Electronic Arts 2001 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2001 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

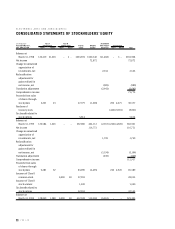

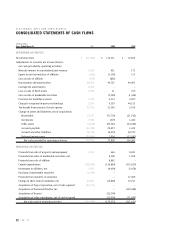

ELECTRONIC ARTS

31

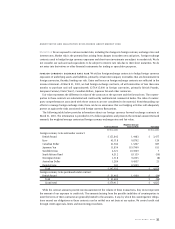

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Market Risk

We are exposed to various market risks, including the changes in foreign currency exchange rates and

interest rates. Market risk is the potential loss arising from changes in market rates and prices. Foreign exchange

contracts used to hedge foreign currency exposures and short-term investments are subject to market risk. We do

not consider our cash and cash equivalents to be subject to interest rate risk due to their short maturities. We do

not enter into derivatives or other financial instruments for trading or speculative purposes.

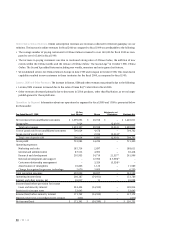

FOREIGN CURRENCY EXCHANGE RATE RISK We utilize foreign exchange contracts to hedge foreign currency

exposures of underlying assets and liabilities, primarily certain intercompany receivables that are denominated in

foreign currencies, thereby, limiting our risk. Gains and losses on foreign exchange contracts are reflected in the

income statement. At March 31, 2001, we had foreign exchange contracts, all with maturities of less than nine

months to purchase and sell approximately $279,415,000 in foreign currencies, primarily British Pounds,

European Currency Units (“Euro”), Canadian Dollars, Japanese Yen and other currencies.

Fair value represents the difference in value of the contracts at the spot rate and the forward rate. The counter-

parties to these contracts are substantial and creditworthy multinational commercial banks. The risks of counter-

party nonperformance associated with these contracts are not considered to be material. Notwithstanding our

efforts to manage foreign exchange risks, there can be no assurances that our hedging activities will adequately

protect us against the risks associated with foreign currency fluctuations.

The following table below provides information about our foreign currency forward exchange contracts at

March 31, 2001. The information is provided in U.S. dollar equivalents and presents the notional amount (forward

amount), the weighted average contractual foreign currency exchange rates and fair value.

Weighted-Average

Contract Amount Contract Rate Fair Value

(In thousands) (In thousands)

Foreign currency to be sold under contract:

British Pound $ 155,842 1.4483 $ 3,477

Euro 45,718 0.8792 120

Canadian Dollar 21,942 1.5267 687

Japanese Yen 11,854 119.7900 611

Swedish Krona 4,521 10.3969 7

South African Rand 4,312 8.1159 (56)

Norwegian Krone 1,518 9.2235 (8)

Australian Dollar 1,284 0.4937 21

Danish Krone 941 8.5009 –

Total $ 247,932 $ 4,859

Foreign currency to be purchased under contract:

British Pound $ 31,483 1.4160 $ (34)

Total $ 31,483 $ (34)

Grand total $ 279,415 $ 4,825

While the contract amounts provide one measurement of the volume of these transactions, they do not represent

the amount of our exposure to credit risk. The amounts (arising from the possible inabilities of counterparties to

meet the terms of their contracts) are generally limited to the amounts, if any, by which the counterparties’ obliga-

tions exceed our obligations as these contracts can be settled on a net basis at our option. We control credit risk

through credit approvals, limits and monitoring procedures.