Lowe's 1998 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 1998 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

|

|

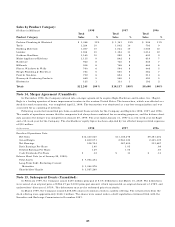

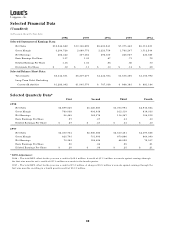

Note 1, Summary of Significant Accounting Policies:

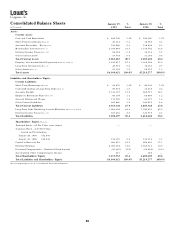

The Company is one of the largest retailers serving the do-it-yourself home improvement, home decor, and home construc-

tion markets in the United States. The Company operated 484 stores in 27 states at January 29, 1999 predominantly located

in the eastern half of the United States. Below are those accounting policies considered to be significant.

Stock Split – On May 29, 1998, the Board of Directors declared a two-for-one stock split on the Company’s common

stock. One additional share was issued on June 26, 1998 for each share held by shareholders of record on June 12, 1998.

The accompanying consolidated financial statements, including per share data, have been adjusted to reflect the effect of the

stock split.

Fiscal Year – Effective February 1, 1997, the Company adopted a 52 or 53 week fiscal year, changing the year end date

from January 31 to the Friday nearest January 31. The fiscal years ended January 29, 1999 and January 30, 1998 each had 52

weeks. All references herein for the years 1998, 1997 and 1996 represent the fiscal years ended January 29, 1999,

January 30, 1998 and January 31, 1997, respectively.

Principles of Consolidation – The consolidated financial statements include the accounts of the Company and its subsidiaries,

all of which are wholly owned. All material intercompany accounts and transactions have been eliminated.

Use of Estimates – The preparation of the Company’s financial statements in conformity with generally accepted accounting

principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and

disclosure of contingent assets and liabilities at the date of the financial statements and reported amounts of revenues and

expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash Equivalents – Cash and cash equivalents include cash on hand, demand deposits, and short-term invest-

ments with original maturities of three months or less when purchased.

Investments – The Company has a cash management program which provides for the investment of excess cash balances

in financial instruments which have maturities of up to five years. Investments, exclusive of cash equivalents, with a maturity

date of one year or less from the balance sheet date are classified as short-term investments. Investments with maturities

greater than one year are classified as long-term. Investments consist primarily of tax-exempt notes and bonds, municipal

preferred tax-exempt stock and repurchase agreements.

The Company has classified all investment securities as available-for-sale, and they are carried at fair market value. Unrealized

gains and losses on such securities are included in accumulated other comprehensive income in shareholders’ equity.

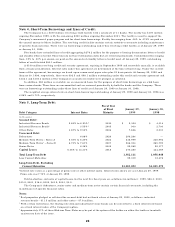

Derivatives – The Company does not use derivative financial instruments for trading purposes. Interest rate swap and

cap agreements, which are occasionally used by the Company in the management of interest rate exposure, are accounted for

on a settlement basis. Income and expense are recorded in the same category as that arising from the related liability. The

Company had no such derivative financial instruments as of January 29, 1999 or January 30, 1998.

Accounts Receivable – The majority of the accounts receivable arise from sales to professional building contractors.

The allowance for doubtful accounts is based on historical experience and a review of existing receivables. The allowance

for doubtful accounts was $2.0 and $1.6 million at January 29, 1999 and January 30, 1998, respectively.

Sales generated through the Company’s private label credit card are not reflected in receivables. Under an agreement

with Monogram Credit Card Bank of Georgia (the Bank), a wholly owned subsidiary of General Electric Capital Corporation,

consumer credit is extended directly to customers by the Bank and all credit program related services are performed directly

by the Bank.

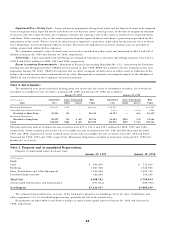

Merchandise Inventory – Inventory is stated at the lower of cost or market. In an effort to more closely match cost of

sales and related sales, cost is determined using the last-in, first-out (LIFO) method. Included in inventory cost are certain

costs associated with the preparation of inventory for resale. If the FIFO method had been used, inventories would have

been $38.6 and $67.6 million higher at January 29, 1999 and January 30, 1998, respectively.

Property and Depreciation – Property is recorded at cost. Costs associated with major additions are capitalized and

depreciated. Upon disposal, the cost of properties and related accumulated depreciation is removed from the accounts with

gains and losses reflected in earnings.

Depreciation is provided over the estimated useful lives of the depreciable assets. Assets are generally depreciated on the

straight-line method. Leasehold improvements are depreciated over the shorter of their estimated useful lives or term of the

related lease.

Leases – Assets under capital leases are amortized in accordance with the Company’s normal depreciation policy for

owned assets or over the lease term, if shorter, and the charge to earnings is included in depreciation expense in the

consolidated financial statements.

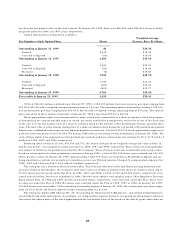

Income Taxes – Income taxes are provided for temporary differences between the tax and financial accounting bases of

assets and liabilities using the liability method. The tax effects of such differences are reflected in the balance sheet at the

enacted tax rates expected to be in effect when the differences reverse.

Store Pre-opening Costs – Costs of opening new retail stores are charged to operations as incurred.

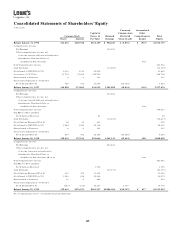

Notes to Consolidated Financial Statements

Years Ended January 29, 1999, January 30, 1998 and January 31, 1997

23