American Airlines 2003 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2003 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

|

|

35

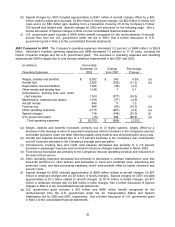

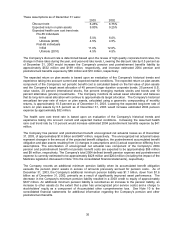

These assumptions as of December 31 were:

2003 2002

Discount rate 6.25% 6.75%

Expected return on plan assets 9.00% 9.25%

Expected health care cost trend rate:

Pre-65 individuals

Initial 5.0% 6.0%

Ultimate (2005) 4.5% 4.5%

Post-65 individuals

Initial 11.0% 12.0%

Ultimate (2010) 4.5% 4.5%

The Company’s discount rate is determined based upon the review of high quality corporate bond rates, the

change in these rates during the year, and year-end rate levels. Lowering the discount rate by 0.5 percent as

of December 31, 2003 would increase the Company’s pension and postretirement benefits liability by

approximately $532 million and $169 million, respectively, and increase estimated 2004 pension and

postretirement benefits expense by $66 million and $10 million, respectively.

The expected return on plan assets is based upon an evaluation of the Company's historical trends and

experience taking into account current and expected market conditions. The expected return on plan assets

component of the Company’s net periodic benefit cost is calculated based on the fair value of plan assets

and the Company’s target asset allocation of 40 percent longer duration corporate bonds, 25 percent U.S.

value stocks, 20 percent international stocks, five percent emerging markets stocks and bonds and 10

percent alternative (private) investments. The Company monitors its actual asset allocation and believes

that its long-term asset allocation will continue to approximate its target allocation. The Company’s historical

annualized ten-year rate of return on plan assets, calculated using a geometric compounding of monthly

returns, is approximately 10.5 percent as of December 31, 2003. Lowering the expected long-term rate of

return on plan assets by 0.5 percent as of December 31, 2003 would increase estimated 2004 pension

expense by approximately $32 million.

The health care cost trend rate is based upon an evaluation of the Company's historical trends and

experience taking into account current and expected market conditions. Increasing the assumed health

care cost trend rate by 1.0 percent would increase estimated 2004 postretirement benefits expense by $41

million.

The Company has pension and postretirement benefit unrecognized net actuarial losses as of December

31, 2003, of approximately $1.6 billion and $407 million, respectively. The unrecognized net actuarial losses

represent changes in the amount of the projected benefit obligation, the postretirement accumulated benefit

obligation and plan assets resulting from (i) changes in assumptions and (ii) actual experience differing from

assumptions. The amortization of unrecognized net actuarial loss component of the Company’s 2004

pension and postretirement benefit net periodic benefit costs are expected to be approximately $58 million

and $8 million, respectively. The Company’s total 2004 defined benefit pension expense and postretirement

expense is currently estimated to be approximately $428 million and $264 million (including the impact of the

Medicare legislation discussed in Note 10 to the consolidated financial statements), respectively.

The Company records an additional minimum pension liability when its accumulated benefit obligation

exceeds the pension plans’ assets in excess of amounts previously accrued for pension costs. As of

December 31, 2003, the Company’s additional minimum pension liability was $1.1 billion, down from $1.6

billion as of December 31, 2002, primarily as a result of significantly improved asset performance. The

decrease in the Company’s minimum pension liability resulted in a 2003 credit to equity of approximately

$337 million. An additional minimum pension liability is recorded as an increase to the pension liability, an

increase to other assets (to the extent that a plan has unrecognized prior service costs) and a charge to

stockholders’ equity as a component of Accumulated other comprehensive loss. See Note 10 to the

consolidated financial statements for additional information regarding the Company's pension and other

postretirement benefits.