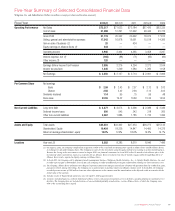

Walgreens 2013 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2013 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

|

|

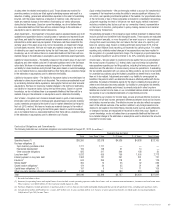

The obligations and commitments included in the table above do not include

unconsolidated partially owned entities, such as Alliance Boots, of which we own

45% of the outstanding share capital. The expected timing of payments of the

obligations above is estimated based on current information. Timing of payments

and actual amounts paid may be different, depending on the time of receipt of

goods or services, or changes to agreed-upon amounts for some obligations.

In connection with the Alliance Boots Purchase and Option Agreement dated

June 18, 2012, we have the right, but not the obligation, to purchase the

remaining 55% interest in Alliance Boots at any time during the period beginning

February 2, 2015, and ending August 2, 2015. If we exercise this call option, we

would, subject to the terms and conditions of such agreement, be obligated to make

a cash payment of £3.133 billion (equivalent to approximately $4.9 billion based on

exchange rates as of August 31, 2013) and issue approximately 144.3 million shares

of our common stock, with the amount and form of such consideration being subject

to adjustment in certain circumstances including if the volume weighted-average price

of our common stock is below $31.18 per share during a period shortly before the

closing of the second step transaction. We also would assume the then-outstanding

debt of Alliance Boots upon the closing of the second step transaction.

In the event that we do not exercise the option, under certain circumstances,

our ownership of Alliance Boots will reduce from 45% to 42% in exchange

for nominal consideration to Walgreens.

In addition, pursuant to our arrangements with AmerisourceBergen and Alliance Boots,

we and Alliance Boots have the right, but not the obligation, to purchase a minority

equity position in AmerisourceBergen over time, including open market purchases

and warrants to acquire AmerisourceBergen common stock. If we elect to exercise

the two warrants issued by AmerisourceBergen in full, Walgreens would, subject to

the terms and conditions of such warrants, be required to make a cash payment of

approximately $584.4 million in connection with the exercise of the first warrant during

a six-month period beginning in March 2016 and $595.8 million in connection

with the exercise of the second warrant during a six-month period beginning in

March 2017. Similarly, if Alliance Boots elects to exercise the two warrants issued by

AmerisourceBergen in full, Alliance Boots would, subject to the terms and conditions

of such warrants, be required to pay AmerisourceBergen similar amounts upon the

exercise of their warrants in 2016 and 2017. Our and Alliance Boots ability to invest

in equity in AmerisourceBergen above certain thresholds is subject to the receipt of

regulatory approvals. See “Liquidity and Capital Resources” above.

Off–Balance Sheet Arrangements

We do not have any unconsolidated special purpose entities and, except as

described herein, we do not have significant exposure to any off–balance sheet

arrangements. The term “off–balance sheet arrangement” generally means any

transaction, agreement or other contractual arrangement to which an entity uncon-

solidated with us is a party, under which we have: (i) any obligation arising under

a guarantee contract, derivative instrument or variable interest; or (ii) a retained

or contingent interest in assets transferred to such entity or similar arrangement

that serves as credit, liquidity or market risk support for such assets.

Letters of credit are issued to support purchase obligations and commitments

(as reflected on the Contractual Obligations and Commitments table) as follows

(In millions):

August 31, 2013

Inventory purchase commitments $ 197

Insurance 263

Real estate development 4

Total $ 464

We have no off–balance sheet arrangements other than those disclosed on the

Contractual Obligations and Commitments table. Both on–balance sheet and

off–balance sheet financing alternatives are considered when pursuing our

capital structure and capital allocation objectives.

Recent Accounting Pronouncements

In July 2012, the Financial Accounting Standards Board (FASB) issued Accounting

Standards Update 2012-02, Intangibles – Goodwill and Other (Topic 350) – Testing

Indefinite-Lived Intangible Assets for Impairment, which permits an entity to make a

qualitative assessment to determine whether it is more likely than not that an

indefinite-lived intangible asset, other than goodwill, is impaired. If an entity concludes,

based on an evaluation of all relevant qualitative factors, that it is not more likely than

not that the fair value of an indefinite-lived intangible asset is less than its carrying

amount, it will not be required to perform the quantitative impairment for that asset.

