Walgreens 2012 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2012 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48

|

|

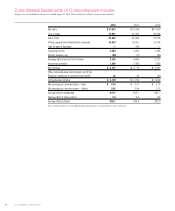

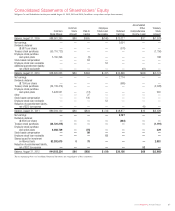

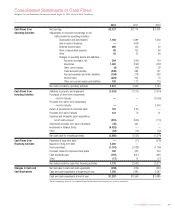

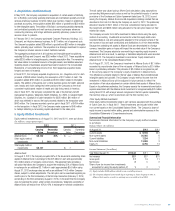

Notes to Consolidated Financial Statements (continued)

36 2012 Walgreens Annual Report

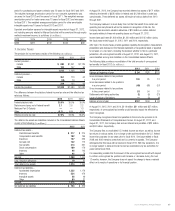

8. Short-Term Borrowings and Long-Term Debt

Short-term borrowings and long-term debt consists of the following

at August 31 (In millions) :

2012 2011

Short-Term Borrowings –

Current maturities of loans assumed through

the purchase of land and buildings; various

interest rates from 5.00% to 8.75%;

various maturities from 2013 to 2035 $ 9 $ 8

4.875% unsecured notes due 2013 net of

unamortized discount and interest rate swap

fair market value adjustment (see Note 9) 1,305 —

Other 5 5

Total short-term borrowings $ 1,319 $ 13

Long-Term Debt –

4.875% unsecured notes due 2013 net of

unamortized discount and interest rate swap

fair market value adjustment (see Note 9) $ — $ 1,339

5.250% unsecured notes due 2019 net of

unamortized discount and interest rate swap

fair market value adjustment (see Note 9) 1,030 1,011

Bridge Facility (see Note 16) 3,000 —

Loans assumed through the purchase of land and buildings;

various interest rates from 5.00% to 8.75%; various

maturities from 2013 to 2035 52 54

4,082 2,404

Less current maturities (9) (8)

Total long-term debt $ 4,073 $ 2,396

On July 17, 2008, the Company issued notes totaling $1.3 billion bearing an interest

rate of 4.875% paid semiannually in arrears on February 1 and August 1 of each

year, beginning on February 1, 2009. The notes will mature on August 1, 2013.

The Company may redeem the notes, at any time in whole or from time to time in

part, at its option at a redemption price equal to the greater of: (1) 100% of the

principal amount of the notes to be redeemed; or (2) the sum of the present values

of the remaining scheduled payments of principal and interest, discounted to the

date of redemption on a semiannual basis at the Treasury Rate, plus 30 basis

points, plus accrued interest on the notes to be redeemed to, but excluding, the

date of redemption. If a change of control triggering event occurs, unless the

Company has exercised its option to redeem the notes, it will be required to offer

to repurchase the notes at a purchase price equal to 101% of the principal amount

of the notes plus accrued and unpaid interest to the date of redemption. The notes

are unsecured senior debt obligations and rank equally with all other unsecured

senior indebtedness of the Company. The notes are not convertible or exchangeable.

Total issuance costs relating to this offering were $9 million, which included

$8 million in underwriting fees. The fair value of the notes as of August 31, 2012

and 2011, was $1,350 million and $1,403 million, respectively. Fair value for

these notes was determined based upon quoted market prices.

On January 13, 2009, the Company issued notes totaling $1.0 billion bearing an

interest rate of 5.250% paid semiannually in arrears on January 15 and July 15

of each year, beginning on July 15, 2009. The notes will mature on January 15,

2019. The Company may redeem the notes, at any time in whole or from time to

time in part, at its option at a redemption price equal to the greater of: (1) 100%

of the principal amount of the notes to be redeemed; or (2) the sum of the present

values of the remaining scheduled payments of principal and interest, discounted

to the date of redemption on a semiannual basis at the Treasury Rate, plus 45

basis points, plus accrued interest on the notes to be redeemed to, but excluding,

the date of redemption. If a change of control triggering event occurs, unless the

Company has exercised its option to redeem the notes, it will be required to offer to

repurchase the notes at a purchase price equal to 101% of the principal amount of

the notes plus accrued and unpaid interest to the date of redemption. The notes are

unsecured senior debt obligations and rank equally with all other unsecured senior

indebtedness of the Company. The notes are not convertible or exchangeable. Total

issuance costs relating to this offering were $8 million, which included $7 million

in underwriting fees. The fair value of the notes as of August 31, 2012 and 2011,

was $1,160 million and $1,173 million, respectively. Fair value for these notes was

determined based upon quoted market prices.

On August 2, 2012, the Company borrowed $3.0 billion of its available $3.5 billion

variable rate 364-day bridge term loan obtained in connection with the investment in

Alliance Boots. Interest was reset monthly based upon the one-month LIBOR plus a

fixed margin, paid on a monthly basis. In fiscal 2012, interest expense on the bridge

loan was $21 million, which included $18 million in one-time costs. On September 13,

2012, the Company repaid in full all amounts borrowed under the bridge loan with a

portion of the net proceeds from a public offering of $4.0 billion of notes (see Note 16).

The Company has had no activity or outstanding balances in its commercial paper

program since fiscal 2009. In connection with the commercial paper program,

the Company maintains two unsecured backup syndicated lines of credit that total

$1.35 billion. The first $500 million facility expires on July 20, 2015, and allows

for the issuance of up to $250 million in letters of credit. The second $850 million

facility expires on July 23, 2017, and allows for the issuance of up to $200 million

in letters of credit. The issuance of letters of credit under either of these facilities

reduces available borrowings. The Company’s ability to access these facilities is

subject to compliance with the terms and conditions of the credit facilities, including

financial covenants. The covenants require the Company to maintain certain financial

ratios related to minimum net worth and priority debt, along with limitations on the

sale of assets and purchases of investments. At August 31, 2012, the Company

was in compliance with all such covenants. The Company pays a facility fee to the

financing banks to keep these lines of credit active. At August 31, 2012, there were

no letters of credit issued against these credit facilities and the Company does not

anticipate any future letters of credit to be issued against these facilities.

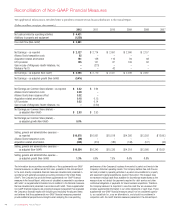

9. Financial Instruments

The Company uses derivative instruments to manage its interest rate exposure

associated with some of its fixed-rate borrowings. The Company does not use

derivative instruments for trading or speculative purposes. All derivative instruments

are recognized in the Consolidated Balance Sheets at fair value. The Company

designates interest rate swaps as fair value hedges of fixed-rate borrowings.

For derivatives designated as fair value hedges, the change in the fair value of

both the derivative instrument and the hedged item are recognized in earnings in

the current period. At the inception of a hedge transaction, the Company formally

documents the hedge relationship and the risk management objective for undertaking

the hedge. In addition, it assesses both at inception of the hedge and on an ongoing

basis whether the derivative in the hedging transaction has been highly effective

in offsetting changes in fair value of the hedged item and whether the derivative

is expected to continue to be highly effective. The impact of any ineffectiveness

is recognized currently in earnings.

Counterparties to derivative financial instruments expose the Company to credit-

related losses in the event of nonperformance, but the Company regularly monitors

the creditworthiness of each counterparty.

Fair Value Hedges

For derivative instruments that are designated and qualify as fair value hedges, the

gain or loss on the derivative, as well as the offsetting gain or loss on the hedged

item attributable to the hedged risk, are recognized in interest expense on the