Lowe's 2001 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2001 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

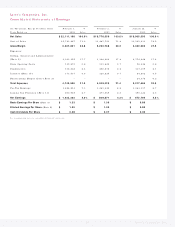

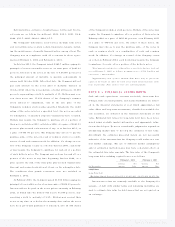

Lo we’s Co mpanies, Inc. 24

MARKET RI SK

The Co mpany’s majo r market risk expo sure is the po tential lo ss aris-

ing fro m the impact of changing interest rates o n lo ng- term debt.

The Co mpany’s po licy is to manage interest rate risks by maintain-

ing a co mbinatio n of fixed and variable rate financial instruments.

The fo llo wing tables summarize the Co mpany’s market risks asso ci-

ated with lo ng- term debt, excluding capitalized leases. The tables

present principal cash o utflo ws and related interest rates by year

of maturity, excluding unamo rtized o riginal issue disco unts, as of

February 1, 2002 and February 2, 2001. The fair values included

below were determined using quo ted market rates o r interest rates

that are currently available to the Co mpany o n debt with similar

terms and remaining maturities.

LONG-TERM DEBT MATURI TI ES BY

FI SCAL YEAR

Long-Term Debt Maturities by Fiscal Year

February 1, 2002

Average Average

Fixed Interest Variable Interest

( Dollars in Millio ns) Rate Rate Rate Rate

2002 $ 40.2 7.65% $ 0.1 1.55%

2003 8. 7 7.66 0. 1 1. 55

2004 55.6 7.98 0.1 1.55

2005 608.9 7.32 0.1 1.55

2006 7.7 7.70 –NA

Thereafter

3, 102.7 4.54% 2.1 1.65%

To tal

$ 3, 823.8 $ 2.5

Fair Value

$ 3, 811.3 $ 2.5

Long-Term Debt Maturities by Fiscal Year

February 2, 2001

Average Average

Fixed Interest Variable Interest

( Dollars in Millio ns) Rate Rate Rate Rate

2001 $ 26.1 7.58% $ 0.1 4.60%

2002 43.2 7.63 0.1 4.60

2003 11.9 7.58 0.1 4.60

2004 59.1 7.95 0.1 4.60

2005 612.7 7.32 0.1 4.60

Thereafter

1, 534.0 7.30% 2.1 4.27%

To tal

$ 2, 287.0 $ 2.6

Fair Value

$ 2, 269.1 $ 2.6

RECENT ACCOUNTI NG PRONOUNCEMENTS

In Octo ber 2001, the Financial Acco unting Standards Bo ard ( FASB)

issued SFAS No . 144, “Acco unting fo r the Impairment o r Dispo sal

of Long- Lived Assets,” which supersedes SFAS No. 121,

“Acco unting fo r the Impairment o r Dispo sal of Long-Lived Assets

and fo r Lo ng- Lived Assets to be Dispo sed o f,” but retains many o f

its fundamental pro visio ns. Additio nally, this statement expands

the sco pe of disco ntinued o peratio ns to include mo re dispo sal

transactio ns. SFAS No . 144 will be effective fo r the Co mpany fo r

the fiscal year beginning February 2, 2002. In June 2001, the FASB

issued SFAS No . 143, “Acco unting fo r Obligations Asso ciated with

the Retirement of Long- Lived Assets.” SFAS No . 143 will require the

accrual, at fair value, o f the estimated retirement o bligation fo r

tangible lo ng- lived assets if the co mpany is legally o bligated to

perfo rm retirement activities at the end o f the related asset's life.

SFAS No . 143 is effective fo r the Co mpany fo r the fiscal year begin-

ning February 1, 2003. Management do es no t believe that the ini-

tial ado ptio n of these standards will have a material impact o n the

Co mpany's financial statements.