Walgreens 2013 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2013 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

|

|

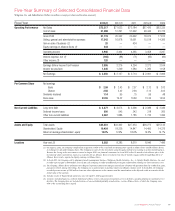

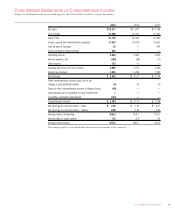

The effective income tax rate was 37.1% for fiscal 2013, 37.0% for 2012, and 36.8%

for 2011. The increase in the effective tax rate from fiscal 2012 was primarily

attributed to higher non-tax deductible permanent differences. Fiscal 2012 included

certain non-deductible transaction costs associated with the investment in Alliance

Boots. We anticipate an effective tax rate of approximately 36% in fiscal 2014.

Liquidity and Capital Resources

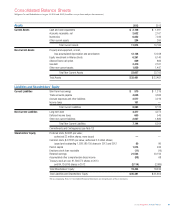

Cash and cash equivalents were $2.1 billion at August 31, 2013, compared to

$1.3 billion at August 31, 2012. Short-term investment objectives are to minimize

risk, maintain liquidity and maximize after-tax yields. To attain these objectives,

investment limits are placed on the amount, type and issuer of securities.

Investments are principally in U.S. Treasury market funds.

Our long-term capital policy is to maintain a strong balance sheet and financial flexi-

bility; reinvest in our core strategies; invest in strategic opportunities that reinforce

our core strategies and meet return requirements; and return surplus cash flow to

shareholders in the form of dividends and share repurchases over the long term.

Net cash provided by operating activities was $4.3 billion at August 31, 2013,

compared to $4.4 billion a year ago. The decrease was primarily a result of changes

in working capital balances. Prior year operating activities also benefited by

increased efforts to reduce inventory during the period we were out of the Express

Scripts network. Cash provided by operations is the principal source of funds

for expansion, investments, acquisitions, remodeling programs, dividends to

shareholders and stock repurchases.

Net cash used for investing activities was $2.0 billion versus $5.9 billion last year.

Additions to property and equipment were $1.2 billion compared to $1.6 billion last

year. In fiscal 2013, we added a total of 350 locations (197 net) compared to last

year’s 266 locations (175 net). The USA Drug acquisition contributed 141 locations

(70 net) in fiscal 2013. There were 39 owned locations added during the year and

41 under construction at August 31, 2013, versus 34 owned locations added and

41 under construction as of August 31, 2012.

Infusion and

Work- Respiratory Specialty Mail

Drugstores sites Services Pharmacy Service Total

August 31, 2011 7,761 355 83 9 2 8,210

New/Relocated 169 36 5 2 — 212

Acquired 43 — 10 1 — 54

Closed/Replaced (43) (25) (22) (1) — (91)

August 31, 2012 7,930 366 76 11 2 8,385

New/Relocated 172 14 10 2 — 198

Acquired 147 — 1 4 — 152

Closed/Replaced (133) (9) (5) (6) — (153)

August 31, 2013 8,116 371 82 11 2 8,582

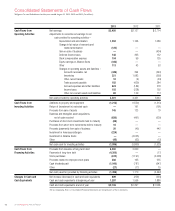

Business acquisitions this year were $630 million versus $491 million last year.

Business acquisitions in the current year include the purchase of the regional drugstore

chain USA Drug from Stephen L. LaFrance Holdings, Inc. and members of the LaFrance

family for $436 million net of assumed cash, an 80% interest in Cystic Fibrosis

Foundation Pharmacy, LLC for $29 million net of assumed cash, and selected other

assets (primarily prescription files). In fiscal 2013, we purchased $224 million of

AmerisourceBergen common stock. Additionally, in the current year, we received

client retention proceeds of $20 million in accordance with the June 2011 sales

agreement of our pharmacy benefit management business, Walgreens Health

Initiatives, Inc. (WHI). Investing activities in 2012 include the August 2012 purchase of

a 45% equity interest in Alliance Boots for $7.0 billion, of which $4.0 billion was

cash. This investment is accounted for as an equity method investment. Business

acquisitions in fiscal 2012 included certain assets from BioScrip’s community specialty

pharmacies and centralized specialty and mail services pharmacy businesses for

$144 million plus inventory; the purchase of Crescent Pharmacy Holdings, LLC, an

infusion pharmacy business, for $73 million, net of assumed cash; and selected other

assets (primarily prescription files). In fiscal 2012, we paid $45 million to Catalyst Health

Solutions Inc. (Catalyst), which was the result of a working capital adjustment in

accordance with the sale of WHI.