The ASU is effective for impairment tests performed for fiscal years beginning after

September 15, 2012 (fiscal 2014), with early adoption permitted. The ASU will

not have a material impact on the Company’s reported results of operations

and financial position. The impact is non-cash in nature and will not affect the

Company’s cash position.

In May 2013, FASB reissued an exposure draft on lease accounting that would require

entities to recognize assets and liabilities arising from lease contracts on the balance

sheet. The proposed exposure draft states that lessees and lessors should apply

a “right-of-use model” in accounting for all leases. Under the proposed model,

lessees would recognize an asset for the right to use the leased asset, and a liability

for the obligation to make rental payments over the lease term. When measuring

the asset and liability, variable lease payments are excluded, whereas renewal options

that provide a significant economic incentive upon renewal would be included.

The accounting by a lessor would reflect its retained exposure to the risks or benefits

of the underlying leased asset. A lessor would recognize an asset representing its

right to receive lease payments based on the expected term of the lease. The lease

expense from real estate based leases would continue to be recorded under a

straight-line approach, but other leases not related to real estate would be expensed

using an effective interest method that would accelerate lease expense. A final standard

is currently expected to be issued in 2014 and would be effective no earlier than

annual reporting periods beginning on January 1, 2017 (fiscal 2018 for the Company).

The proposed standard, as currently drafted, would have a material impact on the

Company’s financial position and the impact on the Company’s reported results of

operations is being evaluated. The impact of this exposure draft is non-cash in nature

and would not affect the Company’s cash position.

In July 2013, the FASB issued Accounting Standards Update 2013-11, Income

Taxes (Topic 740) – Presentation of an Unrecognized Tax Benefit when a Net

Operating Loss Carryforward or Tax Credit Carryforward Exists. This update provides

that an entity’s unrecognized tax benefit, or a portion of its unrecognized tax benefit,

should be presented in its financial statements as a reduction to a deferred tax

asset for a net operating loss carryforward, a similar tax loss, or a tax credit carry-

forward. This update applies prospectively to all entities that have unrecognized tax

benefits when a net operating loss carryforward, a similar tax loss, or a tax credit

carryforward exists at the reporting date. Retrospective application is also permitted.

This update is effective for annual periods, and interim periods within those years,

beginning after December 15, 2013 (fiscal 2014). The standard will not have a

material impact on the Company’s reported results of operations and financial

position. The impact of this ASU is non-cash in nature and will not affect the

Company’s cash position.

Financing and Market Risk

We are exposed to interest rate volatility with regard to future issuances of

fixed-rate debt, and existing and future issuances of floating-rate debt. Primary

exposures include U.S. Treasury rates, LIBOR and commercial paper rates.

From time to time, we use interest rate swaps and forward-starting interest rate

swaps to hedge our exposure to interest rate changes, to reduce the volatility of

our financing costs, and to achieve a desired proportion of fixed versus floating-

rate debt, based on current and projected market conditions. Generally under

these swaps, we agree with a counterparty to exchange the difference between

fixed-rate and floating-rate interest rate amounts based on an agreed upon

notional principal amount.

Information regarding our interest rate swap transactions is set forth in Note 10 to

the Consolidated Financial Statements. These financial instruments are sensitive

to changes in interest rates. On August 31, 2013, we had $1.6 billion in long-term

debt obligations that had floating interest rates. A one percentage point increase or

decrease in interest rates would increase or decrease the annual interest expense

we recognize and the cash we pay for interest expense by approximately $16 million.

In connection with our Purchase and Option Agreement with Alliance Boots and the

transactions contemplated thereby, our exposure to foreign currency risks, primarily

Management’s Discussion and Analysis of Results of Operations

and Financial Condition (continued)

26 2013 Walgreens Annual Report