American Airlines 2007 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2007 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

|

|

71

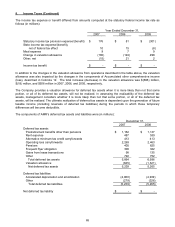

10. Retirement Benefits (Continued)

On December 13, 2007, President Bush signed the Fair Treatment for Experienced Pilots Act (H.R. 4343) into

law, raising the mandatory retirement age for commercial pilots from 60 to 65. Previously, The FAA required

commercial pilots to retire once they reached age 60. As a result of the new legislation, the Company has

estimated the average retirement age for the pilot workgroup to be 63, based on the approximate retirement age

of the Company’s other work groups, which did not have the same mandatory retirement age. This change in the

estimate of pilot retirement age caused a decrease to the pension and other postretirement liability of

approximately $543 million.

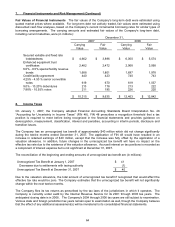

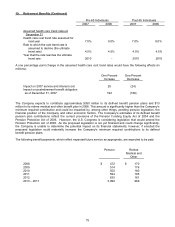

On December 31, 2006, the Company adopted the recognition and disclosure provisions of SFAS 158. SFAS

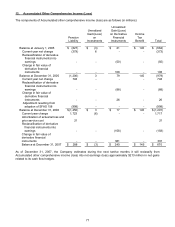

158 required the Company to recognize the funded status (i.e., the difference between the fair value of plan

assets and the projected benefit obligations) of its pension plans in the consolidated balance sheet as of

December 31, 2006 with a corresponding adjustment to Accumulated other comprehensive income (loss). The

adjustment to Accumulated other comprehensive income (loss) at adoption primarily represents the net

unrecognized actuarial losses and unrecognized prior service costs. Further, actuarial gains and losses that arise

in subsequent periods and are not recognized as net periodic pension cost in the same periods will be recognized

as a component of Accumulated other comprehensive income (loss). These amounts will be subsequently

recognized as a component of net periodic pension cost in Other comprehensive income (loss) in accordance

with the Company’s accounting policy.

The incremental effects of adopting the provisions of SFAS 158 on the Company’s consolidated balance sheet at

December 31, 2006 are presented in the following table. The adoption of SFAS 158 had no effect on the

Company’s consolidated statement of operations for the year ended December 31, 2006, or for any prior period

presented, and it did not affect the Company’s operating results in 2007, nor will it in future periods.

Prior to adopting

SFAS 158

Effect of

adopting

SFAS 158

As Reported at

December 31,

2006

Intangible asset (pension) $ 118 $ (118) $ -

Accrued pension and postretirement

benefits liability

4,657

880

5,537

Total liabilities 28,871 880 29,751

Accumulated other comprehensive

income (loss)

(458)

(998)

(1,456)

Total stockholders’ equity (deficit) 392 (998) (606)