Electronic Arts 2001 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2001 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

ELECTRONIC ARTS

29

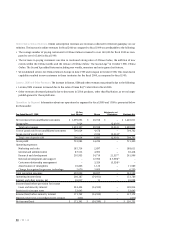

• During fiscal 2001, EA.com used $132,210,000 of cash in operations (including payments to AOL of approxi-

mately $11,250,000), $68,887,000 in capital expenditures for computer equipment, network infrastructure,

internal use software and related third party software, $43,333,000 for the acquisition of Pogo, gross of cash

received of $762,000, offset by $245,141,000 provided through capital contributions from Electronic Arts.

• During fiscal 2000, EA.com used $68,329,000 of cash in operations (including payments to AOL of approxi-

mately $36,000,000), $37,605,000 in capital expenditures for computer equipment, network infrastructure,

internal use software and related third party software, $1,499,000 for an investment in a 3rd party developer,

$32,539,000 for the acquisition of Kesmai and another acquisition, offset by $140,410,000 provided through

capital contributions from Electronic Arts.

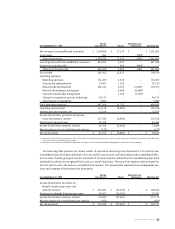

EA.com is required to pay $50,000,000 to AOL as a carriage fee under the AOL agreement. Of this amount,

$25,000,000 was paid upon signing the agreement and the remainder is due in four equal annual installments on

the first four anniversaries of the initial payment. During fiscal 2001, the Company paid AOL the first annual car-

riage payment of $6,250,000. EA.com is also required to pay to AOL $31,000,000 as an advance of a minimum

guaranteed revenue share for revenues generated by subscriptions and other certain commercial transactions on

the EA.com site. Of this amount, $11,000,000 was paid upon signing of the agreement and the remainder is due in

four equal annual installments on the first anniversary of the initial payment. During fiscal 2001, the Company

paid AOL the first annual revenue share payment of $5,000,000.

EA.com also made a commitment to spend $15,000,000 in offline media advertisements promoting our online

games, including those on the AOL service, during the term of the AOL agreement.

Future liquidity needs of EA.com will be met by Electronic Arts as Electronic Arts intends to continue to fund the

cash requirements of EA.com for the foreseeable future.

Impact of Recently Issued Accounting Standards

In June 1998, the Financial Accounting Standards Board (“FASB”)

issued Statement of Financial Accounting Standards No. 133 (“SFAS 133”) “Accounting for Derivative Instruments

and Hedging Activities”, as amended by SFAS 137 “Accounting for Derivative Instruments and Hedging Activities –

Deferral of the Effective Date of FASB Statement No. 133 – an Amendment of FASB Statement No. 133” and SFAS 138

“Accounting for Certain Derivative Instruments and Certain Hedging Activities – an Amendment of FASB Statement

No. 133” which establishes accounting and reporting standards for derivative instruments and hedging activities.

The terms of SFAS 133 and SFAS 138 are effective as of the beginning of the first quarter of the fiscal year beginning

after June 15, 2000. The Company is determining the effect of SFAS 133, 137 and 138 on its financial statements.

In April 2001, the Emerging Issues Task Force issued No. 00-25 (“EITF 00-25”), “Accounting for Consideration

from a Vendor to a Retailer in Connection with the Purchase or Promotion of the Vendor’s Products”, which states

that consideration from a vendor to a reseller of the vendor’s products is presumed to be a reduction of the selling

prices of the vendor’s products and, therefore, should be characterized as a reduction of revenue when recognized

in the vendor’s income statement. That presumption is overcome and the consideration can be categorized as a

cost incurred if, and to the extent that, a benefit is or will be received from the recipient of the consideration. That

benefit must meet certain conditions described in EITF 00-25. The consensus should be applied no later than in

annual or interim financial statements for periods beginning after December 15, 2001. The Company is currently

evaluating the impact of this consensus on its Statement of Operations.