Walgreens 2013 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2013 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

|

|

other things, reduce cost and improve productivity. In fiscal 2011, we recorded

$42 million of pre-tax charges in selling, general and administrative expenses

associated with the program. In total, we incurred $403 million of pre-tax charges

related to the program. We realized total savings related to Rewiring for Growth of

approximately $1.1 billion in fiscal 2011 compared to our base year of fiscal 2008.

Selling, general and administrative expenses realized total savings of $953 million,

while cost of sales benefited by approximately $122 million. The savings were

primarily the result of reduced store labor and personnel and expense reductions.

Additionally, as a part of our Customer Centric Retailing (CCR) initiative, we have

modified our store format to enhance category layouts and adjacencies, shelf heights

and sight lines, and brand and private brand assortments, all of which were designed

to positively impact the shopper experience. This initiative was completed in the

first quarter of fiscal 2012. In total, we converted 5,843 stores and opened 559

new stores with the CCR format. In fiscal 2012, we incurred $33 million in total

program costs, of which $15 million was included in selling, general and adminis-

trative expenses and $18 million in capital costs. In fiscal 2011, we incurred

$144 million in total program costs, of which $84 million was included in selling,

general and administrative expenses and $60 million in capital costs.

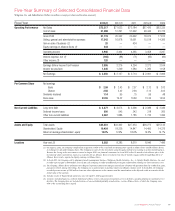

Operating Statistics

Percentage Increases/

(Decreases)

Fiscal Year 2013 2012 2011

Net Sales 0.8 (0.8) 7.1

Net Earnings 15.2 (21.6) 29.8

Comparable Drugstore Sales (1.3) (3.6) 3.3

Prescription Sales 0.4 (3.1) 6.3

Comparable Drugstore Prescription Sales (1.7) (6.1) 3.3

Front-End Sales 1.5 3.6 8.5

Comparable Drugstore Front-End Sales (0.7) 0.6 3.3

Gross Profit 3.8 (0.7) 8.0

Selling, General and Administrative Expenses 3.9 1.9 6.7

Percent to Net Sales

Fiscal Year 2013 2012 2011

Gross Margin 29.3 28.4 28.4

Selling, General and Administrative Expenses 24.3 23.6 23.0

Other Statistics

Fiscal Year 2013 2012 2011

Prescription Sales as a % of Net Sales 62.9 63.2 64.7

Third Party Sales as a % of Total Prescription Sales 95.8 95.6 95.6

Number of Prescriptions (in millions) 683 664 718

Comparable Prescription % Increase/(Decrease) 2.9 (8.4) 1.5

30-Day Equivalent Prescriptions (in millions)* 821 784 819

Comparable 30-Day Equivalent Prescription

% Increase/(Decrease)* 4.8 (5.1) 3.7

Total Number of Locations 8,582 8,385 8,210

* Includes the adjustment to convert prescriptions greater than 84 days to the equivalent

of three 30-day prescriptions. This adjustment reflects the fact that these prescriptions

include approximately three times the amount of product days supplied compared to a

normal prescription.

Results of Operations

Fiscal 2013 net earnings increased 15.2% to $2.5 billion, or $2.56 per diluted

share, versus last year’s earnings of $2.1 billion, or $2.42 per diluted share.

The increase was primarily attributable to higher sales, improved margins, equity

earnings in Alliance Boots and other non-operating income related to our

AmerisourceBergen warrants, partially offset by higher selling, general and adminis-

trative expenses as a percentage of sales. Included in net earnings and net earnings

per diluted share, respectively, were the negative impacts of $241 million, or

$.25 per diluted share, in acquisition-related amortization; $151 million, or $.16 per

diluted share, from the LIFO provision; $124 million, or $.13 per diluted share, in

Alliance Boots related tax; $60 million, or $.06 per diluted share, of acquisition-related

costs; $47 million, or $.05 per diluted share, relating to certain litigation matters

including the DEA settlement; $24 million, or $.03 per diluted share, in costs related

to Hurricane Sandy; and $8 million, or $.01 per diluted share, in costs related to the

completion of a pharmaceutical distribution contract. Net earnings were positively

impacted by $110 million, or $.12 per diluted share, from fair value adjustments of

Form 8-K filed on September 10, 2012, includes as exhibits thereto Alliance Boots

audited consolidated financial statements for the years ended March 31, 2012, 2011

and 2010 (prepared in accordance with International Financial Reporting Standards

