Kohl's 2008 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2008 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

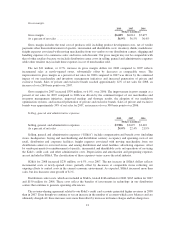

gross margins are calculated by applying a cost-to-retail ratio to the retail value of the inventories. The use of

RIM will result in inventories being valued at the lower of cost or market as markdowns are currently taken as a

reduction of the retail value of inventories.

Based on a review of historical clearance markdowns, current business trends, expected vendor funding and

discontinued merchandise categories, an adjustment to inventory is recorded to reflect additional markdowns

which are estimated to be necessary to liquidate existing clearance inventories and reduce inventories to the

lower of cost or market. Management believes that our inventory valuation approximates the net realizable value

of clearance inventory and results in carrying inventory at the lower of cost or market.

Vendor Allowances

We record vendor allowances and discounts in the income statement when the purpose for which those

monies were designated is fulfilled. Allowances provided by vendors generally relate to profitability of inventory

recently sold and, accordingly, are reflected as reductions to cost of merchandise sold as negotiated. Vendor

allowances will fluctuate based on the amount of promotional and clearance markdowns necessary to liquidate

the inventory. Vendor allowances received for advertising or fixture programs reduce our expense or expenditure

for the related advertising or fixture program when appropriate. See also Note 1 to the consolidated financial

statements, “Business and Summary of Accounting Policies.”

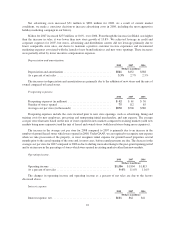

Insurance Reserve Estimates

We use a combination of insurance and self-insurance for a number of risks including workers’

compensation, general liability and employee-related health care benefits, a portion of which is paid by our

associates. We use a third-party actuary, which considers historical claims experience, demographic factors,

severity factors and other actuarial assumptions, to estimate the liabilities associated with these risks. A change in

claims frequency and severity of claims from historical experience as well as changes in state statutes and the

mix of states in which we operate could result in a change to the required reserve levels. We retain the initial risk

of $500,000 per occurrence under our workers’ compensation insurance policy and $250,000 per occurrence

under our general liability policy. We also have a lifetime medical payment limit of $1.5 million.

Impairment of Assets and Closed Store Reserves

We have a significant investment in property and equipment and favorable lease rights. The related

depreciation and amortization is computed using estimated useful lives of up to 50 years. We review our long-

lived assets held for use (including favorable lease rights) for impairment whenever an event or change in

circumstances, such as decisions to close a store, indicates the carrying value of the asset may not be recoverable.

We have historically not experienced any significant impairment of long-lived assets or closed store reserves.

Decisions to close a store can also result in accelerated depreciation over the revised useful life. When operations

at a leased store are discontinued, a reserve is established for the discounted difference between the rent and the

expected sublease rental income. A significant change in cash flows, market valuation, demand for real estate or

other factors, could result in an increase or decrease in the reserve requirement or impairment charge.

Income Taxes

We pay income taxes based on tax statutes, regulations and case law of the various jurisdictions in which we

operate. At any one time, multiple tax years are subject to audit by the various taxing authorities. Our effective

income tax rate was 37.9% in 2008, 37.8% in 2007 and 37.5% in 2006. The effective rate is impacted by changes

in law, location of new stores, level of earnings and the result of tax audits.

Operating Leases

As of January 31, 2009, we leased 641 of our 1,004 retail stores. Many lease agreements contain rent

holidays, rent escalation clauses and/or contingent rent provisions. We recognize rent expense on a straight-line

basis over the expected lease term, including cancelable option periods where failure to exercise such options

would result in an economic penalty. We use a time period for our straight-line rent expense calculation that

equals or exceeds the time period used for depreciation. In addition, the commencement date of the lease term is

29