Safeway 1999 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 1999 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

19

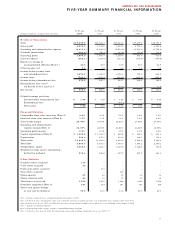

Sales Strong store operations

helped to increase identical-

store sales (stores operating

the entire year in both 1999

and 1998, excluding replace-

ment stores) 1.7% in 1999,

while comparable-store sales,

which include replacement

stores, increased 2.2% . In

1998, identical-store sales

increased 3.7% while compa-

rable-store sales increased

4.1% . Total sales for the

52 weeks of 1999 were

$28.9 billion, compared to

$24.5 billion for the 52 weeks of 1998 and $22.5 billion for the

53 weeks of 1997. Total sales increases are attributed to compa-

rable-store sales increases, the Vons Merger in 1997, the

Dominick’s Acquisition in 1998, and the Carrs and Randall’s

Acquisitions in 1999.

Gross Profit Safeway’s continuing improvement in buying prac-

tices and product mix helped to increase gross profit to 29.49%

of sales, from 29.10% in 1998 and 28.53% in 1997. On a pro

forma basis, gross profit increased 51 basis points from 28.98%

in 1998. Application of the LIFO method resulted in increases in

cost of goods sold of $1.2 million in 1999 and $7.1 million in

1998, and a decrease of $6.1 million in 1997.

Operating and Administrative Expense Operating and

administrative expense, including amortization of goodwill,

was 22.57% of sales in 1999 compared to 22.56% in 1998 and

22.84% in 1997. Safeway’s operating and administrative expense-

to-sales ratio increased in 1999 because Dominick’s, Carrs and

Randall’s operating and administrative expense ratio had histori-

cally been higher than Safeway’s. Increased sales and ongoing

efforts to reduce or control expenses improved this expense ratio

in 1998. Annual goodwill amortization has increased to $101.4 mil-

lion in 1999 from $56.3 million in 1998 and $41.8 million in

1997. On a pro forma basis, operating and administrative expense

declined 30 basis points from 22.87% in 1998.

Interest Expense Interest expense was $362.2 million in

1999, compared to $235.0 million in 1998 and $241.2 million in

1997. Interest expense increased in 1999 primarily because of

the debt incurred to finance the Dominick’s, Carrs and Randall’s

Acquisitions and, to a lesser extent, debt incurred to refinance

the repurchase of Safeway stock. Interest expense in 1998

included debt incurred in connection with the Dominick’s

Acquisition, which was partially offset by the paydown of certain

other indebtedness.

During 1997, Safeway recorded an extraordinary loss of $64.1

million ($0.13 per share) for the redemption of $589.0 million of

Safeway’s public debt, $285.5 million of Vons’ public debt, and

$40.0 million of medium-term notes, which was financed with

$600 million of new public senior debt securities and the balance

with commercial paper.

As of year-end 1999, the Company had effectively converted

$200.0 million of its floating rate debt to fixed interest rate debt

through interest rate swaps agreements. Under one swap agree-

ment, Safeway pays interest of 6.2% on the $100.0 million

notional amount and receives a variable interest rate based on

Federal Reserve rates quoted for commercial paper. This agree-

ment expires in 2007. Additionally, the Company assumed

two interest rate swap agreements, with notional amounts of

$50.0 million each, as part of the Randall’s Acquisition. Under

these swap agreements, Safeway pays interest of 5.30% and

5.49%, respectively, on the $50 million notional amounts and

receives a variable rate based on Federal Reserve rates quoted

for commercial paper. These swap agreements expire in 2001.

Interest rate swap agreements, and a cap agreement that expired

in 1999, increased interest expense by $1.7 million in 1999,

$2.8 million in 1998 and $3.3 million in 1997.

Equity in Earnings of Unconsolidated Affiliates

Safeway’s investment in affiliates consists of a 49% ownership

interest in Casa Ley, S.A. de C.V. (“Casa Ley”), which operates

86 food and general merchandise stores in western Mexico.

Through the first quarter of 1997, Safeway also held a 34.4%

interest in Vons. Safeway records its equity in earnings of uncon-

solidated affiliates on a one-quarter delay basis.

Income from Safeway’s equity investment in Casa Ley

increased to $34.5 million in 1999, from $28.5 million in 1998

and $22.7 million in 1997. Casa Ley’s financial results have been

improving since 1995, when Mexico suffered from the adverse

effects of high interest rates and inflation.

Equity in earnings of unconsolidated affiliates included

Safeway’s share of Vons earnings of $12.2 million in the first

quarter of 1997.

