LabCorp 2013 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2013 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

|

|

12

LABORATORY CORPORATION OF AMERICA

Management’s Discussion and Analysis

of Financial Condition and Results of Operations (in millions)

The Company has discussed its intention to increase its ratio of

total debt to consolidated Earnings Before Interest, Taxes, Depreciation,

and Amortization (“EBITDA”) over time from 2.0 to 1.0 as of

December 2012 to 2.5 to 1.0. The Company believes that it can

achieve this through the use of its Revolving Credit Facility and its

ready access to debt capital markets. As of December 31, 2013,

the ratio of total debt to consolidated EBITDA was 2.4 to 1.0. The

Company continues to monitor the debt capital markets and,

given current market conditions, believes it can readily increase its

ratio of total debt to consolidated EBITDA. The Company believes

that its cash from operations, in combination with cash on hand

and borrowing capacity, will be sufficient to satisfy its obligations

in 2014 and beyond.

Operating Activities

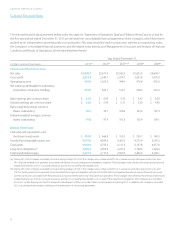

In 2013, the Company’s operations provided $818.7 of cash,

reflecting the Company’s solid business results. The decrease in

cash provided from operations in 2013 as compared with 2012

is primarily attributable to the delays and denials of coverage

for existing tests by some payers after implementation of newly

established molecular pathology codes as well as government

payment reductions. These delays, denials and government

reductions reduced year over year operating cash flow by more

than an estimated $100.0. The Company continues to focus on

efforts to increase cash collections from all payers and to generate

ongoing improvements to the claim submission processes.

In 2012, the Company’s operations provided $841.4 of cash,

reflecting the Company’s solid business results. The Company

continued to focus on efforts to increase cash collections from

all payers and to generate ongoing improvements to the claim

submission processes.

Investing Activities

Capital expenditures were $202.2, $173.8 and $145.7 for 2013, 2012

and 2011, respectively. The increase in capital spending in 2013

was related to certain integration and cost savings initiatives started

by the Company. The Company expects capital expenditures

of approximately $185.0 to $205.0 in 2014. Such expenditures are

expected to be funded by cash flow from operations, as well

as borrowings under the Company’s Revolving Credit Facility

as needed.

The Company remains committed to growing its business

through strategic acquisitions and licensing agreements. The

Company has invested a total of $632.9 over the past three years

in strategic business acquisitions, including MEDTOX Scientific in

2012 and Orchid in 2011. These acquisitions have helped strengthen

the Company’s geographic presence along with expanding

capabilities in the specialty testing operations. The Company

believes the acquisition market remains attractive with a number of

opportunities to strengthen its scientific capabilities, grow esoteric

testing capabilities and increase presence in key geographic areas.

The Company has invested a total of $2.9 over the past three years

in licensing new testing technologies and had $41.0 net book value

of capitalized patents, licenses and technology as of December 31,

2013. While the Company continues to believe its strategy of

entering into licensing and technology distribution agreements

with the developers of leading-edge technologies will provide

future growth in revenues, there are certain risks associated with

these investments. These risks include, but are not limited to, the

failure of the licensed technology to gain broad acceptance in

the marketplace and/or that insurance companies, managed care

organizations, or Medicare and Medicaid will not approve

reimbursement for these tests at a level commensurate with

the costs of running the tests. Any or all of these circumstances

could result in impairment in the value of the related capitalized

licensing costs.

Financing Activities

On December 21, 2011, the Company entered into a Credit

Agreement (the “Credit Agreement”) providing for the Revolving

Credit Facility, a five-year $1,000.0 senior unsecured revolving credit

facility with Bank of America, N.A., acting as Administrative Agent,

Barclays Capital as Syndication Agent, and a group of financial

institutions as lending parties. As part of the new Revolving Credit

Facility, the Company repaid all of the outstanding principal balances

of $318.8 on its existing term loan facility and $235.0 on its existing

revolving credit facility. In conjunction with the repayment and

cancellation of its old credit facility, the Company recorded

approximately $1.0 of remaining unamortized debt costs as

interest expense in the accompanying Consolidated Statements

of Operations for the year ended December 31, 2011.

There were no balances outstanding on the Company’s

Revolving Credit Facility at December 31, 2013 or December 31,

2012. The Revolving Credit Facility bears interest at varying rates

based upon a base rate or LIBOR plus (in each case) a percentage

based on the Company’s debt rating with Standard & Poor’s and

Moody’s Rating Services.