McKesson 2005 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2005 McKesson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

|

|

McKESSON CORPORATION

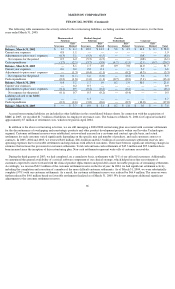

FINANCIAL NOTES (Continued)

Convertible Junior Subordinated Debentures

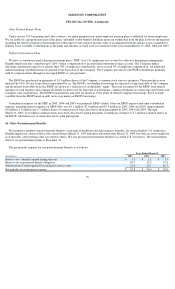

In February 1997, we issued 5% Convertible Junior Subordinated Debentures (the “Debentures”) in an aggregate principal amount of

$206,186,000. The Debentures, which are included in long-term debt, mature on June 1, 2027, bear interest at an annual rate of 5%, payable

quarterly, and are currently redeemable by us at 101.0% of the principal amount. The Debentures were purchased by the McKesson Financing

Trust (“Trust”), which is wholly owned by the Company, with proceeds from its issuance of four million shares of preferred securities to the

public and 123,720 common securities to us. These preferred securities are convertible at the holder’s option into the Company’s common

stock. The Debentures represent the sole assets of the Trust. The Company was not designated as the primary beneficiary of the Trust and as a

result, does not consolidate its investment in the Trust.

Holders of the preferred securities are entitled to cumulative cash distributions at an annual rate of 5% of the liquidation amount of $50 per

security. Each preferred security is convertible at the rate of 1.3418 shares of the Company’s common stock, subject to adjustment in certain

circumstances. The preferred securities will be redeemed upon repayment of the Debentures and are callable by us on or after March 4, 2000,

in whole or in part, initially at 103.5% of the liquidation preference per share, and thereafter at prices declining at 0.5% per annum to 100% of

the liquidation preference on and after March 4, 2007 plus, in each case, accumulated, accrued and unpaid distributions, if any, to the

redemption date.

We have guaranteed, on a subordinated basis, distributions and other payments due on the preferred securities (the “Guarantee”). The

Guarantee, when taken together with our obligations under the Debentures, and in the indenture pursuant to which the Debentures were issued,

and our obligations under the Amended and Restated Declaration of Trust governing the subsidiary trust, provides a full and unconditional

guarantee of amounts due on the preferred securities.

Other Financing

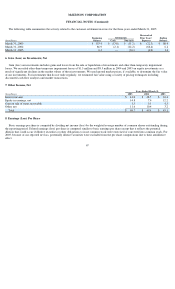

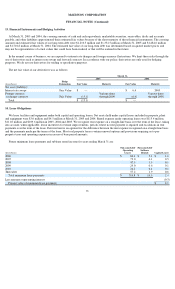

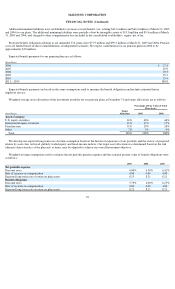

In September 2004, we entered into a $1.3 billion five-year, senior unsecured revolving credit facility. Borrowings under the new credit

facility bear interest at a fixed base rate, or a floating rate based on the London Interbank Offering Rate (“LIBOR”) rate or a Eurodollar rate.

Effective as of the closing date of the new credit facility agreement, we terminated the commitments under a $550 million, three-year revolving

credit facility that would have expired in September 2005 and a $650 million, 364-day credit facility that would have expired in September

2004. At March 31, 2005, no amounts were outstanding under the revolving credit facility.

In June 2004, we renewed our committed revolving receivables sale facility under substantially similar terms to those previously in place,

with the exception that the facility was increased by $300.0 million to $1.4 billion. The renewed facility expires in June 2005. At March 31,

2005 and March 31, 2004, no amounts were outstanding or utilized under the receivables sale facility.

In 2005, 2004 and 2003, we sold customer lease portfolio receivables for cash proceeds of $50.7 million, $45.4 million and $117.9 million.

The employee stock ownership program (“ESOP”) debt bears interest at rates ranging from 8.6% fixed rate to approximately 89% of the

London Interbank Offering Rate (“LIBOR”) or LIBOR plus 0.4% and is due in semi-annual and annual installments through 2009.

Our various borrowing facilities and certain long-term debt instruments are subject to covenants. Our principal debt covenant is our debt to

capital ratio, which cannot exceed 56.5%. If we exceed this ratio, repayment of debt outstanding under the revolving credit facility and

$235.0 million of term debt could be accelerated. At March 31, 2005, this ratio was 18.7% and we were in compliance with all other covenants.

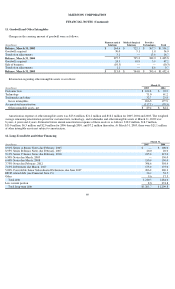

Aggregate annual payments on long-term debt, including capital lease obligations, for the years ending March 31, are as follows:

$8.8 million in 2006, $27.5 million in 2007, $157.5 million in 2008, $8.0 million in 2009, $222.9 million in 2010 and $785.8 million thereafter.

70