Lowe's 1998 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 1998 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

|

|

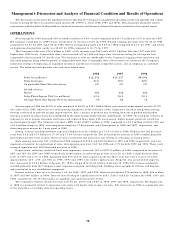

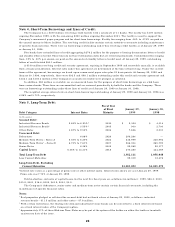

LIQUIDITY AND CAPITAL RESOURCES

Primary sources of liquidity are cash flows from operating activities and the sale of debt securities. Net cash provided by

operating activities was $696.8 million for 1998. This compared to $664.9 and $543.0 million in 1997 and 1996, respectively.

The increase in net cash provided by operating activities for 1998 is primarily related to increased earnings and various operating

liabilities offset by an increase in inventory, net of accounts payable. The increase during 1997 resulted primarily from increased

earnings and smaller increases in inventory, net of accounts payable, from year to year. Working capital at January 29, 1999 was

$820.3 million compared to $660.3 million at January 30, 1998.

The primary component of net cash used in investing activities continues to be new store facilities in connection with the

Company’s expansion plan. Cash acquisitions of fixed assets were $928 million for 1998. This compares to $773 million and

$677 million for 1997 and 1996, respectively. Retail selling space as of January 29, 1999, totaling 43.4 million square feet,

represents an 18.8% increase over the selling space as of January 30, 1998. The January 30, 1998 selling space total of 36.5

million square feet represents a 20.3% increase over the 1996 total of 30.4 million square feet. Financing and investing activities also

include noncash transactions of capital leases for new store facilities and equipment, the result of which is to increase long-term debt

and property. During 1998, 1997 and 1996, the Company acquired fixed assets (primarily new store facilities) under capital leases of

$47.3, $32.7 and $182.7 million, respectively.

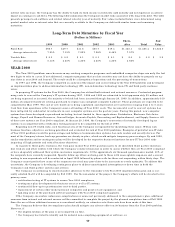

Cash flows provided by financing activities were $236.5, $221.7 and $11.9 million in 1998, 1997 and 1996, respectively. The

major cash components of financing activities in 1998 included the issuance of $300 million principal amount of 6.875% Deben-

tures due February 15, 2028, $50.8 million of cash dividend payments and $15.5 million of scheduled debt repayments. In 1997,

financing activities included the issuance of $268 million aggregate principal of Medium Term Notes (MTN’s) with final maturities

ranging from September 1, 2007 to May 15, 2037, cash dividend payments of $28.7 million and $32.8 million of scheduled debt

repayments. The interest rates on the MTN’s range from 6.07% to 7.61% and approximately 37% of these MTN’s may be put to the

Company at the option of the holder on either the tenth or twentieth anniversary date of the issue. The major financing activities for

1996 included the non-cash conversion of $284.7 million principal amount of 3% Convertible Subordinated Notes into common

stock and $34.7 million in cash dividend payments. The ratio of long-term debt to equity plus long-term debt was 29.0%, 28.7%

and 25.7% as of year end 1998, 1997 and 1996, respectively. The increases in 1998 and 1997 were primarily due to the issuance

of debt securities as previously described.

In February 1999, the Company issued $400 million principal of 6.5% Debentures due March 15, 2029 in a private offering. In

March 1999, the Company also issued 6,206,895 shares of common stock in a public offering. The net proceeds from the stock offering

were approximately $348.1 million. The shares were issued under a shelf registration statement filed with the Securities and Ex-

change Commission in December 1997.

At January 29, 1999, the Company had a $300 million revolving credit facility with a syndicate of eleven banks, available lines

of credit aggregating $278 million for the purpose of issuing documentary letters of credit and standby letters of credit and $80

million available, on an unsecured basis, for the purpose of short-term borrowings on a bid basis from various banks. At January 29,

1999, outstanding letters of credit aggregated $80.1 million. The revolving credit facility has $100 million expiring in November

1999, with the remaining $200 million expiring in November 2001. In addition, the Company has a $100 million revolving credit

and security agreement from a financial institution with $92.5 million outstanding at January 29, 1999.

The Company’s 1999 capital budget is currently at $1.6 billion, inclusive of approximately $214 million of operating or capital

leases. More than 80% of this planned commitment is for store expansion. Expansion plans for 1999 consist of approximately 80 to

85 stores (including the relocation of 30 to 35 older, smaller format stores). This planned expansion is expected to increase sales

floor square footage by approximately 18%. Approximately 15% of the 1999 projects will be leased and 85% will be owned.

Additionally, the Company has entered into an agreement with a lessor to build a one million square foot regional distribution center

in Pennsylvania, which is expected to be operational in Spring 1999. In addition, a 195 thousand square foot specialty distribution

center will be located at the same site. At January 29, 1999, the Company operated four regional distribution centers and nine smaller

support facilities. The Company believes that funds from operations, funds from equity and debt issuances, leases and existing

short-term credit agreements will be adequate to finance the 1999 expansion plan and other operating needs.

In November 1998, the Company entered into a merger agreement to acquire Eagle Hardware and Garden, Inc. (Eagle) in a

stock-for-stock merger transaction, which was completed April 2, 1999. The transaction was valued at approximately $1 billion,

structured as a tax-free exchange of the Company's common stock for Eagle's common stock, and accounted for as a pooling of

interests. Summary, combined company, pro forma financial information for 1998, 1997 and 1996 is included in Note 14 of the

consolidated financial statements.

General inflation has not had a material impact on the Company during the past three years. As noted above, the LIFO credit

was $29.0 and $7.0 million in 1998 and 1997, respectively. This compares to a charge of $1.4 million in 1996. Overall inventory

deflation was 1.69% and .99% for 1998 and 1997, respectively. There was overall inventory inflation of .15% for 1996.

MARKET RISK

The Company had no derivative financial instruments at January 29, 1999 or January 30, 1998.

The Company’s major market risk exposure is the potential loss arising from changing interest rates and its impact on long-term

investments and long-term debt. The Company’s policy is to manage interest rate risks by maintaining a combination of fixed and

variable rate financial instruments. At January 29, 1999, long-term investments consisted of $28.7 million in municipal obligations,

classified as available-for-sale securities. Although the fair value of these securities, like all fixed income securities, would fall if

16