American Airlines 2003 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2003 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

|

|

62

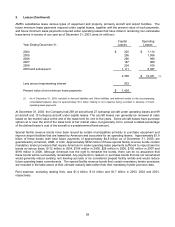

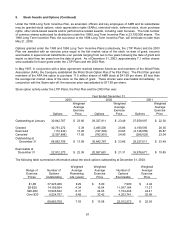

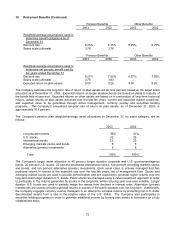

6. Indebtedness (Continued)

In 2002, the Regional Airports Improvement Corporation and the New York City Industrial Development Agency

issued facilities sublease revenue bonds at the Los Angeles International Airport and John F. Kennedy

International Airport, respectively, to provide reimbursement to American for certain facility construction and other

related costs. The Company has recorded the total amount of the issuances of $759 million (net of $38 million

discount) as long-term debt on the accompanying consolidated balance sheet as of December 31, 2002. These

obligations bear interest at fixed rates, with an average effective rate of 8.54 percent, and mature over various

periods of time, with a final maturity in 2028. The Company has received approximately $687 million in

reimbursements of certain facility construction and other related costs through December 31, 2003. Of the

remaining $72 million of bond issuance proceeds not yet received, classified as Other assets on the

accompanying consolidated balance sheet, $25 million are held by the trustee for reimbursement of future facility

construction costs and will be available to the Company in the future, and $47 million are held in a debt service

reserve fund.

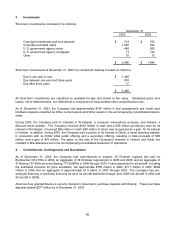

Certain debt is secured by aircraft, engines, equipment and other assets having a net book value of approximately

$12.6 billion.

As of December 31, 2003, AMR has issued guarantees covering approximately $932 million of American’s tax-

exempt bond debt and American has issued guarantees covering approximately $936 million of AMR’s unsecured

debt, including the 4.25 percent senior convertible notes discussed above. In addition, as of December 31, 2003,

AMR and American have issued guarantees covering approximately $503 million of AMR Eagle’s secured debt,

and AMR has issued guarantees covering an additional $1.9 billion of AMR Eagle’s secured debt.

Cash payments for interest, net of capitalized interest, were $661 million, $564 million and $343 million for 2003,

2002 and 2001, respectively.

In February 2004, American issued $180 million of Fixed Rate Secured Notes due 2009. These notes are

secured by certain spare parts and bear interest at 7.25 percent. Also in February 2004, AMR issued, and

American guaranteed, $324 million of 4.5 percent senior convertible notes due 2024.

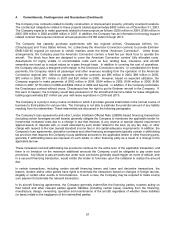

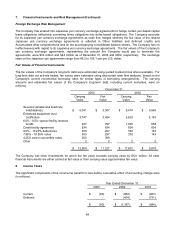

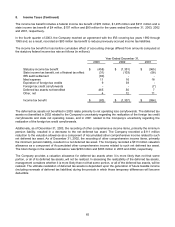

7. Financial Instruments and Risk Management

As part of the Company's risk management program, AMR uses a variety of financial instruments, including fuel

swap and option contracts and interest rate swaps. Prior to September 2002, the Company also used currency

option contracts and exchange agreements. The Company does not hold or issue derivative financial instruments

for trading purposes.

The Company is exposed to credit losses in the event of non-performance by counterparties to these financial

instruments, but it does not expect any of the counterparties to fail to meet its obligations. The credit exposure

related to these financial instruments is represented by the fair value of contracts with a positive fair value at the

reporting date, reduced by the effects of master netting agreements. To manage credit risks, the Company selects

counterparties based on credit ratings, limits its exposure to a single counterparty under defined guidelines, and

monitors the market position of the program and its relative market position with each counterparty. The Company

also maintains industry-standard security agreements with a number of its counterparties which may require the

Company or the counterparty to post collateral if the value of selected instruments exceed specified mark-to-

market thresholds or upon certain changes in credit ratings. The Company’s outstanding posted collateral as of

December 31, 2003 is included in restricted cash and short-term investments and is not material. The Company’s

credit rating has limited its ability to enter into certain types of fuel hedge contracts. A further deterioration of its

credit rating or liquidity position may negatively affect the Company’s ability to hedge fuel in the future.