American Airlines 2007 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2007 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

|

|

66

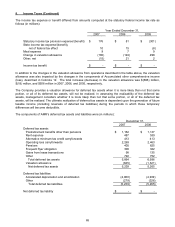

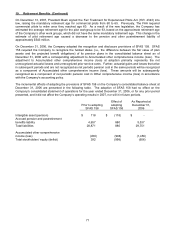

8. Income Taxes (Continued)

At December 31, 2007, the Company had available for federal income tax purposes an alternative minimum tax

credit carryforward of approximately $413 million, which is available for an indefinite period, and federal net

operating losses of approximately $6.6 billion for regular tax purposes, which will expire, if unused, beginning in

2022. These net operating losses include an SFAS123(R) unrealized benefit of approximately $647 million

related to the implementation of SFAS 123(R) that will be recorded in equity when realized. The Company had

available for state income tax purposes net operating losses of $3.7 billion, which expire, if unused, in years 2008

through 2026. The amount that will expire in 2008 is $93 million.

Cash payments for income taxes were $7 million, $1 million and $7 million for 2007, 2006 and 2005, respectively.

Under special tax rules (the Section 382 Limitation), cumulative stock purchases by material shareholders

exceeding 50 percent during a 3-year period can potentially limit a company’s future use of net operating losses

(NOL’s). Such limitation is increased by “built-in gains”, as provided by current IRS guidance. Based on available

information, the Company is not currently subject to the Section 382 Limitation. If triggered in a future period,

under current tax rules, such limitation is not expected to significantly impact the recorded value or timing of

utilization of AMR’s NOL's.

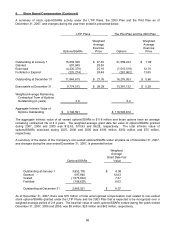

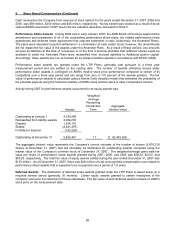

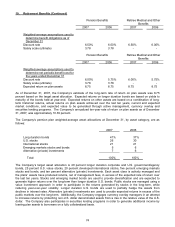

9. Share Based Compensation

AMR grants, or has granted, stock compensation under three plans: the Pilots Stock Option Plan (the Pilot Plan),

the 1998 Long Term Incentive Plan, and the 2003 Employee Stock Incentive Plan (the 2003 Plan). The Company

established the Pilot Plan in 1997 to grant members of the APA AMR stock options in conjunction with a prior

contract negotiation. The Pilot Plan expired in May of 2007.

Under the 1998 Long Term Incentive Plan, as amended, officers and key employees of AMR and its subsidiaries

may be granted certain types of stock or performance based awards. At December 31, 2007, the Company had

stock option/ settled stock appreciation right (SSAR) awards, performance share awards, deferred share awards

and other awards outstanding under this plan. The total number of common shares authorized for distribution

under the 1998 Long Term Incentive Plan is 23,700,000 shares. The 1998 Long Term Incentive Plan, the

successor to the 1988 Long Term Incentive Plan (collectively, the LTIP Plans), will terminate no later than May 21,

2008.

In 2003, the Company established the 2003 Plan to provide equity awards to employees. Under the 2003 Plan,

employees may be granted stock options/SSARs, restricted stock and deferred stock. At December 31, 2007, the

Company had stock options/SSARs and deferred awards outstanding under the 2003 Plan. The total number of

shares authorized for distribution under the 2003 Plan is 42,680,000 shares.

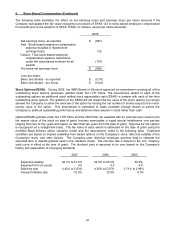

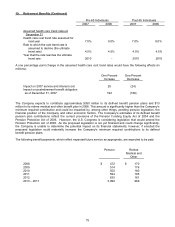

In 2007, 2006 and 2005, the total charge for share-based compensation expense included in wages, salaries and

benefits expense was $131 million, $219 million and $132 million, respectively. In 2007, 2006 and 2005, the

amount of cash used to settle equity instruments granted under share-based compensation plans was $11 million,

$29 million and $6 million, respectively.

Prior to January 1, 2006, the Company accounted for its share-based compensation plans in accordance with

Accounting Principles Board Opinion No. 25, “Accounting for Stock Issued to Employees” (APB 25) and related

Interpretations. Under APB 25, no compensation expense was recognized for stock option grants if the exercise

price of the Company’s stock option grants was at or above the fair market value of the underlying stock on the

date of grant. Effective January 1, 2006, the Company adopted the fair value recognition provisions of Statement

of Financial Accounting Standards No. 123(R), “Share-Based Payment” (SFAS 123(R)) using the modified-

prospective transition method. Under this transition method, compensation cost recognized in 2007 and 2006

includes: (a) compensation cost for all share-based payments granted prior to, but not yet vested as of January 1,

2006 based on the fair value used for pro forma disclosures and (b) compensation cost for all share-based

payments granted subsequent to January 1, 2006, based on the fair value estimated in accordance with the

provisions of SFAS 123(R). Results for prior periods have not been restated. The adoption of SFAS 123(R) did

not have a significant impact on the Company’s net income or basic and diluted amounts per share in 2006.