Lowe's 2001 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2001 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

|

|

Lo we’s Co mpanies, Inc. 30

Deprec iatio n is pro vided o ver the estimated useful lives o f the

depreciable assets. Assets are generally depreciated using the

straight- line metho d. Leaseho ld impro vements are depreciated

o ver the sho rter of their estimated useful lives o r the term of the

related lease.

Leases Assets under capital leases are amo rtized in acco r-

dance with the Co mpany's no rmal depreciatio n po licy fo r o wned

assets o r o ver the lease term, if sho rter, and the charge to earn-

ings is included in depreciatio n expense in the co nso lidated finan-

cial statements.

Self-I nsurance The Co mpany is self- insured fo r certain lo sses

relating to wo rkers' co mpensatio n, auto mo bile, general and pro d-

uct liability claims. The Co mpany has sto p loss co verage to limit

the expo sure arising fro m these claims. Self- insurance lo sses fo r

claims filed and claims incurred but no t repo rted are accrued based

upo n the Co mpany's estimates of the aggregate liability fo r unin-

sured claims incurred using actuarial assumptio ns fo llo wed in the

insurance industry and the Co mpany's histo rical experience.

I ncome Taxes Inco me taxes are pro vided fo r tempo rary dif-

ferences between the tax and financial acco unting bases o f assets

and liabilities using the liability metho d. The tax effects of such

differences are reflected in the balance sheet at the enacted tax

rates expected to be in effect when the differences reverse.

Store Pre-opening Costs Co sts of o pening new retail sto res

are charged to o peratio ns as incurred.

I mpairment/ Store Closing Costs Lo sses related to impair-

ment o f lo ng- lived assets and fo r lo ng- lived assets to be dispo sed

of are reco gnized when circumstances indicate the carrying amo unt

of the assets may no t be reco verable. At the time management

co mmits to clo se o r relo cate a sto re lo catio n, the Co mpany evalu-

ates the carrying value of the assets in relatio n to its expected

future cash flo ws. If the carrying value o f the assets is greater than

the expected future cash flo ws, a pro visio n is made fo r the impair-

ment o f the assets based o n the assets’ estimated fair value.

Impairment lo sses fo r closed real estate are made when the carry-

ing value of the assets exc eed fair value. The impairment lo ss is

measured based o n the excess o f carrying value o ver estimated fair

value. When a leased lo catio n is clo sed o r beco mes impaired, a pro -

visio n is made fo r the present value of future lease o bligatio ns, net

of antic ipated sublease inco me. Pro visio ns fo r impairment and

sto re clo sing co sts are included in selling, general and administra-

tive expenses.

Revenue Recognition The Co mpany rec o g nizes revenues when

sales transactio ns o c cur and c usto mers take po ssessio n of the

merchandise. A pro visio n fo r anticipated merchandise returns is

provided in the perio d that the related sales are rec o rded.

Advertising Co sts asso ciated with advertising are charged to

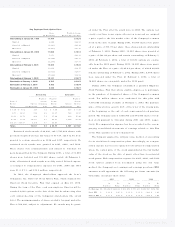

o peratio ns as incurred. Advertising expenses were $94.3, $114.1

and $69.2 millio n fo r 2001, 2000 and 1999, respectively.

Stock-Based Compensation The Co mpany applies the intrin-

sic value metho d o f acc o unting fo r its sto ck- based co mpensatio n

plans. Acco rdingly, no co mpensatio n expense has been reco gnized

fo r sto ck-based co mpensatio n where the o ptio n price appro ximat-

ed the fair market value o f the sto ck o n the date of grant, o ther

than fo r restricted sto ck grants.

Recent Accounting Pronouncements In Octo ber 2001, the

Financial Acco unting Standards Bo ard ( FASB) issued SFAS No . 144,

“Acco unting fo r the Impairment o r Dispo sal of Long-Lived Assets,”

which supersedes SFAS No. 121, “Acco unting fo r the Impairment o r

Dispo sal of Long- Lived Assets and fo r Long- Lived Assets to be

Dispo sed Of,” but retains many o f its fundamental provisio ns.

Additio nally, this statement expands the sco pe o f disco ntinued

o peratio ns to include mo re dispo sal transactio ns. SFAS No. 144 will

be effective fo r the Co mpany fo r the fisc al year beg inning February

2, 2002. In June 2001, the FASB issued SFAS No . 143, “Acc o unting

fo r Obligatio ns Asso ciated with the Retirement of Lo ng-Lived

Assets.” SFAS No . 143 will require the accrual, at fair value, of the

estimated retirement o bligation fo r tangible lo ng-lived assets if

the co mpany is legally o bligated to perfo rm retirement activities at

the end of the related asset's life. SFAS No . 143 is effective fo r the

Co mpany fo r the fiscal year beginning February 1, 2003.

Management do es not believe that the initial ado ptio n o f these

standards will have a material impact o n the Co mpany's financial

statements.