American Airlines 2006 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2006 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

|

|

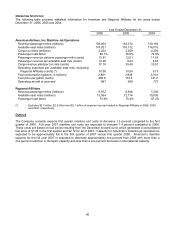

41

Other Information

Critical Accounting Policies and Estimates The preparation of the Company’s financial statements in

conformity with generally accepted accounting principles requires management to make estimates and

assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes.

The Company believes its estimates and assumptions are reasonable; however, actual results and the timing of

the recognition of such amounts could differ from those estimates. The Company has identified the following

critical accounting policies and estimates used by management in the preparation of the Company’s financial

statements: accounting for long-lived assets, passenger revenue, frequent flyer program, stock compensation,

pensions and other postretirement benefits, and income taxes.

Long-lived assets – The Company has approximately $19 billion of long-lived assets as of December 31,

2006, including approximately $18 billion related to flight equipment and other fixed assets. In addition to

the original cost of these assets, their recorded value is impacted by a number of estimates made by the

Company, including estimated useful lives, salvage values and the Company’s determination as to whether

aircraft are temporarily or permanently grounded. In accordance with Statement of Financial Accounting

Standards No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets” (SFAS 144), the

Company records impairment charges on long-lived assets used in operations when events and

circumstances indicate that the assets may be impaired, the undiscounted cash flows estimated to be

generated by those assets are less than the carrying amount of those assets and the net book value of the

assets exceeds their estimated fair value. In making these determinations, the Company uses certain

assumptions, including, but not limited to: (i) estimated fair value of the assets; and (ii) estimated future

cash flows expected to be generated by the assets, generally evaluated at a fleet level, which are based on

additional assumptions such as asset utilization, length of service and estimated salvage values. A change

in the Company's fleet plan has been the primary indicator that has resulted in an impairment charge in the

past.

On November 17, 2004, American deferred the delivery date of 54 Boeing aircraft by approximately seven

years which, in combination with numerous other factors, led American to re-evaluate the expected useful

lives of its aircraft. As a result of this evaluation, American changed its estimate of the depreciable lives of

its Boeing 737-800, Boeing 757-200 and McDonnell Douglas MD-80 aircraft from 25 to 30 years effective

January 1, 2005. The primary factors that supported changing the estimated useful life of these aircraft

were (i) the absence of scheduled narrow body deliveries until 2013 (even these 47 narrow body deliveries

would only replace less than ten percent of the Company’s existing narrow body fleet assuming the

deliveries are not used to grow the Company’s capacity at that time), (ii) the financial condition of the

Company, which significantly limits its flexibility to purchase new aircraft and (iii) the absence of technology

step change for narrow body aircraft, such as technology that would allow the Company to fly its aircraft

substantially more efficiently (as was the case with replacements for previous generation aircraft such as

the B-727 which had three engines versus two on the replacement aircraft) that would clearly economically

compel the Company to replace the fleet. In addition, there are currently no government regulations, such

as noise reduction requirements, that would require aircraft replacement.

Subsequent to the change in depreciable lives on January 1, 2005, all of American’s fleet types are

depreciated over 30 years except for the Airbus A300 and the Boeing 767, which did not generally meet the

above conditions to support extending their lives.