Walgreens 2012 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2012 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

|

|

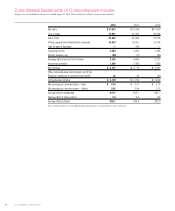

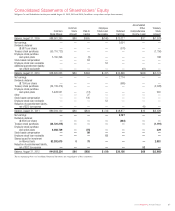

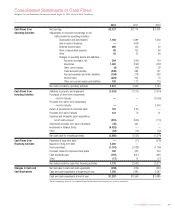

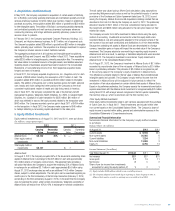

30 2012 Walgreens Annual Report

1. Summary of Major Accounting Policies

Description of Business

The Company is principally in the retail drugstore business and its operations are

within one reportable segment. At August 31, 2012, there were 8,385 drugstore

and other locations in all 50 states, the District of Columbia, Guam and Puerto Rico.

Prescription sales were 63.2% of total sales for fiscal 2012 compared to 64.7%

in 2011 and 65.2% in 2010.

Basis of Presentation

The consolidated financial statements include the accounts of the Company and its

subsidiaries. All intercompany transactions have been eliminated. The consolidated

financial statements are prepared in accordance with accounting principles generally

accepted in the United States of America and include amounts based on management’s

prudent judgments and estimates. Actual results may differ from these estimates.

Cash and Cash Equivalents

Cash and cash equivalents include cash on hand and all highly liquid investments

with an original maturity of three months or less. Credit and debit card receivables

from banks, which generally settle within two business days, of $88 million and $83

million were included in cash and cash equivalents at August 31, 2012 and 2011,

respectively. At August 31, 2012 and 2011, the Company had $820 million and

$1,239 million, respectively, in money market funds, all of which was included in

cash and cash equivalents.

The Company’s cash management policy provides for controlled disbursement.

As a result, the Company had outstanding checks in excess of funds on deposit

at certain banks. These amounts, which were $256 million at August 31, 2012,

and $229 million at August 31, 2011, are included in trade accounts payable

in the accompanying Consolidated Balance Sheets.

In fiscal 2011, the Company held $191 million in restricted cash to support certain

insurance obligations. In fiscal 2012, the restricted cash was released and the

obligations were supported by issued letters of credit.

Inventories

Inventories are valued on a lower of last-in, first-out (LIFO) cost or market basis.

At August 31, 2012 and 2011, inventories would have been greater by $1,897 million

and $1,587 million, respectively, if they had been valued on a lower of first-in,

first-out (FIFO) cost or market basis. As a result of declining inventory levels,

the fiscal 2012 LIFO provision was reduced by $268 million of LIFO liquidation.

Inventory includes product costs, inbound freight, warehousing costs and vendor

allowances not classified as a reduction of advertising expense.

Equity Method Investments

The Company uses the equity method to account for investments in companies if

the investment provides the ability to exercise significant influence, but not control,

over operating and financial policies of the investee. The Company’s proportionate

share of the net income or loss of these companies is included in consolidated

net earnings. Judgment regarding the level of influence over each equity method

investment includes considering key factors such as the Company’s ownership

interest, representation on the board of directors, participation in policy-making

decisions and material intercompany transactions.

Property and Equipment

Depreciation is provided on a straight-line basis over the estimated useful lives of

owned assets. Leasehold improvements and leased properties under capital leases

are amortized over the estimated useful life of the property or over the term of the

lease, whichever is shorter. Estimated useful lives range from 10 to 39 years for

land improvements, buildings and building improvements; and 2 to 13 years for

equipment. Major repairs, which extend the useful life of an asset, are capitalized;

routine maintenance and repairs are charged against earnings. The majority of the

business uses the composite method of depreciation for equipment. Therefore,

gains and losses on retirement or other disposition of such assets are included

in earnings only when an operating location is closed, completely remodeled or

impaired. Fully depreciated property and equipment are removed from the cost

and related accumulated depreciation and amortization accounts.

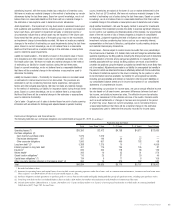

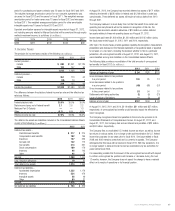

Property and equipment consists of (In millions) :

2012 2011

Land and land improvements

Owned locations $ 3,189 $ 3,209

Distribution centers 96 96

Other locations 232 240

Buildings and building improvements

Owned locations 3,684 3,651

Leased locations (leasehold improvements only) 1,518 1,235

Distribution centers 608 596

Other locations 525 372

Equipment

Locations 4,995 4,468

Distribution centers 1,158 1,098

Other locations 586 423

Capitalized system development costs 420 328

Capital lease properties 149 118

17,160 15,834

Less: accumulated depreciation and amortization 5,122 4,308

$ 12,038 $ 11,526

Depreciation expense for property and equipment was $841 million in fiscal 2012,

$809 million in fiscal 2011 and $804 million in fiscal 2010.

The Company capitalizes application stage development costs for significant

internally developed software projects, such as upgrades to the store point-of-sale

system. These costs are amortized over a five-year period. Amortization

expense was $70 million in fiscal 2012, $58 million in fiscal 2011 and

$44 million in fiscal 2010. Unamortized costs at August 31, 2012 and 2011,

were $292 million and $230 million, respectively.

Goodwill and Other Intangible Assets

Goodwill represents the excess of the purchase price over the fair value of assets

acquired and liabilities assumed. The Company accounts for goodwill and intangibles

under ASC Topic 350, Intangibles – Goodwill and Other, which does not permit

amortization, but requires the Company to test goodwill and other indefinite-lived

assets for impairment annually or whenever events or circumstances indicate

impairment may exist.

Impaired Assets and Liabilities for Store Closings

The Company tests long-lived assets for impairment whenever events or circum-

stances indicate that a certain asset may be impaired. Store locations that have

been open at least five years are reviewed for impairment indicators at least annually.

Once identified, the amount of the impairment is computed by comparing the

carrying value of the assets to the fair value, which is based on the discounted

estimated future cash flows. Impairment charges included in selling, general and

administrative expenses were $27 million in fiscal 2012, $44 million in fiscal

2011 and $17 million in fiscal 2010.

The Company also provides for future costs related to closed locations. The liability

is based on the present value of future rent obligations and other related costs

(net of estimated sublease rent) to the first lease option date. The reserve for store

closings was $117 million, $145 million and $151 million in fiscal 2012, 2011 and

2010, respectively. See Note 3 for additional disclosure regarding the Company’s

reserve for future costs related to closed locations.

Financial Instruments

The Company had $157 million and $143 million of outstanding letters of credit at

August 31, 2012 and 2011, respectively, which guarantee the purchase of foreign

goods, and additional outstanding letters of credit of $38 million and $40 million at

August 31, 2012 and 2011, respectively, which guarantee payments of insurance

claims. The insurance claim letters of credit are annually renewable and will remain

in place until the insurance claims are paid in full. Letters of credit of $229 million

and $13 million were outstanding at August 31, 2012, and August 31, 2011,

Notes to Consolidated Financial Statements