American Airlines 1997 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 1997 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

|

|

AMR CORPORATION

62

The projected benefit obligation was calculated using

weighted-average discount rates of 7.25% and 7.75% at

December 31, 1997 and 1996, respectively; rates of

increase for compensation ranging from 4.0% to 4.20% at

December 31, 1997 and 1996; and the 1983 Group

Annuity Mortality Table. The weighted-average expected

long-term rate of return on assets was 9.50% in 1997,

1996 and 1995. The vested benefit obligation and plan

assets at fair value at December 31, 1997, for plans whose

benefits are guaranteed by the Pension Benefit Guaranty

Corporation were $4.6 billion and $5.2 billion, respectively.

In October 1997, AMR spun off the portion of its

defined benefit pension plan applicable to employees of

The SABRE Group to the Legacy Pension Plan (LPP), a

defined benefit plan established by The SABRE Group

effective January 1, 1997. At the date of the spin-off, the

net obligation attributable to The SABRE Group employ-

ees participating in AMR’s plan was approximately $20

million. The SABRE Group also established The SABRE

Group Retirement Plan (SGRP), a defined contribution

plan. Effective January 1, 1997, employees of The SABRE

Group who were under the age of 40 as of December 31,

1996 participate in the SGRP. Employees of The SABRE

Group who were age 40 or over as of December 31, 1996

had the option of participating in either the SGRP or the

LPP. The SABRE Group contributes 2.75 percent of each

participating employee’s base pay to the SGRP. The

employees vest in the contributions after three years of ser-

vice, including any prior service with AMR affiliates. In

addition, The SABRE Group matches 50 cents of each dol-

lar contributed by participating employees, limited to the

first six percent of the employee’s base pay contribution,

subject to IRS limitations. Employees are immediately

vested in their own contributions and the Company’s

matching contributions. In 1997, costs for the SGRP were

$11 million.

In addition to pension benefits, other postretirement

benefits, including certain health care and life insurance

benefits, are also provided to retired employees. The

amount of health care benefits is limited to lifetime

maximums as outlined in the plan. Substantially all

employees of American and employees of certain other

subsidiaries may become eligible for these benefits if they

satisfy eligibility requirements during their working lives.

Certain employee groups make contributions toward

funding a portion of their retiree health care benefits

during their working lives. AMR funds benefits as incurred

and makes contributions to match employee prefunding.

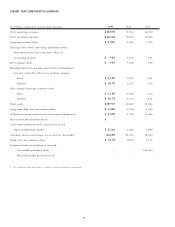

Net other postretirement benefit cost was (in millions):

Year Ended December 31,

1997 1996 1995

Service cost - benefits earned

during the period $48 $58 $ 48

Interest cost on accumulated other

postretirement benefit obligation 95 102 101

Return on assets (4) (3) (2)

Net amortization and deferral (14) (5) (6)

Net other postretirement benefit cost $125 $152 $ 141

In addition to net other postretirement benefit cost, in

late 1995, AMR offered early retirement programs to

select groups of employees as part of its restructuring

efforts. In accordance with Statement of Financial

Accounting Standards No. 106, “Employers’ Accounting

for Postretirement Benefits Other than Pensions,” AMR

recognized additional other postretirement benefit

expense of $93 million associated with the program in

1995 which was included in restructuring costs. Of this

amount, $26 million was for special termination benefits

and $67 million was for the net actuarial losses resulting

from the early retirements for 1995.

The funded status of the plan, reconciled to the

accrued other postretirement benefit cost recognized in

AMR’s balance sheet, was (in millions):

December 31,

1997 1996

Retirees $630 $593

Fully eligible active plan participants 178 128

Other active plan participants 598 492

Accumulated other postretirement

benefit obligation 1,406 1,213

Plan assets at fair value 56 39

Accumulated other postretirement

benefit obligation in excess of plan assets 1,350 1,174

Unrecognized net gain 177 300

Unrecognized prior service benefit 52 56

Accrued other postretirement benefit cost $1,579 $1,530

Plan assets consist primarily of shares of mutual funds

managed by a subsidiary of AMR.