Safeway 1999 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 1999 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

|

|

30

Acquisitions as purchases. Under purchase accounting, the

purchase price is allocated to acquired assets and liabilities

based on their estimated fair values at the date of acquisi-

tion, and any excess is allocated to goodwill.

For Randall’s and Carrs, such allocations are subject to

final determination based on real estate, leasehold and

equipment valuation studies, and a review of the books,

records and accounting policies of Randall’s and Carrs,

which are expected to be complete before the end of the

third quarter and first quarter of fiscal 2000, respectively.

Accordingly, the final allocations may be different from the

amount reflected herein, although management does not

expect such differences to be material.

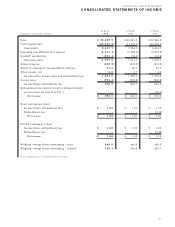

Pro Forma

(in millions, except per-share amounts) 1999 1998

Sales $30,801.8 $29,474.1

Net income $ 95 7.6 $ 706.2

Diluted earnings per share:

Net income $ 1.82 $ 1.42

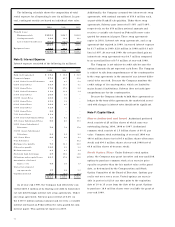

Note C: Financing

Notes and debentures were composed of the following at

year-end (in millions):

199 9 1998

Commercial paper $ 2 ,3 58 .1 $ 1,745.0

Bank credit agreement, unsecured 75.7 89.1

9.30% Senior Secured

Debentures due 2007 24 .3 24.3

6.85% Senior Notes due 2004, unsecured 200.0 200.0

7.00% Senior Notes due 2007, unsecured 250.0 250.0

7.45% Senior Debentures

due 2027, unsecured 150.0 150.0

5.75% Senior Notes due 2000, unsecured 400.0 400.0

5.875% Senior Notes due 2001, unsecured 400.0 400.0

6.05% Senior Notes due 2003, unsecured 350.0 350.0

6.50% Senior Notes due 2008, unsecured 250.0 250.0

7.00% Senior Notes due 2002, unsecured 600.0 –

7.25% Senior Notes due 2004, unsecured 400.0 –

7.50% Senior Notes due 2009, unsecured 500.0 –

9.35% Senior Subordinated Notes

due 1999, unsecured –66.7

10% Senior Subordinated Notes

due 2001, unsecured 79 .9 79.9

9.65% Senior Subordinated Debentures

due 2004, unsecured 81 .2 81.2

9.875% Senior Subordinated Debentures

due 2007, unsecured 24 .2 24.2

10% Senior Notes due 2002, unsecured 6.1 6.1

Mortgage notes payable, secured 75 .6 115.9

Other notes payable, unsecured 98 .8 102.7

Medium-term notes, unsecured 25 .5 25.5

Short-term bank borrowings, unsecured 129.7 161.8

■■■■■■■■■

6,479.1 4,522.4

Less current maturities (557.1) (279.8)

■■■■■■■■■

Long-term portion $ 5, 92 2.0 $ 4,242.6

■■■■■■■■■

Commercial Paper The amount of commercial paper

borrowings is limited to the unused borrowing capacity

under the bank credit agreement. Commercial paper is

classified as long-term because the Company intends to

and has the ability to refinance these borrowings on a

long-term basis through either continued commercial paper

borrowings or utilization of the bank credit agreement,

which matures in 2002. The weighted average interest rate

on commercial paper borrowings was 5.37% during 1999

and 6.79% at year-end 1999.

Bank Credit Agreement Safeway’s total borrowing

capacity under the bank credit agreement is $3.0 billion.

Of the $3.0 billion credit line, $2.0 billion matures in

2002 and has two one-year extension options, and $1.0 bil-

lion is renewable annually through 2004. The restrictive

covenants of the bank credit agreement limit Safeway with

respect to, among other things, creating liens upon its

assets and disposing of material amounts of assets other

than in the ordinary course of business. Safeway is also

required to meet certain financial tests under the bank

credit agreement. At year-end 1999, the Company had

total unused borrowing capacity under the bank credit

agreement of $520 million.

U.S. borrowings under the bank credit agreement carry

interest at one of the following rates selected by the

Company: (i) the prime rate; (ii) a rate based on rates at

which Eurodollar deposits are offered to first-class banks

by the lenders in the bank credit agreement plus a pricing

margin based on the Company’s debt rating or interest cov-

erage ratio (the “Pricing Margin”); or (iii) rates quoted at

the discretion of the lenders. Canadian borrowings denomi-

nated in U.S. dollars carry interest at one of the following

rates selected by the Company: (a) the Canadian base rate

or (b) the Canadian Eurodollar rate plus the Pricing

Margin. Canadian borrowings denominated in Canadian

dollars carry interest at one of the following rates selected

by the Company: (i) the Canadian prime rate or (ii) the rate

for Canadian bankers acceptances plus the Pricing Margin.

The weighted average interest rate on borrowings under

the bank credit agreement was 5.59% during 1999 and

5.18% at year-end 1999.

Senior Secured Indebtedness The 9.30% Senior

Secured Debentures due 2007 are secured by a deed of

trust which created a lien on the land, buildings and

equipment owned by Safeway at its distribution center in

Tracy, California.