Kohl's 2008 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2008 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

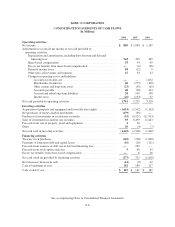

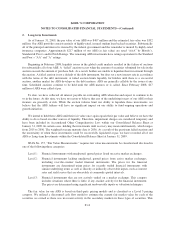

KOHL’S CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

1. Business and Summary of Accounting Policies (continued)

Preopening Costs

Preopening expenses relate to the costs associated with new store openings, including advertising, hiring

and training costs for new employees, processing and transporting initial merchandise and rent expense.

Preopening costs are expensed as incurred.

Income Taxes

Income taxes are accounted for under the asset and liability method. Under this method, deferred tax assets

and liabilities are recorded based on differences between the amounts of assets and liabilities recognized for

financial reporting purposes and such amounts recognized for income tax purposes. Deferred tax assets and

liabilities are calculated using the enacted tax rates and laws that are expected to be in effect when the differences

are expected to reverse. We establish valuation allowances for tax benefits when we believe it is more likely than

not that the related expense will be deductible for tax purposes.

On February 4, 2007, we adopted Financial Accounting Standards Board (“FASB”) Interpretation No. 48,

“Accounting for Uncertainty in Income Taxes—an interpretation of FASB Statement No. 109” (“FIN 48”),

which clarifies the accounting and disclosure for uncertainty in tax positions, as defined. FIN 48 seeks to reduce

the diversity in practice associated with certain aspects of the recognition and measurement related to accounting

for income taxes. Our liability for unrecognized tax benefits was not impacted by the implementation of FIN 48.

We recognize interest and penalty expense related to unrecognized tax benefits in our provision for income

tax expense.

Net Income Per Share

Basic net income per share is net income divided by the average number of common shares outstanding

during the period. Diluted net income per share includes incremental shares assumed to be issued upon exercise

of stock options.

The information required to compute basic and diluted net income per share is as follows:

2008 2007 2006

(In Millions except per share data)

Numerator—net income ....................................... $ 885 $1,084 $1,109

Denominator—weighted average shares

Basic .................................................. 306 318 332

Impact of dilutive employee stock options (a) .................. 123

Diluted ................................................ 307 320 335

Net income per share:

Basic .................................................. $2.89 $ 3.41 $ 3.34

Diluted ................................................ $2.89 $ 3.39 $ 3.31

(a) Excludes 18 million options for 2008, 9 million options for 2007 and 8 million options for 2006 as the

impact of such options was antidilutive.

F-12