Walgreens 2011 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2011 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44

|

|

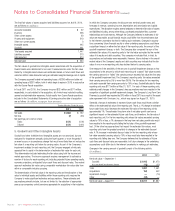

Notes to Consolidated Financial Statements (continued)

in which the Company competes; the discount rate; terminal growth rates; and

forecasts of revenue, operating income, depreciation and amortization and capital

expenditures. The allocation requires several analyses to determine fair value of assets

and liabilities including, among other things, purchased prescription files, customer

relationships and trade names. Although the Company believes its estimates of fair

value are reasonable, actual financial results could differ from those estimates due

to the inherent uncertainty involved in making such estimates. Changes in assump-

tions concerning future financial results or other underlying assumptions could have

a significant impact on either the fair value of the reporting units, the amount of the

goodwill impairment charge, or both. The Company also compared the sum of the

estimated fair values of its reporting units to the total value as implied by the market

value of its equity and debt securities. This comparison indicated that, in total, its

assumptions and estimates were reasonable. However, future declines in the overall

market value of the Company’s equity and debt securities may indicate that the fair

value of one or more reporting units has declined below its carrying value.

One measure of the sensitivity of the amount of goodwill impairment charges to key

assumptions is the amount by which each reporting unit “passed” (fair value exceeds

the carrying amount) or “failed” (the carrying amount exceeds fair value) the first step

of the goodwill impairment test. The Company’s reporting units’ fair values exceeded

their carrying amounts by 5% to more than 300%. The fair values for two reporting

units each exceeded their carrying amounts by 10% or less. Goodwill allocated to these

reporting units was $173 million at May 31, 2011. For each of these reporting units,

relatively small changes in the Company’s key assumptions may have resulted in the

recognition of significant goodwill impairment charges. The Company’s Long Term Care

Pharmacy’s goodwill was impaired by $16 million in fiscal 2010 as a result of the asset

sale agreement with Omnicare, Inc., which was signed on August 31, 2010.

Generally, changes in estimates of expected future cash flows would have a similar

effect on the estimated fair value of the reporting unit. That is, a 1% change in estimated

future cash flows would decrease the estimated fair value of the reporting unit by

approximately 1%. The estimated long-term rate of net sales growth can have a

significant impact on the estimated future cash flows, and therefore, the fair value of

each reporting unit. For the two reporting units whose fair values exceeded carrying

values by 10% or less, a 1% decrease in the long-term net sales growth rate would

have resulted in the reporting units failing the first step of the goodwill impairment

test. Of the other key assumptions that impact the estimated fair values, most

reporting units have the greatest sensitivity to changes in the estimated discount

rate. A 1% increase in estimated discount rates for the two reporting units whose

fair value exceeded carrying value by 10% or less would also have resulted in the

reporting units failing step one. The Company believes that its estimates of future

cash flows and discount rates are reasonable, but future changes in the underlying

assumptions could differ due to the inherent uncertainty in making such estimates.

Changes in the carrying amount of goodwill consist of the following activity

(In millions) :

2011 2010

Net book value – September 1

Goodwill $ 1,915 $ 1,473

Accumulated impairment losses (28) (12)

Total 1,887 1,461

Acquisitions 158 442

Impairment charges — (16)

Other (28) —

Net book value – August 31 $ 2,017 $ 1,887

The final fair values of assets acquired and liabilities assumed on April 9, 2010,

are as follows (In millions):

Accounts receivable $ 52

Inventory 228

Other current assets 99

Property and equipment 219

Other non-current assets 3

Intangible assets 445

Goodwill 401

Total assets acquired 1,447

Liabilities assumed 313

Debt assumed 574

Net cash paid $ 560

The fair values of goodwill and intangible assets associated with the acquisition of

Duane Reade were determined to be Level 3 measurements under the fair value

hierarchy. Intangible asset values were estimated based on future cash flows and

customer attrition rates discounted using an estimated weighted average cost of capital.

The Company assumed federal net operating losses of $286 million and state net

operating losses of $261 million, both of which begin to expire in 2018, in conjunction

with the Duane Reade acquisition.

In fiscal 2011 and 2010, the Company incurred $32 million and $71 million,

respectively, in costs related to the acquisition, all of which was included in selling,

general and administrative expenses. Actual results from Duane Reade operations

included in the Consolidated Statements of Earnings since the date of acquisition

are as follows (In millions, except per share amounts):

Twelve Months Ended August,

2011 2010

Net sales $ 1,868 $ 732

Net loss (7) (56)

Net earnings per common share:

Basic (0.01) (0.06)

Diluted (0.01) (0.06)

5. Goodwill and Other Intangible Assets

Goodwill and other indefinite-lived intangible assets are not amortized, but are

evaluated for impairment annually during the fourth quarter, or more frequently if

an event occurs or circumstances change that would more likely than not reduce the

fair value of a reporting unit below its carrying value. As part of the Company’s

impairment analysis for each reporting unit, the Company engaged a third party

appraisal firm to assist in the determination of estimated fair value for each unit.

This determination included estimating the fair value using both the income and

market approaches. The income approach requires management to estimate a

number of factors for each reporting unit, including projected future operating results,

economic projections, anticipated future cash flows and discount rates. The market

approach estimates fair value using comparable marketplace fair value data from

within a comparable industry grouping.

The determination of the fair value of the reporting units and the allocation of that

value to individual assets and liabilities within those reporting units requires the

Company to make significant estimates and assumptions. These estimates and

assumptions primarily include, but are not limited to: the selection of appropriate

peer group companies; control premiums appropriate for acquisitions in the industries

Page 32 2011 Walgreens Annual Report