American Airlines 1997 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 1997 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

|

|

AMR CORPORATION

61

The Black-Scholes option valuation model was devel-

oped for use in estimating the fair value of traded options

which have no vesting restrictions and are fully transfer-

able. In addition, option valuation models require the input

of highly subjective assumptions including the expected

stock price volatility. Because the Company’s employee

stock options have characteristics significantly different

from those of traded options, and because changes in the

subjective input assumptions can materially affect the fair

value estimate, in management’s opinion, the existing mod-

els do not necessarily provide a reliable single measure of

the fair value of its employee stock options. In addition,

because SFAS 123 is applicable only to options and stock-

based awards granted subsequent to December 31, 1994,

its pro forma effect will not be fully reflected until 1999.

The Company’s pro forma net earnings and earnings

per share assuming the Company had accounted for its

employee stock options using the fair value method

would have resulted in 1997 net earnings of $960 million

and basic and diluted earnings per share of $10.77 and

$10.50, respectively. The pro forma effect of SFAS 123 is

immaterial to the Company’s 1996 and 1995 net earnings

and earnings per share.

10. Retirement Benefits

Substantially all employees of American and employees of

certain other subsidiaries are eligible to participate in pension

plans. The defined benefit plans provide benefits for partici-

pating employees based on years of service and average com-

pensation for a specified period of time before retirement.

Airline pilots and flight engineers also participate in defined

contribution plans for which Company contributions are

determined as a percentage of participant compensation.

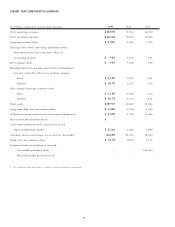

Total costs for all pension plans were (in millions):

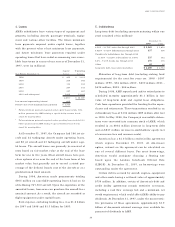

Year Ended December 31,

1997 1996 1995

Defined benefit plans:

Service cost - benefits earned

during the period $ 189 $204 $ 165

Interest cost on projected

benefit obligation 403 375 323

Return on assets (435) (91) (1,288)

Net amortization and deferral 26 (322) 1,008

Net periodic pension cost for

defined benefit plans 183 166 208

Defined contribution plans 142 132 124

Total $325 $298 $ 332

In addition to the pension costs shown above, in late

1995, AMR offered early retirement programs to select

groups of employees as part of its restructuring efforts. In

accordance with Statement of Financial Accounting Stan-

dards No. 88, “Employers’ Accounting for Settlements and

Curtailments of Defined Benefit Pension Plans and for Ter-

mination Benefits,” AMR recognized additional pension

expense of $220 million associated with these programs in

1995 which was included in restructuring costs. Of this

amount, $118 million was for special termination benefits

and $102 million was for the actuarial losses resulting

from the early retirements for 1995.

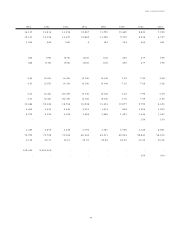

The funded status and actuarial present value of benefit

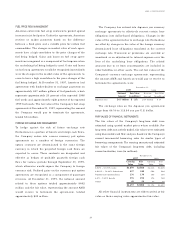

obligations of the defined benefit plans were (in millions):

December 31,

1997 1996

Plans with Plans with Plans with Plans with

Assets in Accumulated Assets in Accumulated

Excess of Benefit Excess of Benefit

Accumulated Obligation Accumulated Obligation

Benefit in Excess Benefit in Excess

Obligation of Assets Obligation of Assets

Vested benefit obligation $4,580 $ 53 $2,729 $ 1,435

Accumulated

benefit obligation $4,802 $ 57 $2,882 $ 1,510

Effect of projected

future salary increases 940 26 650 202

Projected benefit obligation 5,742 83 3,532 1,712

Plan assets at fair value 5,213 6 3,154 1,463

Plan assets less than

projected benefit obligation (529) (77) (378) (249)

Unrecognized net loss 761 27 729 237

Unrecognized prior

service cost 58 5 37 29

Unrecognized transition asset (21) 1 (32) -

Adjustment to record

minimum pension liability - (11) - (69)

Prepaid (accrued)

pension cost1$269 $ (55) $356 $ (52)

1AMR’s funding policy is to make contributions equal to, or in excess of,

the minimum funding requirements of the Employee Retirement Income

Security Act of 1974.

Plan assets consist primarily of domestic and foreign

government and corporate debt securities, marketable

equity securities, and money market and mutual fund

shares, of which approximately $92 million and $71 mil-

lion of plan assets at December 31, 1997 and 1996,

respectively, were invested in shares of mutual funds

managed by a subsidiary of AMR.