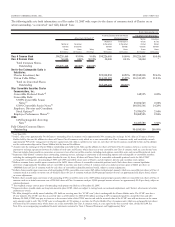

Charter 2007 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2007 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

cable system. In 2007, major DBS competitors offered a greater

variety of channel packages, and were especially competitive

with promotional pricing for more basic services, such as a

monthly price of approximately $35 for 100 channels compared

to approximately $50 for the closest comparable package offered

by us in most of our markets. In addition, while we continue to

believe that the initial investment by a DBS customer exceeds

that of a cable customer, the initial equipment cost for DBS has

decreased substantially, as the DBS providers have aggressively

marketed offers to new customers of incentives for discounted or

free equipment, installation, and multiple units. DBS providers

are able to offer service nationwide and are able to establish a

national image and branding with standardized offerings, which

together with their ability to avoid franchise fees of up to 5% of

revenues and property tax, leads to greater efficiencies and lower

costs in the lower tiers of service. However, we believe that

cable-delivered OnDemand and Subscription OnDemand services

are superior to DBS service, because cable headends can provide

two-way communication to deliver many titles which customers

can access and control independently, whereas DBS technology

can only make available a much smaller number of titles with

DVR-like customer control. We also believe that our higher tier

services, particularly bundled premium packages, are price-com-

petitive with DBS packages, and that many consumers prefer our

ability to economically bundle video packages with high-speed

Internet packages. Further, we have the potential in some areas

to provide a more complete “whole house” communications

package when combining video, high-speed Internet, and tele-

phone services. We believe that this ability to bundle services

differentiates us from DBS competitors and could enable us to

win back former customers who migrated to satellite. However,

joint marketing arrangements between DBS providers and tele-

communications carriers allow similar bundling of services in

certain areas. DBS providers have also made attempts at wide-

spread deployment of high-speed Internet access services via

satellite, but those services have been technically constrained and

of limited appeal. DBS providers are offering more high defini-

tion programming, including local high definition programming.

Telephone Companies and Utilities

Charter’s telephone service competes directly with established

telephone companies and other carriers, including internet-based

VoIP providers, for voice service customers. Because we offer

voice services, we are subject to considerable competition from

telephone companies and other telecommunications providers.

The telecommunications industry is highly competitive and

includes competitors with greater financial and personnel

resources, strong brand name recognition, and long-standing

relationships with regulatory authorities and customers. More-

over, mergers, joint ventures and alliances among our competi-

tors have resulted in providers capable of offering cable

television, Internet, and telephone services in direct competition

with us. For example, major local exchange carriers have entered

into joint marketing arrangements with DBS providers to offer

bundled packages combining telephone (including wireless),

high-speed Internet, and video services.

DSL service allows Internet access to subscribers at data

transmission speeds greater than those available over conven-

tional telephone lines. DSL service therefore is more competitive

with high-speed Internet access over cable systems than conven-

tional dial-up. Most telephone companies, which already have

plant, an existing customer base, and other operational functions

in place (such as, billing, service personnel, etc.), offer DSL

service. We expect DSL to remain a significant competitor to

our high-speed Internet services, particularly as telephone com-

panies bundle DSL with telephone service. In addition, the

continuing deployment of fiber into telephone companies’ net-

works (primarily by Verizon Communications, Inc. (“Verizon”))

will enable them to provide even higher bandwidth Internet

services.

We believe that pricing for residential and commercial

Internet services on our system is generally comparable to that

for similar DSL services and that some residential customers

prefer our Internet services bundled with our video and/or

telephone services, and prefer our high Internet speeds. However,

DSL providers may currently be in a better position to offer data

services to businesses since their networks tend to be more

complete in commercial areas. They also have the ability to

bundle telephone with Internet services for a higher percentage

of their customers.

Telephone companies, including AT&T Inc. (“AT&T”) and

Verizon, can offer video and other services in competition with

us, and we expect they will increasingly do so in the future.

AT&T and Verizon are both upgrading their networks. Some

upgraded portions of these networks carry two-way video ser-

vices comparable to ours, in the case of Verizon, high-speed data

services that operate at speeds as high as or higher than ours,

and digital voice services that are similar to ours. In addition,

these companies continue to offer their traditional telephone

services, as well as service bundles that include wireless voice

services provided by affiliated companies. Based on internal

estimates, we believe that AT&T and Verizon are offering video

services in areas serving approximately 5% to 6% of our esti-

mated homes passed as of December 31, 2007. Additional

upgrades and product launches, primarily by AT&T, are

expected in markets in which we operate.

In addition to telephone companies obtaining franchises or

alternative authorizations in some areas and seeking them in

others, they have been successful through various means in

weakening or streamlining the franchising requirements applica-

ble to them. They have had significant success at the federal and

state level, securing an FCC ruling and numerous state franchise

laws that facilitate their entry into the video marketplace.

Because telephone companies have been successful in avoiding

or weakening the franchise and other regulatory requirements

that remain applicable to cable operators like us, their competi-

tive posture has often been enhanced. The large scale entry of

major telephone companies as direct competitors in the video

marketplace could adversely affect the profitability and valuation

of our cable systems.

Additionally, we are subject to competition from utilities

that possess fiber optic transmission lines capable of transmitting

CHARTER COMMUNICATIONS, INC. 2007 FORM 10-K

11