Liquidity and Financial Resources

Net cash flow from operations was $1,488.4 million in 1999,

$1,252.7 million in 1998 and $1,221.6 million in 1997. Net cash

flow from operations increased in 1999 and 1998 largely due to

increased net income.

Cash flow used by investing activities was $2,064.3 million

in 1999, $2,186.4 million in 1998 and $607.7 million in 1997.

The change in cash flow used by investing activities in 1999 and

1998 is primarily due to the Randall’s and Dominick’s Acquisitions

as well as increased capital expenditures. Safeway opened 67 new

stores and remodeled 251 stores in 1999. In 1998, Safeway

opened 46 new stores and remodeled 234 stores. The Company

completed a new distribution center in Maryland and opened a

new manufacturing plant in California during 1998.

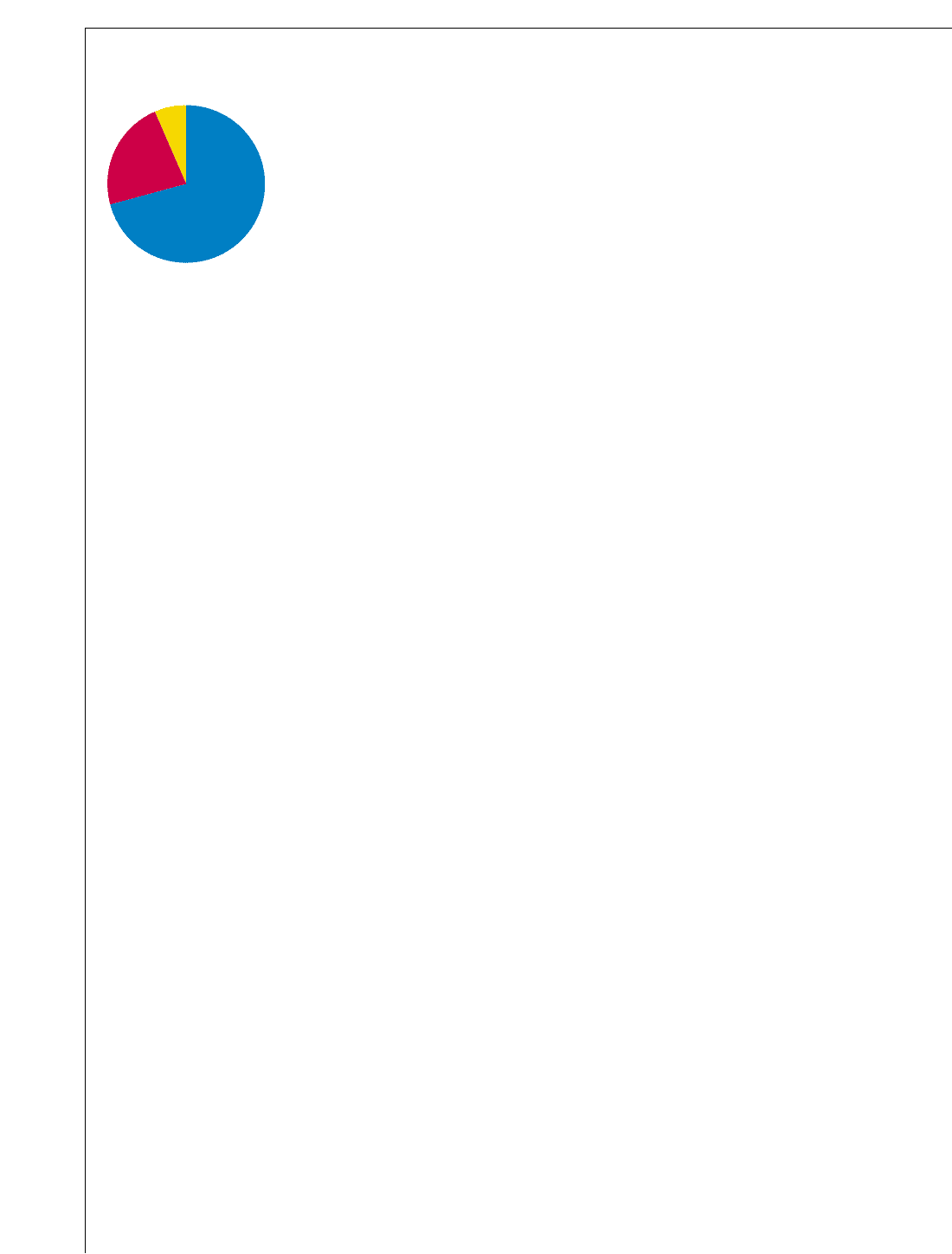

Portions of

1999 Sales Dollar

■ Costs of Goods Sold: 70.5%

■ Operating and

Administrating Expense: 22.6%

■ Operating Profit: 6.9%