Charter 2007 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2007 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

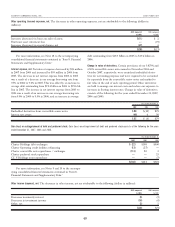

Under both SFAS No. 144 and SFAS No. 142, if an asset is

determined to be impaired, it is required to be written down to

its estimated fair market value. We determine fair market value

based on estimated discounted future cash flows, using reason-

able and appropriate assumptions that are consistent with inter-

nal forecasts. Our assumptions include these and other factors:

Penetration rates for analog and digital video, high-speed Inter-

net, and telephone; revenue growth rates; and expected operating

margins and capital expenditures. Considerable management

judgment is necessary to estimate future cash flows, and such

estimates include inherent uncertainties, including those relating

to the timing and amount of future cash flows, and the discount

rate used in the calculation.

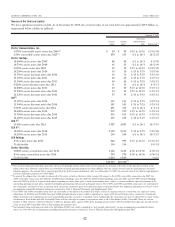

Franchises were aggregated into essentially inseparable asset

groups to conduct the valuations. The asset groups generally

represent geographic clustering of our cable systems into groups

by which such systems are managed. Management believes such

groupings represent the highest and best use of those assets.

Our valuations, which are based on the present value of

projected after tax cash flows, result in a value of property, plant

and equipment, franchises, customer relationships, and our total

entity value. The value of goodwill is the difference between the

total entity value and amounts assigned to the other assets. The

use of different valuation assumptions or definitions of franchises

or customer relationships, such as our inclusion of the value of

selling additional services to our current customers within cus-

tomer relationships versus franchises, could significantly impact

our valuations and any resulting impairment.

Franchises, for valuation purposes, are defined as the future

economic benefits of the right to solicit and service potential

customers (customer marketing rights), and the right to deploy

and market new services (service marketing rights). Fair value is

determined based on estimated discounted future cash flows

using assumptions consistent with internal forecasts. The fran-

chise after-tax cash flow is calculated as the after-tax cash flow

generated by the potential customers obtained (less the antici-

pated customer churn) and the new services added to those

customers in future periods. The sum of the present value of the

franchises’ after-tax cash flow in years 1 through 10 and the

continuing value of the after-tax cash flow beyond year 10 yields

the fair value of the franchise.

Customer relationships, for valuation purposes, represent the

value of the business relationship with our existing customers

(less the anticipated customer churn), and are calculated by

projecting future after-tax cash flows from these customers,

including the right to deploy and market additional services to

these customers. The present value of these after-tax cash flows

yields the fair value of the customer relationships. Substantially

all our acquisitions occurred prior to January 1, 2002. We did not

record any value associated with the customer relationship

intangibles related to those acquisitions. For acquisitions subse-

quent to January 1, 2002, we did assign a value to the customer

relationship intangible, which is amortized over its estimated

useful life.

Our impairment assessment as of October 1, 2007 did not

indicate impairment; however upon completion of our 2008

budgeting process in December 2007, we determined that a

triggering event requiring a reassessment of franchise values had

occurred. Largely driven by increased competition being experi-

enced by us and our peers, we lowered our projected revenue

and expense growth rates and increased our projected capital

expenditures, and accordingly revised our estimates of future cash

flows as compared to those used in prior valuations. See “Item 1.

Business – Competition.” As a result, we recorded $178 million of

impairment for the year ended December 31, 2007.

The valuations completed at October 1, 2006 and 2005

showed franchise values in excess of book value, and thus

resulted in no impairments.

The valuations used in our impairment assessments involve

numerous assumptions as noted above. While economic condi-

tions, applicable at the time of the valuation, indicate the

combination of assumptions utilized in the valuations are reason-

able, as market conditions change so will the assumptions, with a

resulting impact on the valuation and consequently the potential

impairment charge. At December 31, 2007, a 10% and 5% decline

in the estimated fair value of our franchise assets in each of our

asset groupings would have increased our impairment charge by

approximately $840 million and $390 million, respectively. A

10% and 5% increase in the estimated fair value of our franchise

assets in each of our asset groupings would have reduced our

impairment charge by approximately $178 million and $90 mil-

lion, respectively.

Income Taxes. All operations are held through Charter Holdco

and its direct and indirect subsidiaries. Charter Holdco and the

majority of its subsidiaries are generally limited liability compa-

nies that are not subject to income tax. However, certain of these

limited liability companies are subject to state income tax. In

addition, the subsidiaries that are corporations are subject to

federal and state income tax. All of the remaining taxable

income, gains, losses, deductions and credits of Charter Holdco

are passed through to its members: Charter, CII and Vulcan

Cable. Charter is responsible for its share of taxable income or

loss of Charter Holdco allocated to it in accordance with the

Charter Holdco limited liability company agreement (“LLC

Agreement”) and partnership tax rules and regulations.

The LLC Agreement provides for certain special allocations

of net tax profits and net tax losses (such net tax profits and net

tax losses being determined under the applicable federal income

tax rules for determining capital accounts). Under the LLC

Agreement, through the end of 2003, net tax losses of Charter

Holdco that would otherwise have been allocated to Charter

based generally on its percentage ownership of outstanding

common units were allocated instead to membership units held

by Vulcan Cable and CII (the “Special Loss Allocations”) to the

extent of their respective capital account balances. After 2003,

under the LLC Agreement, net tax losses of Charter Holdco

were allocated to Charter, Vulcan Cable and CII based generally

on their respective percentage ownership of outstanding com-

mon units to the extent of their respective capital account

balances. Allocations of net tax losses in excess of the members’

aggregate capital account balances are allocated under the rules

34

CHARTER COMMUNICATIONS, INC. 2007 FORM 10-K