Capital expenditures for fiscal 2014 are expected to be approximately $1.4 billion,

excluding business acquisitions, joint ventures and prescription file purchases,

although the actual amount may vary depending upon a variety of factors, including,

among other things, the timing of implementation of certain capital projects.

We expect to add approximately 85 to 160 new drugstores in fiscal 2014. In addition,

we continue to allocate a portion of our capital budget to relocating stores to more

convenient and profitable freestanding locations.

Net cash used by financing activities was $1.5 billion compared to the prior year

which provided net cash of $1.2 billion. In September 2012, we received proceeds

from a public offering of $4.0 billion of notes with varying interest rates (see Note 9).

The notes were used, in part, to repay the $3.0 billion 364-day bridge term loan

obtained in August 2012 in connection with the investment in Alliance Boots. In addition,

we repaid our $1.3 billion 4.875% notes upon maturity on August 1, 2013. We

repurchased shares totaling $615 million in the current year, all of which was to support

the needs of the employee stock plans. In the prior year, we repurchased shares totaling

$1.2 billion, primarily in conjunction with our share buyback programs and $40 million

to support the needs of the employee stock plans. We had proceeds related to

employee stock plans of $486 million compared to $165 million last year. Cash

dividends paid were $1.0 billion versus $787 million a year ago. On July 10, 2013,

we announced an increase in the quarterly dividend to 31.5 cents per share from the

previous rate of 27.5 cents per share. The increase raises the annual dividend rate

from $1.10 per share to $1.26 per share.

In connection with our long-term capital policy, our Board of Directors has authorized

several share repurchase programs and set a long-term dividend payout ratio target

between 30 and 35 percent of net earnings. The 2009 and 2011 stock repurchase

programs, which were both completed in fiscal 2011, allowed for the repurchase of

up to $2.0 billion and $1.0 billion of the Company’s common stock, respectively.

Additionally, on July 13, 2011, our Board of Directors authorized the 2012 stock

repurchase program, which allows for the repurchase of up to $2.0 billion of the

Company’s common stock prior to its expiration on December 31, 2015. Activity

related to these programs was as follows (In millions):

Fiscal Year Ended 2013 2012 2011

2009 stock repurchase program $ — $ — $ 360

2011 stock repurchase program — — 1,000

2012 stock repurchase program — 1,151 424

$ — $ 1,151 $ 1,784

We determine the timing and amount of repurchases from time to time based on our

assessment of various factors including prevailing market conditions, alternate uses of

capital, liquidity, the economic environment and other factors. We anticipate that the

pace of any future share repurchase will continue to be significantly curtailed from

the levels achieved in fiscal 2012 and 2011 due to the debt levels incurred for

the investment in Alliance Boots. The timing and amount of these purchases may

change at any time and from time to time. The Company has repurchased and may

from time to time in the future repurchase shares on the open market through

Rule 10b5-1 plans, which enable a company to repurchase shares at times when

it otherwise might be precluded from doing so under insider trading laws.

We had no commercial paper outstanding at August 31, 2013. In connection with our

commercial paper program, we maintain two unsecured backup syndicated lines of

credit that total $1.35 billion. The first $500 million facility expires on July 20, 2015,

and allows for the issuance of up to $250 million in letters of credit. The second

$850 million facility expires on July 23, 2017, and allows for the issuance of up to

$200 million in letters of credit. The issuance of letters of credit under either of these

facilities reduces available borrowings. Our ability to access these facilities is subject to

our compliance with the terms and conditions of the credit facility, including financial

covenants. The covenants require us to maintain certain financial ratios related to

minimum net worth and priority debt, along with limitations on the sale of assets and

purchases of investments. At August 31, 2013, we were in compliance with all such

covenants. The Company pays a facility fee to the financing banks to keep these lines

of credit active. At August 31, 2013, there were no letters of credit issued against

these facilities and we currently do not anticipate any future letters of credit to be

issued against these facilities.

As of October 17, 2013, our credit ratings were:

Long-Term Commercial

Rating Agency Debt Rating Paper Rating Outlook

Moody’s Baa1 P-2 Negative

Standard & Poor’s BBB A-2 Stable

2013 Walgreens Annual Report 23