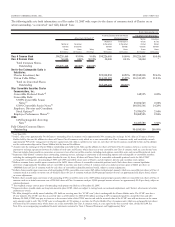

Charter 2007 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2007 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

signals with minimal signal distortion. Certain utilities are also

developing broadband over power line technology, which may

allow the provision of Internet and other broadband services to

homes and offices. Utilities have deployed broadband over power

line technology in a few limited markets. In some cases, it is the

local municipalities that regulate us, which own cable systems

that compete with us.

Broadcast Television

Cable television has long competed with broadcast television,

which consists of television signals that the viewer is able to

receive without charge using an “off-air” antenna. The extent of

such competition is dependent upon the quality and quantity of

broadcast signals available through “off-air” reception, compared

to the services provided by the local cable system. Traditionally,

cable television has provided higher picture quality and more

channel offerings than broadcast television. However, the recent

licensing of digital spectrum by the FCC now provides traditional

broadcasters with the ability to deliver high definition television

pictures and multiple digital-quality program streams, as well as

advanced digital services such as subscription video and data

transmission.

Traditional Overbuilds

Cable systems are operated under non-exclusive franchises his-

torically granted by local authorities. More than one cable system

may legally be built in the same area. It is possible that a

franchising authority might grant a second franchise to another

cable operator and that such franchise might contain terms and

conditions more favorable than those afforded us. In addition,

entities willing to establish an open video system, under which

they offer unaffiliated programmers non-discriminatory access to

a portion of the system’s cable system, may be able to avoid local

franchising requirements. Well-financed businesses from outside

the cable industry, such as public utilities that already possess

fiber optic and other transmission lines in the areas they serve,

may over time become competitors. There are a number of cities

that have constructed their own cable systems, in a manner

similar to city-provided utility services. There also has been

interest in traditional cable overbuilds by private companies not

affiliated with established local exchange carriers. Constructing a

competing cable system is a capital intensive process which

involves a high degree of risk. We believe that in order to be

successful, a competitor’s overbuild would need to be able to

serve the homes and businesses in the overbuilt area with equal

or better service quality, on a more cost-effective basis than we

can. Any such overbuild operation would require either signifi-

cant access to capital or access to facilities already in place that

are capable of delivering cable television programming.

As of December 31, 2007, excluding telephone companies,

we are aware of traditional overbuild situations impacting

approximately 7% to 8% of our total homes passed and potential

traditional overbuild situations in areas servicing approximately

an additional 2% of our total homes passed. Additional overbuild

situations may occur.

Private Cable

Additional competition is posed by satellite master antenna

television systems, or SMATV systems, serving multiple dwelling

units, or MDUs, such as condominiums, apartment complexes,

and private residential communities. Private cable systems can

offer improved reception of local television stations, and many of

the same satellite-delivered program services that are offered by

cable systems. SMATV systems currently benefit from operating

advantages not available to franchised cable systems, including

fewer regulatory burdens and no requirement to service low

density or economically depressed communities. The FCC

recently adopted regulations that favor SMATV and private cable

operators serving MDU complexes, allowing them to continue to

secure exclusive contracts with MDU owners. The FCC regula-

tions have been appealed, and the FCC is currently considering

whether to restrict their ability to enter into exclusive arrange-

ments, but this sort of regulatory disparity, if it withstands judicial

review, provides a competitive advantage to certain of our

current and potential competitors.

Other Competitors

Local wireless Internet services have recently begun to operate in

many markets using available unlicensed radio spectrum. Some

cellular phone service operators are also marketing PC cards

offering wireless broadband access to their cellular networks.

These service options offer another alternative to cable-based

Internet access.

High-speed Internet access facilitates the streaming of video

into homes and businesses. As the quality and availability of

video streaming over the Internet improves, video streaming

likely will compete with the traditional delivery of video pro-

gramming services over cable systems. It is possible that pro-

gramming suppliers will consider bypassing cable operators and

market their services directly to the consumer through video

streaming over the Internet.

REGULATION AND LEGISLATION

The following summary addresses the key regulatory and legisla-

tive developments affecting the cable industry and our three

primary services: video service, high-speed Internet service, and

telephone service. Cable system operations are extensively regu-

lated by the federal government (primarily the FCC), certain

state governments, and most local governments. A failure to

comply with these regulations could subject us to substantial

penalties. Our business can be dramatically impacted by changes

to the existing regulatory framework, whether triggered by

legislative, administrative, or judicial rulings. Congress and the

FCC have frequently revisited the subject of communications

regulation often designed to increase competition to the cable

industry, and they are likely to do so in the future. We could be

materially disadvantaged in the future if we are subject to new

regulations that do not equally impact our key competitors. We

can provide no assurance that the already extensive regulation of

our business will not be expanded in the future.

CHARTER COMMUNICATIONS, INC. 2007 FORM 10-K

12