Charter 2007 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2007 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

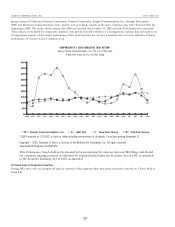

|

|

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS.

Reference is made to ‘Item 1A. Risk Factors‘ and ‘Cautionary

Statement Regarding Forward-Looking Statements,‘ which

describe important factors that could cause actual results to differ

from expectations and non-historical information contained

herein. In addition, the following discussion should be read in

conjunction with the audited consolidated financial statements of

Charter Communications, Inc. and subsidiaries as of and for the

years ended December 31, 2007, 2006, and 2005.

Overview

Charter is a broadband communications company operating in

the United States, with approximately 5.6 million customers at

December 31, 2007. Through our hybrid fiber and coaxial cable

network, we offer our customers traditional cable video program-

ming (analog and digital, which we refer to as “video” service),

high-speed Internet access, and telephone services, as well as,

advanced broadband services (such as OnDemand, high defini-

tion television service and DVR). See “Item 1. Business – Prod-

ucts and Services” for further description of these terms,

including “customers.”

Approximately 89% and 88% of our revenues for each of the

years ended December 31, 2007 and 2006, respectively, are

attributable to monthly subscription fees charged to customers

for our video, high-speed Internet, telephone, and commercial

services provided by our cable systems. Generally, these cus-

tomer subscriptions may be discontinued by the customer at any

time. The remaining 11% and 12% of revenue is derived prima-

rily from advertising revenues, franchise fee revenues (which are

collected by us but then paid to local franchising authorities),

pay-per-view and OnDemand programming (where users are

charged a fee for individual programs viewed), installation or

reconnection fees charged to customers to commence or rein-

state service, and commissions related to the sale of merchandise

by home shopping services.

The cable industry’s and our most significant competitive

challenges stem from DBS providers and DSL service providers.

In addition, telephone companies either offer or are making

upgrades of their networks that will allow them to offer services

that provide features and functions similar to our video, high-

speed Internet, and telephone services, and they also offer them

in bundles similar to ours. See “Item 1. Business – Competition.”

We believe that competition from DBS and telephone companies

has resulted in net video customer losses. In addition, we face

increasingly limited opportunities to expand our customer base

now that approximately 56% of our video customers subscribe to

our digital video service. These factors have contributed to

decreased growth rates for digital video customers. Similarly,

competition from DSL providers along with increasing penetra-

tion of high-speed Internet service in homes with computers has

resulted in decreased growth rates for high-speed Internet cus-

tomers. In the recent past, we have grown revenues by offsetting

video customer losses with price increases and sales of incremen-

tal services such as high-speed Internet, OnDemand, DVR, high

definition television, and telephone. We expect to continue to

grow revenues through price increases and high-speed Internet

upgrades, increases in the number of our customers who pur-

chase bundled services including high-speed Internet and tele-

phone, and through sales of incremental video services including

wireless networking, high definition television, OnDemand, and

DVR service. In addition, we expect to increase revenues by

expanding the sales of our services to our commercial customers.

However, we cannot assure you that we will be able to grow

revenues at historical rates, if at all.

Our expenses primarily consist of operating costs, selling,

general and administrative expenses, depreciation and amortiza-

tion expense and interest expense. Operating costs primarily

include programming costs, the cost of our workforce, cable

service related expenses, advertising sales costs and franchise fees.

Selling, general and administrative expenses primarily include

salaries and benefits, rent expense, billing costs, call center costs,

internal network costs, bad debt expense, and property taxes. We

are attempting to control our costs of operations by maintaining

strict controls on expenses. More specifically, we are focused on

managing our cost structure by improving workforce productiv-

ity, and leveraging our growth, and increasing the effectiveness of

our purchasing activities.

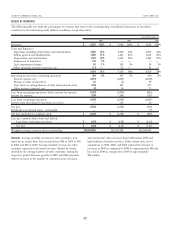

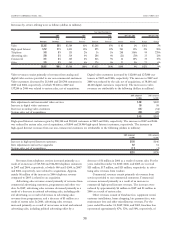

Our operating income from continuing operations increased

to $548 million for the year ended December 31, 2007 from

$367 million for the year ended December 31, 2006 and $304 mil-

lion for the year ended December 31, 2005. We had positive

operating margins (defined as operating income from continuing

operations divided by revenues) of 9%, 7%, and 6% for the years

ended December 31, 2007, 2006, and 2005, respectively. The

improvement in operating income from continuing operations

and operating margin for the years ended December 31, 2007,

2006, and 2005 is principally due to an increase in revenue over

expenses as a result of increased customers for high-speed

Internet, digital video, and telephone customers, as well as overall

rate increases.

We have a history of net losses. Further, we expect to

continue to report net losses for the foreseeable future. Our net

losses are principally attributable to insufficient revenue to cover

the combination of operating expenses and interest expenses we

incur because of our high amounts of debt, and depreciation

expenses resulting from the capital investments we have made

and continue to make in our cable properties. We expect that

these expenses will remain significant.

Beginning in 2004 and continuing through 2007, we sold

several cable systems to divest geographically non-strategic assets

and allow for more efficient operations, while also reducing debt

or increasing our liquidity. In 2005, 2006, and 2007, we closed

the sale of certain cable systems representing a total of approxi-

mately 33,000, 390,300, and 85,100 video customers, respectively.

As a result of these sales we have improved our geographic

footprint by reducing our number of headends, increasing the

number of customers per headend, and reducing the number of

states in which the majority of our customers reside. We have

CHARTER COMMUNICATIONS, INC. 2007 FORM 10-K

31