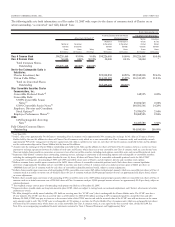

Charter 2007 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2007 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

VIDEO SERVICE

Cable Rate Regulation. The cable industry has operated under a

federal rate regulation regime for more than a decade. The

regulations currently restrict the prices that cable systems charge

for the minimum level of video programming service, referred to

as “basic service,” and associated equipment. All other cable

offerings are now universally exempt from rate regulation.

Although basic service rate regulation operates pursuant to a

federal formula, local governments, commonly referred to as

local franchising authorities, are primarily responsible for admin-

istering this regulation. The majority of our local franchising

authorities have never been certified to regulate basic service

cable rates (and order rate reductions and refunds), but they

generally retain the right to do so (subject to potential regulatory

limitations under state franchising laws), except in those specific

communities facing “effective competition,” as defined under

federal law. With increased competition from DBS and telephone

companies offering video service, our systems are increasingly

likely to satisfy the effective competition standard. We have

already secured FCC recognition of effective competition, and

become rate deregulated in many of our communities.

There have been frequent calls to impose expanded rate

regulation on the cable industry. Confronted with rapidly increas-

ing cable programming costs, it is possible that Congress may

adopt new constraints on the retail pricing or packaging of cable

programming. For example, there has been considerable legisla-

tive and regulatory interest in requiring cable operators to offer

historically bundled programming services on an à la carte basis,

or to at least offer a separately available child-friendly “family

tier.” Such mandates could adversely affect our operations.

Federal rate regulations generally require cable operators to

allow subscribers to purchase premium or pay-per-view services

without the necessity of subscribing to any tier of service, other

than the basic service tier. The applicability of this rule in certain

situations remains unclear, and adverse decisions by the FCC

could affect our pricing and packaging of services. As we attempt

to respond to a changing marketplace with competitive pricing

practices, such as targeted promotions and discounts, we may

face Communications Act uniform pricing requirements that

impede our ability to compete.

Must Carry/Retransmission Consent. There are two alternative legal

methods for carriage of local broadcast television stations on

cable systems. Federal “must carry” regulations require cable

systems to carry local broadcast television stations upon the

request of the local broadcaster. Alternatively, federal law

includes “retransmission consent” regulations, by which popular

commercial television stations can prohibit cable carriage unless

the cable operator first negotiates for “retransmission consent,”

which may be conditioned on significant payments or other

concessions. Broadcast stations must elect “must carry” or

“retransmission consent” every three years, with the next election

to be made prior to October 1, 2008. Either option has a

potentially adverse effect on our business. Popular stations

invoking “retransmission consent” have been increasingly

demanding in their negotiations with cable operators.

In September 2007, the FCC adopted an order increasing

the cable industry’s existing must-carry obligations by requiring

cable operators to offer “must carry” broadcast signals in both

analog and digital format (dual carriage) for a three year period

commencing on February 17, 2009, the date on which the

broadcast television industry will complete its ongoing transition

from an analog to digital format. The burden could increase

further if cable systems are required to carry multiple program

streams included within a single digital broadcast transmission

(multicast carriage), which the recent FCC order did not address.

Additional government-mandated broadcast carriage obligations

could disrupt existing programming commitments, interfere with

our preferred use of limited channel capacity, and limit our

ability to offer services that appeal to our customers and generate

revenues. We may need to take additional operational steps

and/or make further operating and capital investments by Febru-

ary 17, 2009 to ensure that customers not otherwise equipped to

receive digital programming, retain access to broadcast

programming.

Access Channels. Local franchise agreements often require cable

operators to set aside certain channels for public, educational,

and governmental access programming. Federal law also requires

cable systems to designate a portion of their channel capacity for

commercial leased access by unaffiliated third parties, who gener-

ally offer programming that our customers do not particularly

desire. The FCC recently adopted a reduction in the rates that

operators can charge commercial leased access users and

imposed additional administrative requirements that will be bur-

densome on the cable industry. The FCC’s new rules were

adopted to facilitate commercial leased access usage. Under

federal statue, commercial leased access programmers are entitled

to use up to 15% of a cable system’s capacity. Increased activity

in this area could further burden the channel capacity of our

cable systems, and potentially limit the amount of services we

are able to offer and may necessitate further investments to

expand our network capacity.

Access to Programming. The Communications Act and the FCC’s

“program access” rules generally prevent satellite video program-

mers affiliated with cable operators from favoring cable operators

over competing multichannel video distributors, such as DBS,

and limit the ability of such programmers to offer exclusive

programming arrangements to cable operators. Given the height-

ened competition and media consolidation that we face, it is

possible that we will find it increasingly difficult to gain access to

popular programming at favorable terms. Such difficulty could

adversely impact our business.

Ownership Restrictions. Federal regulation of the communications

field traditionally included a host of ownership restrictions, which

limited the size of certain media entities and restricted their

ability to enter into competing enterprises. Through a series of

legislative, regulatory, and judicial actions, most of these

CHARTER COMMUNICATIONS, INC. 2007 FORM 10-K

13