Charter 2004 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2004 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

CHARTER COMMUNICATIONS, INC. AND SUBSIDIARIES 2004 FORM 10-K

Notes to Consolidated Financial Statements

December 31, 2004, 2003 and 2002

(dollars in millions, except where indicated)

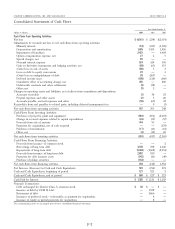

1. ORGANIZATION AND BASIS OF PRESENTATION ing activities were $472 million, $765 million and $748 million

for the years ending December 31, 2004, 2003 and 2002,

Charter Communications, Inc. (‘‘Charter’’) is a holding company respectively.

whose principal assets at December 31, 2004 are the 47% The Company has a significant level of debt. The Com-

controlling common equity interest in Charter Communications pany’s long-term financing as of December 31, 2004 consists of

Holding Company, LLC (‘‘Charter Holdco’’) and ‘‘mirror’’ notes $5.5 billion of credit facility debt, $13.3 billion principal amount

which are payable by Charter Holdco to Charter and have the of high-yield notes and $1.0 billion principal amount of

same principal amount and terms as those of Charter’s convertible senior notes. In 2005, $30 million of the Company’s

convertible senior notes. Charter Holdco is the sole owner of debt will mature and in 2006, an additional $186 million of the

Charter Communications Holdings, LLC (‘‘Charter Holdings’’). Company’s debt will mature. In 2007 and beyond, significant

The consolidated financial statements include the accounts of additional amounts will become due under the Company’s

Charter, Charter Holdco, Charter Holdings and all of their remaining long-term debt obligations.

wholly owned subsidiaries where the underlying operations The Company has historically required significant cash to

reside, collectively referred to herein as the ‘‘Company.’’ Charter fund capital expenditures and debt service costs. Historically, the

consolidates Charter Holdco on the basis of voting control. Company has funded these requirements through cash flows

Charter Holdco’s limited liability company agreement provides from operating activities, borrowings under its credit facilities,

that so long as Charter’s Class B common stock retains its sales of assets, issuances of debt and equity securities and cash

special voting rights, Charter will maintain a 100% voting on hand. However, the mix of funding sources changes from

interest in Charter Holdco. Voting control gives Charter full period to period. For the year ended December 31, 2004, the

authority and control over the operations of Charter Holdco. All Company, generated $472 million of net cash flows from

significant intercompany accounts and transactions among con- operating activities, after paying cash interest of $1.3 billion. In

solidated entities have been eliminated. The Company is a addition, the Company generated approximately $744 million

broadband communications company operating in the United from the sale of assets, substantially all of which was used to

States. The Company offers its customers traditional cable video fund operations, including capital expenditures. Finally, the

programming (analog and digital video) as well as high-speed Company had net cash flows from financing activities of

data services and, in some areas, advanced broadband services $294 million, which included, among other things, the proceeds

such as high definition television, video on demand and from the issuance in December of $550 million of CCO

telephony. The Company sells its cable video programming, Holdings, LLC (‘‘CCO Holdings’’) Notes. This debt issuance

high-speed data and advanced broadband services on a subscrip- was the primary reason cash on hand increased by $523 million

tion basis. The Company also sells local advertising on satellite- to $650 million at December 31, 2004. Approximately $622 mil-

delivered networks. lion was used to repay outstanding borrowings under the

The preparation of financial statements in conformity with Company’s revolving credit facility, through a series of transac-

accounting principles generally accepted in the United States tions executed in February 2005.

requires management to make estimates and assumptions that The Company expects that cash on hand, cash flows from

affect the reported amounts of assets and liabilities and operating activities and the amounts available under its credit

disclosure of contingent assets and liabilities at the date of the facilities will be adequate to meet its cash needs in 2005. Cash

financial statements and the reported amounts of revenues and flows from operating activities and amounts available under the

expenses during the reporting period. Areas involving significant Company’s credit facilities may not be sufficient to fund the

judgments and estimates include capitalization of labor and Company’s operations and satisfy its principal repayment obliga-

overhead costs; depreciation and amortization costs; impair- tions that come due in 2006 and, the Company believes, will

ments of property, plant and equipment, franchises and good- not be sufficient to fund its operations and satisfy such

will; income taxes; and contingencies. Actual results could differ repayment obligations thereafter.

from those estimates. It is likely that the Company will require additional funding

Reclassifications. Certain prior year amounts have been to repay debt maturing after 2006. The Company is working

reclassified to conform with the 2004 presentation. with its financial advisors to address such funding requirements.

However, there can be no assurance that such funding will be

2. LIQUIDITY AND CAPITAL RESOURCES available to the Company. Although Mr. Allen and his affiliates

The Company incurred net loss applicable to common stock of have purchased equity from the Company in the past, Mr. Allen

$4.3 billion, $242 million and $2.5 billion in 2004, 2003 and and his affiliates are not obligated to purchase equity from,

2002, respectively. The Company’s net cash flows from operat- contribute to or loan funds to the Company in the future.

F-8