(IFRS) as issued by the International Accounting Standards Board) and unaudited

pro forma consolidated financial information related to our 45% investment in Alliance

Boots. Alliance Boots audited consolidated financial statements for the years ended

March 31, 2013 and 2012 (prepared in accordance with IFRS) are available on our

Form 8-K filed on May 15, 2013. Walgreens equity earnings, initial investment and the

call option excludes the Alliance Boots minority interest in Galenica Ltd. (Galenica). The

Alliance Boots investment in Galenica was distributed to the Alliance Boots shareholders

other than Walgreens during May 2013, which had no impact to us. We account for

our 45% investment in Alliance Boots using the equity method of accounting.

Investments accounted for under the equity method are recorded initially at cost and

subsequently adjusted for our share of the net income or loss and cash contributions

and distributions to or from these entities. Net income reported by Alliance Boots is

translated from British pounds Sterling at the average rate for the period. See Note 5

to our consolidated financial statements for additional information regarding our equity

method investments. We utilize a three-month lag in reporting equity income from our

investment in Alliance Boots, reported as equity earnings in Alliance Boots on the

Consolidated Statements of Comprehensive Income. The investment is recorded as

Equity investment in Alliance Boots in the Consolidated Balance Sheets.

Combined synergies across both companies were approximately $154 million in the

first year following completion of our 45% investment in Alliance Boots. Fiscal 2014

combined synergies are estimated to be between $350 million and $400 million.

The three-month lag impacts the quarterly and fiscal year timing of when Alliance Boots

results and synergies will be reflected in the equity earnings in Alliance Boots included in

our financial statements. Because of the three-month lag and the timing of the closing

of this investment, our financial statements for the year ended August 31, 2013, reflect

twelve months of the dilutive effect of the incremental shares and interest expense

associated with our Alliance Boots investment, but only ten months (August 2012

through May 2013) of results of Alliance Boots are reflected in the equity earnings

in Alliance Boots included in our Consolidated Statements of Comprehensive Income

for the twelve-month period. See “Cautionary Note Regarding Forward-Looking

Statements” below.

On March 19, 2013, we, in conjunction with Alliance Boots and AmerisourceBergen

Corporation (AmerisourceBergen) announced various agreements and arrangements,

including a ten-year pharmaceutical distribution agreement between ourselves and

AmerisourceBergen pursuant to which we will source branded and generic pharma-

ceutical products from AmerisourceBergen; an agreement which provides

AmerisourceBergen the ability to access generics and related pharmaceutical prod-

ucts through Walgreens Boots Alliance Development GmbH, a global sourcing joint

venture between ourselves and Alliance Boots; and agreements and arrangements

pursuant to which we and Alliance Boots together have the right, but not the obligation,

to purchase a minority equity position in AmerisourceBergen and gain associated

representation on AmerisourceBergen’s board of directors in certain circumstances.

AmerisourceBergen has begun to distribute all branded pharmaceutical products that

we historically sourced from distributors and suppliers, effective September 1, 2013.

AmerisourceBergen began distribution of certain branded drugs in the fourth quarter.

Over time, beginning in calendar year 2014, AmerisourceBergen is expected to

distribute increasingly significant levels of generic pharmaceutical products that

we currently self-distribute. In addition to the information in this report, please refer

to our Current Report on Form 8-K filed on March 20, 2013, for more detailed

information regarding these agreements and arrangements. See “Cautionary Note

Regarding Forward-Looking Statements” below.

Investments accounted for under the equity method are recorded initially at cost and

subsequently adjusted for the Company’s share of the net income or loss and cash

contributions and distributions to or from these entities. The Company’s investment in

Alliance Boots and the related call option were recorded as assets with a $7.1 billion

aggregate value on the Company’s August 31, 2013 balance sheet, which represented

30.1% of the Company’s long-lived assets as of that date. Because the Company’s

investment in Alliance Boots is denominated in a foreign currency (British pounds

Sterling), translation gains or losses impact the value of the investment. See Note 5

to Consolidated Financial Statements for additional information.

Restructuring and Customer Centric Retailing Initiative

We completed one of our strategic initiatives to enhance shareholder value in fiscal

2011, known as the “Rewiring for Growth” program, which was designed to, among

2013 Walgreens Annual Report 21