Kohl's 2008 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2008 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

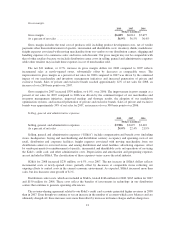

Capital expenditures include costs for new store openings, store remodels, distribution center openings and

other base capital needs. Capital expenditures totaled $1.0 billion for 2008, a $528 million decrease from 2007.

This decrease is primarily due to a decrease in the number of new store openings in 2008 compared to 2007. We

opened 75 stores in 2008 compared to 112 stores in 2007. Total capital expenditures for fiscal 2009 are expected

to be approximately $800 million. The actual amount of our future capital expenditures will depend primarily on

the number of new stores opened, the mix of owned, leased or acquired stores, the number of stores remodeled

and the timing of distribution center openings. We do not anticipate that our expansion plans will be limited by

any restrictive covenants in our financing agreements. We believe that our capital structure is well positioned to

support our expansion plans. We anticipate that internally generated cash flows will be the primary source of

funding for future growth.

Capital expenditures, including favorable lease rights, by major category were as follows:

2008 2007 2006

New stores ....................................................... 68% 77% 76%

Remodels / relocations .............................................. 12 62

Distribution centers ................................................ 436

Other ............................................................ 16 14 16

Acquisition of property and equipment and favorable lease rights ............ 100% 100% 100%

Net cash used in investing activities increased $128 million for 2007 compared to 2006. The increase

reflects higher capital expenditures, partially offset by the net impact of short-term investing activities. Net short-

term investment activity resulted in a use of funds of $52 million in 2007 and $270 million in 2006. Net short-

term investment activity reflects investment funds used to purchase treasury stock and the investment of proceeds

from the $1 billion of new debt issued in September 2007 and the sale of our private label credit card portfolio in

2006. Capital expenditures totaled $1.5 billion for 2007, a $379 million increase over 2006 primarily due to an

increase in the number of stores opened and an increase in the number of remodels.

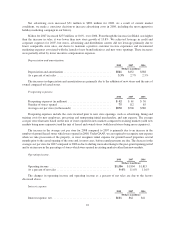

Financing activities.

Our financing activities used cash of $273 million in 2008 and provided cash of $325 million in 2007. The

change reflects the proceeds from issuance of debt in 2007 and lower treasury stock repurchases in 2008.

We have various facilities upon which we may draw funds, including a $900 million senior unsecured

revolving facility and two demand notes with aggregate availability of $50 million. The $900 million revolving

facility expires in October 2011. The co-leads of this facility, The Bank of New York Mellon and Bank of

America, have each committed $100 million. The remaining 12 lenders have each committed between $30 and

$130 million.

We had no amounts outstanding on our lines of credit at either year-end 2008 or year-end 2007. Average

borrowings under these facilities were $40 million for 2008, $63 million for 2007 and $19 million for 2006. The

decrease from 2007 to 2008 reflects decreased cash needs due to lower inventory levels, capital expenditures and

stock repurchases.

Our credit ratings have been unchanged since September 2007 when we issued $1 billion in debt. Our

ratings are currently as follows:

Moody’s

Standard

& Poor’s Fitch

Long-term debt .................................... Baa1 BBB+ BBB+

25