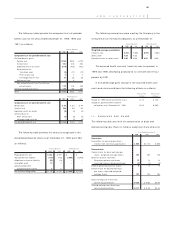

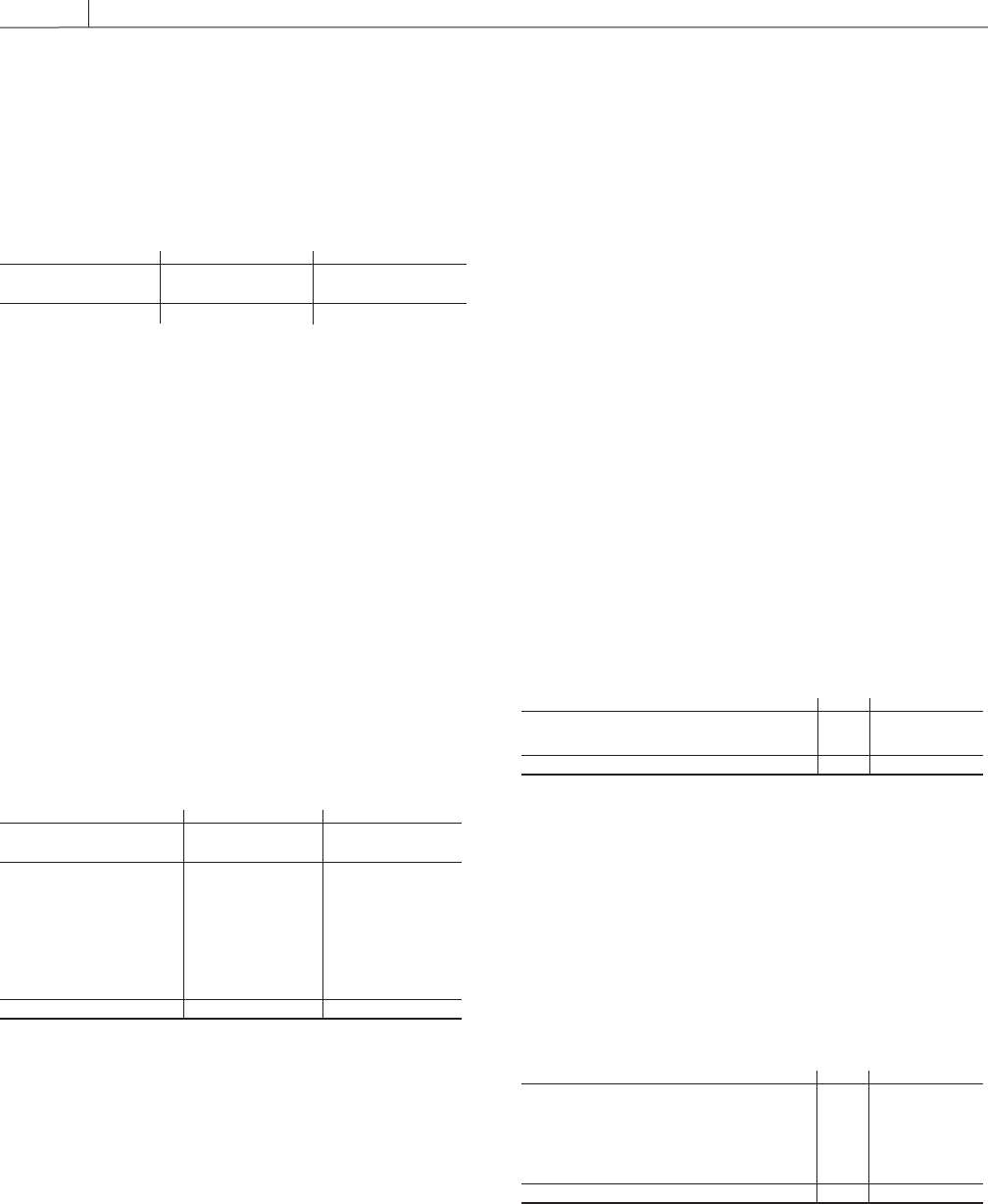

Company’s yen currency exchange agreements, representing the

amount the Company would receive or pay to terminate the

agreements, were (in millions):

December 31,

1999 1998

Notional Fair Notional Fair

Amount Value Amount Value

Japanese yen 33.6 billion $41 33.7 billion $(5)

The exchange rates on the Japanese yen agreements range

from 66.50 to 116.89 yen per U.S. dollar.

Fair Values of Financial Instruments The fair values of the

Company’s long-term debt were estimated using quoted market

prices where available. For long-term debt not actively traded, fair

values were estimated using discounted cash flow analyses, based

on the Company’s current incremental borrowing rates for similar

types of borrowing arrangements. The carrying amounts and

estimated fair values of the Company’s long-term debt, including

current maturities, were (in millions):

December 31,

1999 1998

Carrying Fair Carrying Fair

Value Value Value Value

Secured variable and fixed

rate indebtedness $2,651 $2,613 $ 890 $1,013

7.875% – 10.62% notes 1,014 1,024 875 973

9.0% – 10.20% debentures 437 469 437 531

6.0% – 7.10% bonds 176 174 176 189

Variable rate indebtedness 86 86 86 86

Other 16 16 20 20

$4,380 $4,382 $2,484 $2,812

All other financial instruments, except for the investment in

Equant, are either carried at fair value or their carrying value

approximates fair value.

Financial Accounting Standards Board Statement of Financial

Accounting Standards No. 133, “ Accounting for Derivative

Instruments and Hedging Activities” (SFAS 133), as amended, is

required to be adopted in fiscal years beginning after June 15,

2000. SFAS 133 will require the Company to recognize all deriva-

tives on the balance sheet at fair value. Derivatives that are not

hedges must be adjusted to fair value through income. If the

derivative is a hedge, depending on the nature of the hedge,

changes in the fair value of derivatives will either be offset

against the change in fair value of the hedged assets, liabilities, or

firm commitments through earnings or recognized in other

comprehensive income until the hedged item is recognized in

earnings. The ineffective portion of a derivative’s change in fair

value will be immediately recognized in earnings. The Company is

currently evaluating the impact of SFAS 133 on the Company’s

financial condition and results of operations.

7. INCOME TAXES

The significant components of the income tax provision were

(in millions):

Year Ended December 31,

1999 1998 1997

Current $167 $451 $206

Deferred 183 268 321

$350 $719 $527

The income tax provision includes a federal income tax provision

of $290 million, $628 million and $462 million and a state income

tax provision of $49 million, $78 million and $56 million for the

years ended December 31, 1999, 1998 and 1997, respectively.

The income tax provision differed from amounts computed at

the statutory federal income tax rate as follows (in millions):

Year Ended December 31,

1999 1998 1997

Statutory income tax provision $352 $641 $467

State income tax provision, net 32 51 36

Meal expense 19 18 20

Change in valuation allowance (67) (4) –

Other, net 14 13 4

Income tax provision $350 $719 $527

The change in valuation allowance in 1999 relates to the

reversal of the Company’s investment in Canadian (see Note 2).

The change in valuation allowance in 1998 relates to the