Proctor and Gamble 2007 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2007 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

The Procter & Gamble Company 43Management’s Discussion and Analysis

(#-

(#.

(#.

%*

%,

%+

86E>I6AHE:C9>C<

d[cZihVaZh

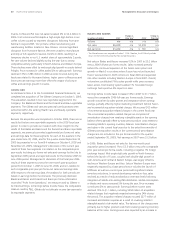

Proceeds from Asset Sales. Proceeds from asset sales in 2007 were

$281 million primarily due to the divestitures of Pert in North America,

Sure and several nonstrategic minor Beauty brands. In 2006, proceeds

from asset sales were $882 million primarily due to the divestitures of

Spinbrush, Rembrandt and Right Guard, all required by regulatory

authorities in relation to the Gillette acquisition, and our Korean paper

businesses.

Dividend Payments. Our rst discretionary use of cash is dividend

payments. Dividends per common share increased 11% to $1.28 per

share in 2007. This increase represents the 51st consecutive scal year

the Company has increased its common share dividend. Total dividend

payments to both common and preferred shareholders were $4.2 billion,

$3.7 billion and $2.7 billion in 2007, 2006 and 2005, respectively.

&#%(

&#'-

&#&*

%*

%,

%+

9>K>9:C9H

eZgXdbbdch]VgZ

Long-Term and Short-Term Debt. We maintain debt levels we

consider appropriate after evaluating a number of factors, including

cash ow expectations, cash requirements for ongoing operations,

investment plans (including acquisitions and share repurchase activities)

and the overall cost of capital. Total debt was $35.4 billion in 2007,

$38.1 billion in 2006 and $24.3 billion in 2005. The decrease in debt

in 2007 was primarily due to the utilization of operating cash ow

to pay down existing balances. Debt increased in 2006 primarily due

to additional debt used to nance the share repurchase program

announced in conjunction with the Gillette acquisition.

Liquidity. Our primary source of liquidity is cash generated from

operations. We believe internally generated cash ows adequately

support business operations, capital expenditures and shareholder

dividends, as well as a level of other discretionary cash uses (e.g., for

minor acquisitions or share repurchases).

We are able to supplement our short-term liquidity, if necessary, with

broad access to capital markets and three bank credit facilities. Broad

access to nancing includes commercial paper programs in multiple

markets at favorable rates given our strong credit ratings (including

separate U.S. dollar and Euro multi-currency programs).

We maintain three bank facilities: a $24 billion three-year facility

expiring in July 2008, a $1.8 billion facility expiring in August 2010

and a $1 billion facility expiring in July 2009. The credit facilities are

for general corporate purposes, including renancing needs

associated with the share buyback plan announced concurrently with

the Company’s acquisition of Gillette and to support our on-going

commercial paper program. Beyond some residual renancing

requirements on the debt related to acquisition of Gillette, we

anticipate that these facilities will remain largely undrawn beyond

June 2008. We periodically change our facility structure to take

advantage of more favorable nancing rates and to support our

longer term nancing needs.

These credit facilities do not have cross-default or ratings triggers, nor

do they have material adverse events clauses, except at the time of

signing. While not considered material to the overall nancial condition

of the Company, there is a covenant in the $1 billion credit facility

stating the ratio of net debt to earnings before interest expense,

income taxes, depreciation and amortization cannot exceed 4.0 at the

time of a draw on the facility. As of June 30, 2007, we are comfortably

below this level, with a ratio of approximately 1.6.

In addition to these credit facilities, long-term borrowing available

under our current shelf registration statement was $2.2 billion at

June 30, 2007.

The Company’s Moody’s and Standard & Poor’s (S&P) short-term

credit ratings are P-1 and A-1+, respectively. Our Moody’s and S&P

long-term credit ratings are Aa3 with a negative outlook and AA-

with a stable outlook, respectively.

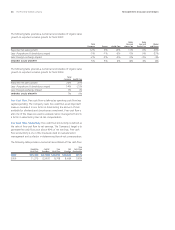

Treasury Purchases. Total share repurchases in 2007 were $5.6 billion,

of which $0.3 billion were made as part of our publicly announced

share repurchase plan in connection with the Gillette acquisition.

Total share repurchases in 2006 were $16.8 billion, nearly all of which

were made as part of our publicly announced share repurchase plan.

We completed the announced share buyback program in July 2006

and purchased a total of $20.1 billion of shares under this program.

In scal years 2008 to 2010, we expect to repurchase $24 – $30 billion

of Company shares at a rate of $8 – $10 billion per year.

Guarantees and Other Off-Balance Sheet Arrangements. We do not

have guarantees or other off-balance sheet nancing arrangements,

including variable interest entities, that we believe could have a

material impact on nancial condition or liquidity.