Safeway 1999 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 1999 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

2

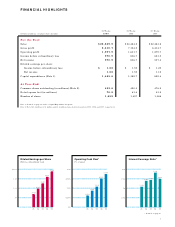

TO OUR STOCKHOLDERS

Safeway had another year of outstanding operating

and financial results in 1999. Once again we were one of

the industry’s leading performers, posting record earn-

ings and, on a pro forma basis, reducing our expense-to-

sales ratio for an unprecedented seventh straight year.

We also accelerated our capital spending program and

completed two more acquisitions.

Unfortunately, as many of you know, these achieve-

ments were not reflected in our stock price. The super-

market industry, typically a “stable” sector, seemed to

be out of favor in 1999 as investors found other sectors

more attractive.

Fortunately history has shown that, over time, the

financial markets tend to reward companies with strong

earnings, solid economic fundamentals and sound

management. We believe Safeway is widely regarded

as such a company.

Operating Results

As indicated in the following highlights, we continued

to make good progress in 1999.

■■Net income rose 20% to $970.9 million ($1.88 per

share) from $806.7 million ($1.59 per share) in 1998.

■■Total sales increased 18% to $28.9 billion, primarily

due to the acquisitions described below. Bolstered by

a strong fourth quarter, comparable-store sales for the

year were up 2.2% , while identical-store sales (which

exclude replacement stores) increased 1.7% . The corre-

sponding fourth-quarter sales gains were 3.7% and

2.9% , respectively.

■■On a pro forma basis, our gross profit margin

improved by 51 basis points in 1999. The increase

reflects continuing improvements in buying practices

and product mix.

■■On a pro forma basis, operating and administrative

expense as a percentage of sales fell 30 basis points,

largely as a result of increased sales and ongoing efforts

to reduce or control costs. Our O&A expense-to-sales

ratio has declined for seven consecutive years.

■■Operating cash flow as a percentage of sales reached

an all-time high of 9.35%.

■■Our interest coverage ratio (operating cash flow

divided by interest expense) remained a very strong

7.45 times despite the additional debt incurred to

finance acquisitions and the stock repurchase program,

described below.