Electronic Arts 2001 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2001 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72

|

|

ELECTRONIC ARTS

61

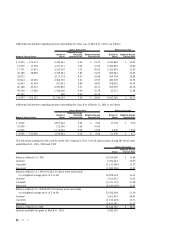

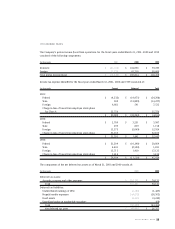

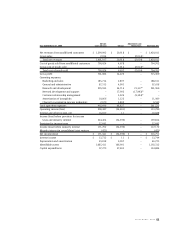

(17) COMPREHENSIVE INCOME

SFAS 130 requires classification of other comprehensive income in a financial statement and display of other com-

prehensive income separately from retained earnings and additional paid-in capital. Other comprehensive income

includes primarily foreign currency translation adjustments and unrealized gains (losses) on investments.

The change in the components of comprehensive income, net of tax, is summarized as follows (in thousands):

Foreign Currency Unrealized Accumulated

Translation Gains (Losses) Other Compre-

Adjustments on Investments hensive Loss

Balance at March 31, 1998 $ (3,198) $ 1,730 $ (1,468)

Other comprehensive income (loss) (2,643) 1,544 (1,099)

Balance at March 31, 1999 (5,841) 3,274 (2,567)

Other comprehensive loss (339) (3,455) (3,794)

Balance at March 31, 2000 (6,180) (181) (6,361)

Other comprehensive income (loss) (9,439) 3,097 (6,342)

Balance at March 31, 2001 $ (15,619) $ 2,916 $ (12,703)

Change in unrealized gains (losses) on investments, net are shown net of taxes of $1,391,000, $(1,553,000) and

$727,000 in fiscal 2001, 2000 and 1999, respectively.

The currency translation adjustments are not adjusted for income taxes as they relate to indefinite investments

in non-U.S. subsidiaries.

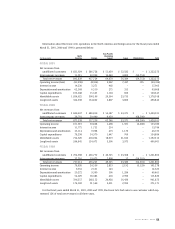

(18) DISCLOSURES ABOUT FAIR VALUE OF FINANCIAL INSTRUMENTS

The following methods and assumptions were used to estimate the fair value of each class of financial instruments

for which it is practicable to estimate that value:

Cash, cash equivalents, short-term investments, receivables, accounts payable and accrued liabilities – the

carrying amount approximates fair value because of the short maturity of these instruments.

Long-term investments, investments classified as held-to-maturity and marketable securities – fair value is

based on quoted market prices.

(19) SEGMENT INFORMATION

SFAS 131 establishes standards for the reporting by public business enterprises of information about product

lines, geographic areas and major customers. The method for determining what information to report is based on

the way that management organizes the operating segments within the Company for making operational decisions

and assessments of financial performance. The Company’s chief operating decision maker is considered to be the

Company’s Chief Executive Officer (“CEO”). The CEO reviews financial information presented on a consolidated

basis accompanied by disaggregated information about revenues by geographic region and by product lines for

purposes of making operating decisions and assessing financial performance.