Safeway 1999 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 1999 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

|

|

29

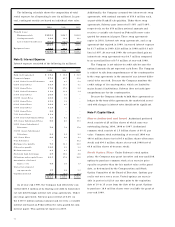

Off-balance sheet instruments The fair value of interest

rate swaps are the amount at which they could be settled

based on estimates obtained from dealers. At year-end

1999, net unrealized gains on such agreements were

$4.7 million compared to an unrealized loss of $7.0 million

at year-end 1998. Since the Company intends to hold these

agreements as hedges for the term of the agreements, the

market risk associated with changes in interest rates

should not be significant.

Impairment of Long-Lived Assets When Safeway

decides to close a store or other facility, the Company

accrues estimated future losses, if any, which may include

lease payments or other costs of holding the facility, net of

estimated future income in accordance with the provisions

of SFAS No. 121, “Accounting for the Impairment of Long-

Lived Assets and for Long-Lived Assets to be Disposed

of.” The operating costs, including depreciation, of stores

or other facilities to be sold or closed are expensed during

the period they remain in use. Safeway had an accrued lia-

bility of $87.3 million at year-end 1999 and $84.6 million

at year-end 1998 for such estimated future losses, which is

included in Accrued Claims and Other Liabilities in the

Company’s consolidated balance sheets.

Goodwill Goodwill is $4.8 billion at year-end 1999 and

$3.3 billion at year-end 1998, and is being amortized on a

straight-line basis over its estimated useful life of 40 years.

If it became probable that the projected future undiscounted

cash flows of acquired assets were less than the carrying

value of the goodwill, Safeway would recognize an impair-

ment loss in accordance with the provisions of SFAS No. 121.

Goodwill amortization was $101.4 million in 1999,

$56.3 million in 1998 and $41.8 million in 1997. Goodwill

and related amortization have increased due to the acquisi-

tions of Randall’s, Dominick’s and Carrs and the Vons

Merger discussed in Note B.

Stock-Based Compensation Safeway accounts for

stock-based awards to employees using the intrinsic

value method in accordance with Accounting Principles

Board Opinion No. 25, “Accounting for Stock Issued to

Employees.” The disclosure requirements of SFAS No. 123,

“Accounting for Stock-Based Compensation,” are set forth

in Note F.

New Accounting Standards In June 1998 the

Financial Accounting Standards Board issued Statement

of Financial Accounting Standards (“SFAS”) No. 133,

“Accounting for Derivative Instruments and Hedging

Activities,” which was amended by SFAS 137, which

defines derivatives, requires that derivatives be carried at

fair value, and provides for hedge accounting when certain

conditions are met. This statement is effective for Safeway

beginning in the first quarter of 2001. Although the

Company has not fully assessed the implications of this new

statement, the Company believes adoption of this statement

will not have a material impact on its financial statements.

During the first quarter of 1999, the Company adopted

SOP 98-5, “Reporting on the Costs of Start-Up Activities,”

which requires that costs incurred for start-up activities, such

as store openings, be expensed as incurred. This SOP did not

have a material impact on Safeway’s financial statements.

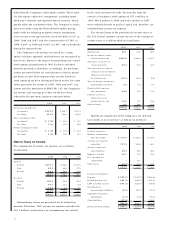

Note B: Acquisitions

In September 1999, Safeway acquired all of the outstand-

ing shares of Randall’s in exchange for $1.3 billion con-

sisting of $754 million of cash and 12.7 million shares of

Safeway stock. The Randall’s Acquisition was accounted

for as a purchase and resulted in goodwill of approximately

$1.3 billion which will be amortized over 40 years.

Safeway used proceeds from the issuance of subordinated

debt to fund the cash portion of the acquisition.

In April 1999, Safeway acquired Carrs by purchasing

all of the outstanding shares of Carrs for approximately

$106 million in cash. The Carrs Acquisition was account-

ed for as a purchase and resulted in goodwill of approxi-

mately $213 million which will be amortized over 40 years.

Safeway funded the acquisition, and subsequent repay-

ment of approximately $239 million of Carrs’ debt, with

issuance of commercial paper

In November 1998 Safeway completed its acquisition

of all of the outstanding shares of Dominick’s for a total

of approximately $1.2 billion in cash. The Dominick’s

Acquisition was accounted for as a purchase and resulted

in additional goodwill of $1.6 billion which is being

amortized over 40 years. Safeway funded the Dominick’s

Acquisition, including the repayment of approximately

$560 million of debt and lease obligations, with a combina-

tion of bank borrowings and commercial paper.

The following unaudited pro forma combined summary

financial information is based on the historical consolidated

results of operations of Safeway, Dominick’s, Carrs and

Randall’s as if the Dominick’s, Carrs and Randall’s

Acquisitions had occurred as of the beginning of each year

presented. This pro forma financial information is presented

for informational purposes only and may not be indicative

of what the actual consolidated results of operations would

have been if the acquisitions had been effective as of the

beginning of the years presented. Pro forma adjustments

were applied to the respective historical financial state-

ments to account for the Dominick’s, Carrs and Randall’s