American Express 2003 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2003 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

•AEFA uses interest rate caps, swaps and floors to protect the margin between the interest rates earned on investments and

the interest rates credited to holders of certain investment certificates and fixed annuities.

•Certain of AEFA’s annuity and investment certificate products have returns tied to the performance of equity markets.

These elements are considered derivatives under SFAS No. 133. AEFA manages this equity market risk by entering into

options and futures with offsetting characteristics.

•AEFA consolidated a derivative as a result of adopting FIN 46 as discussed in Note 1. The derivative’s value is based on

the interest and gains and losses related to a reference portfolio of high-yield loans.

See Note 6 for further information regarding the Company’s use of interest rate products related to short- and long-term

debt obligations.

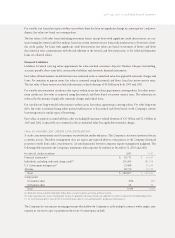

(Note 10) GUARANTEES AND OFF-BALANCE SHEET ITEMS

The Company, through its TRS operating segment, provides cardmember protection plans that cover losses associated with

purchased products, as well as certain other guarantees in the ordinary course of business that are within the scope of FASB

Interpretation No. 45, “Guarantor’s Accounting and Disclosure Requirement for Guarantees, Including Indirect Guarantees

of Indebtedness of Others” (FIN 45). In the hypothetical scenario that all claims occur within one year, the aggregate max-

imum amount of potential future losses associated with such guarantees would not exceed $82 billion. The total amount

of related liability accrued at December 31, 2003 for such programs was $486 million, which management believes to be

adequate based on actual experience. The Company has no collateral or other recourse provisions related to these guaran-

tees. Expenses relating to claims under these guarantees were approximately $30 million in 2003.

The Company, through its AEB operating segment, provides various guarantees to its customers in the ordinary course of

business that are also within the scope of FIN 45, including financial letters of credit, performance guarantees and finan-

cial guarantees, among others. Generally, guarantees range in term from three months to one year. AEB receives a fee related

to most of these guarantees, many of which help to facilitate customer cross-border transactions. At December 31, 2003,

the Company held $761 million of collateral supporting these guarantees. The following table provides information related

to such guarantees as of December 31, 2003:

(Millions) Maximum amount

of undiscounted Amount of related

Type of Guarantee future payments liability at 12/31/03

Financial letters of credit $207 $ 1.1

Performance guarantees 119 0.4

Financial guarantees 629 0.5

Total $955 $ 2.0

Additionally, the Company had $770 million and $1,036 million of loan commitments and other lines of credit at Decem-

ber 31, 2003 and 2002, respectively, as well as $544 million and $474 million of bank standby letters of credit, bank guar-

antees and bank commercial and other bank letters of credit at December 31, 2003 and 2002, respectively, which were

outside the scope of FIN 45. The Company issues commercial and other letters of credit to facilitate the short-term trade-

related needs of its banking clients, which typically mature within six months. At December 31, 2003 and 2002, the Com-

pany held $114 million and $148 million, respectively, of collateral supporting commercial and other letters of credit.

The Company also has commitments aggregating $156 billion and $126 billion related to its card business in 2003 and

2002, respectively, primarily related to commitments to extend credit to certain cardmembers as part of established lend-

ing product agreements. Many of these are not expected to be drawn; therefore, total unused credit available to cardmem-

bers does not represent future cash requirements. The Company’s charge card products have no preset spending limit and

are not reflected in unused credit available to cardmembers.

In addition, the Company has certain contingent obligations for worldwide business arrangements. These payments relate

to contractual agreements with partners entered into as part of the ongoing operation of the TRS business. The contingent

obligations under such arrangements were $2.5 billion as of December 31, 2003.

(p.95_axp_ notes to consolidated financial statements)