Lowe's 1999 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 1999 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

|

|

15

Management’s Discussion and

Analysis of Financial Condition

and Results of Operations

This discussion summarizes the significant factors

affecting the Company’s consolidated operating results and

liquidity and capital resources during the three-year

period ended January 28, 2000 (i.e., fiscal years 1999,

1998 and 1997). This discussion should be read in con-

junction with the Letter to Shareholders, financial state-

ments, and financial statement footnotes included in this

annual report.

The Company changed its method of accounting for

substantially all of its inventories from the Last-In-First-

Out (LIFO) method to the First-In-First-Out (FIFO)

method effective for the fiscal year ended January 28, 2000.

The Company has been experiencing reduced costs in most

product categories resulting from a combination of better

buying, increased imports and logistics efficiencies. There-

fore, management believes the FIFO method provides a

better measurement of operating results. The change will

also aid in financial statement comparability within the

retail home improvement industry segment.

Prior period consolidated financial statements have

been restated for the retroactive effect of the change in

accounting method. A LIFO adjustment was not required

during 1999 because the calculated effect was minimal;

therefore there was no effect on current year earnings. The

effect of this change on the Company’s net earnings and

retained earnings for the years ended January 29, 1999

and January 30, 1998 was a decrease of $18.4 million ($.05

per share diluted) and $4.4 million ($.01 per share

diluted), respectively.

The Company completed its merger with Eagle Hard-

ware & Garden, Inc. (Eagle) on April 2, 1999. The trans-

action, which was valued at approximately $1.3 billion,

was structured as a tax-free exchange of the Company’s

common stock for Eagle’s common stock, and was

accounted for as a pooling of interests. As a result,

all current and historical financial information is presented

on a combined basis.

OPERATIONS

Net earnings for 1999 increased 34% to $672.8 mil-

lion or 4.2% of sales compared to $500.4 million or 3.8%

of sales for 1998. Diluted earnings per share were $1.75

for 1999 compared to $1.34 for 1998 and $1.04 for 1997.

Return on beginning assets was 9.5% for 1999 compared

to 8.5% for 1998; and return on beginning shareholders’

equity was 18.6% for 1999 compared to 16.8% for 1998.

Net earnings for 1999, excluding the one-time charge

of $.04 per share for costs relating to the merger with Eagle,

increased 38% to $689.8 million or 4.3% of sales. Diluted

earnings per share, excluding the one-time charge, were

$1.79 for 1999. Excluding the one-time charge, return on

beginning assets was 9.7% for 1999; and return on begin-

ning shareholders’ equity was 19.1% for 1999.

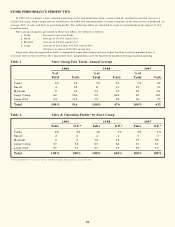

The Company’s sales were $15.9 billion in 1999, a

19% increase over 1998 sales of $13.3 billion. Sales for

1998 were 20% higher than 1997 levels. Comparable store

sales increased 6.2% in 1999. The increases in sales are

attributable to the Company’s ongoing store expansion and

relocation program along with the growth in comparable

store sales. Comparable store sales increases are driven by

the Company’s focus on commercial business, special

order, and installed sales initiatives, which is combined

with the continued strategy of employing an expanded

inventory assortment, everyday competitive prices and an

emphasis on customer service. The following table pre-

sents sales and store information:

1999 1998 1997

Sales (in millions) $15,906 $13,331 $11,108

Sales Increases 19% 20% 19%

Comparable Store Sales Increases 6% 6% 4%

At end of year:

Stores 576 520 477

Sales Floor Square Feet (in millions) 57.0 47.8 39.9

Average Store Size Net Selling

Square Feet (in thousands) 99 92 84

Gross margin in 1999 was 27.5% of sales compared to

26.8% in 1998. Both of these years showed improvement

over the 26.6% rate achieved in 1997. Lower product

acquisition costs, along with adherence to careful pricing

disciplines in the execution of the Company’s everyday

competitive pricing strategy, and changes in product mix

resulting from the expanded merchandise selection avail-

able in larger stores continued to provide margin improve-

ments during 1999 and 1998. In addition, an increase in

the level of controls relating to inventory shrinkage also

contributed to gross margin improvements in 1999.

Selling, general and administrative expenses (SG&A)

were $2.8 billion or 17.4% of sales in 1999. SG&A in the

two previous years were $2.3 and $2.0 billion or 17.5%

and 17.6% of sales, respectively. The 10 basis point

decrease in 1999 and 1998 resulted primarily from lower

net advertising costs, increased credit card program

income and leveraging of expenses.