Charter 2007 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2007 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

disclosures under GAAP, nor do they impact our accounting for

capital expenditures under GAAP.

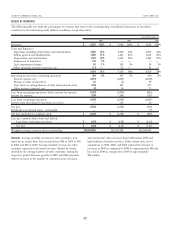

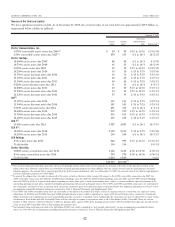

The following table presents our major capital expenditures

categories in accordance with NCTA disclosure guidelines for

the years ended December 31, 2007, 2006, and 2005 (dollars in

millions):

2007 2006 2005

For the Years Ended December 31,

Customer premise equipment

(a)

$ 578 $ 507 $ 434

Scalable infrastructure

(b)

232 214 174

Line extensions

(c)

105 107 134

Upgrade/Rebuild

(d)

52 45 49

Support capital

(e)

277 230 297

Total capital expenditures $1,244 $1,103 $1,088

(a)

Customer premise equipment includes costs incurred at the customer residence

to secure new customers, revenue units and additional bandwidth revenues. It

also includes customer installation costs in accordance with SFAS No. 51,

Financial Reporting by Cable Television Companies, and customer premise equip-

ment (e.g., set-top boxes and cable modems, etc.).

(b)

Scalable infrastructure includes costs not related to customer premise equipment

or our network, to secure growth of new customers, revenue units, and additional

bandwidth revenues, or provide service enhancements (e.g., headend equipment).

(c)

Line extensions include network costs associated with entering new service areas

(e.g., fiber/coaxial cable, amplifiers, electronic equipment, make-ready and design

engineering).

(d)

Upgrade/rebuild includes costs to modify or replace existing fiber/coaxial cable

networks, including betterments.

(e)

Support capital includes costs associated with the replacement or enhancement

of non-network assets due to technological and physical obsolescence (e.g.,

non-network equipment, land, buildings and vehicles).

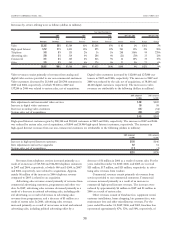

DESCRIPTION OF OUR OUTSTANDING DEBT

Overview

As of December 31, 2007 and 2006, our long-term debt totaled

approximately $19.9 billion and $19.1 billion, respectively. This

debt was comprised of approximately $7.2 billion and $5.4 billion

of credit facility debt, $12.3 billion and $13.3 billion accreted

amount of high-yield notes and $402 million and $408 million

accreted amount of convertible senior notes at December 31,

2007 and 2006, respectively. See the organizational chart on

page 4 and the first table under “– Liquidity and Capital

Resources – Overview of Our Debt and Liquidity” for debt

outstanding by issuer.

As of December 31, 2007 and 2006, the blended weighted

average interest rate on our debt was 9.0% and 9.5%, respectively.

The interest rate on approximately 85% and 78% of the total

principal amount of our debt was effectively fixed, including the

effects of our interest rate hedge agreements, as of December 31,

2007 and 2006, respectively. The fair value of our high-yield

notes was $10.3 billion and $13.3 billion at December 31, 2007

and 2006, respectively. The fair value of our convertible senior

notes was $332 million and $576 million at December 31, 2007

and 2006, respectively. The fair value of our credit facilities was

$6.7 billion and $5.4 billion at December 31, 2007 and 2006,

respectively. The fair value of high-yield and convertible notes

was based on quoted market prices, and the fair value of the

credit facilities was based on dealer quotations.

The following description is a summary of certain provisions

of our credit facilities and our notes (the “Debt Agreements”).

The summary does not restate the terms of the Debt Agreements

in their entirety, nor does it describe all terms of the Debt

Agreements. The agreements and instruments governing each of

the Debt Agreements are complicated and you should consult

such agreements and instruments for more detailed information

regarding the Debt Agreements.

Credit Facilities – General

Charter Operating Credit Facilities

The Charter Operating credit facilities were amended and

restated in March 2007, among other things, to defer maturities

and to increase availability. The Charter Operating credit facili-

ties provide borrowing availability of up to $8.0 billion as follows:

ka term loan with a total principal amount of $6.5 billion,

which is repayable in equal quarterly installments, com-

mencing March 31, 2008, and aggregating in each loan year

to 1% of the original amount of the term loan, with the

remaining balance due at final maturity on March 6, 2014;

and

ka revolving line of credit of $1.5 billion, with a maturity date

on March 6, 2013.

The Charter Operating credit facilities also allow us to enter

into incremental term loans in the future with an aggregate

amount of up to $1.0 billion, with amortization as set forth in the

notices establishing such term loans, but with no amortization

greater than 1% prior to the final maturity of the existing term

loan. However, no assurance can be given that we could obtain

such incremental term loans if Charter Operating sought to do

so.

Amounts outstanding under the Charter Operating credit

facilities bear interest, at Charter Operating’s election, at a base

rate or the Eurodollar rate, as defined, plus a margin for

Eurodollar loans of up to 2.00% for the revolving credit facility

and 2.00% for the term loan, and quarterly commitment fees of

0.5% per annum is payable on the average daily unborrowed

balance of the revolving credit facility.

The obligations of Charter Operating under the Charter

Operating credit facilities (the “Obligations”) are guaranteed by

Charter Operating’s immediate parent company, CCO Holdings,

and subsidiaries of Charter Operating, except for certain subsid-

iaries, including immaterial subsidiaries and subsidiaries precluded

from guaranteeing by reason of the provisions of other indebted-

ness to which they are subject (the “non-guarantor subsidiaries”).

The Obligations are also secured by (i) a lien on substantially all

of the assets of Charter Operating and its subsidiaries (other than

assets of the non-guarantor subsidiaries), to the extent such lien

can be perfected under the Uniform Commercial Code by the

filing of a financing statement, and (ii) a pledge by CCO

Holdings of the equity interests owned by it in Charter Operat-

ing or any of Charter Operating’s subsidiaries, as well as

intercompany obligations owing to it by any of such entities.

CHARTER COMMUNICATIONS, INC. 2007 FORM 10-K

46